Interested in electric cars, high speed trains, and/or space travel? Chances are then, you are familiar with Elon Musk. Use Twitter? You have likely come across a missive or two from the eccentric South African billionaire, who co-founded PayPal before joining Tesla and launching Space X and The Boring Company, the latter of which refers to his hyperloop endeavor. The 47-year old utilizes the social media platform to post photos of rocket ships, share press mentions about his companies, crack jokes, and debate the merits of the mainstream media. Rather standard fare for a Twitter user.

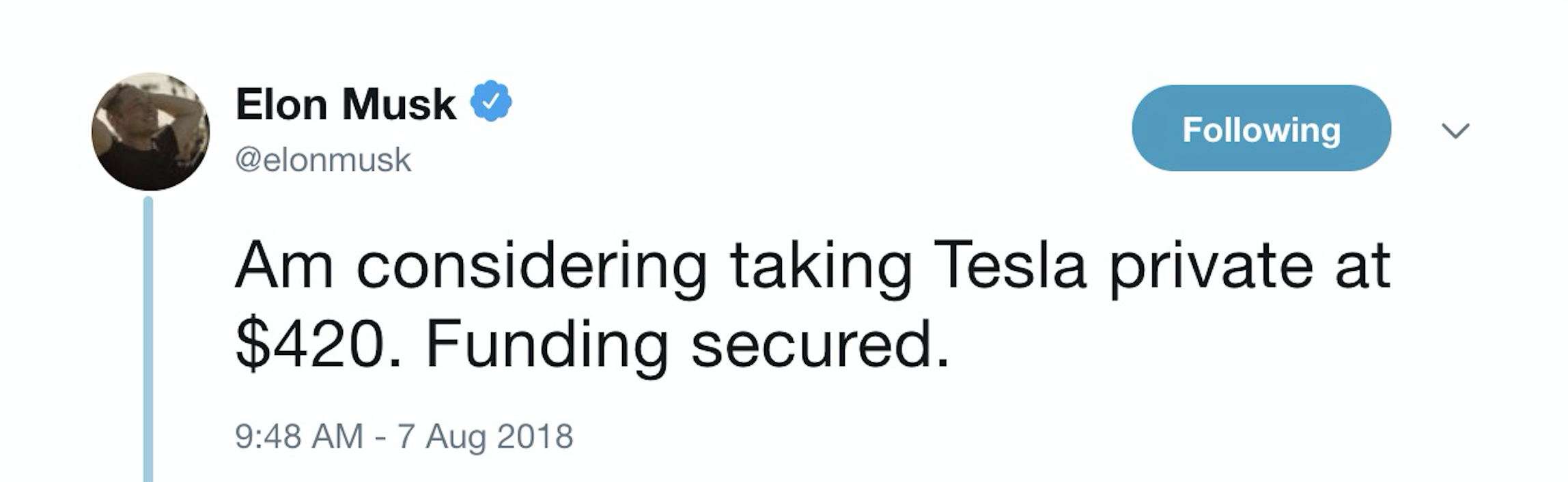

Around midday on August 7, Musk informed his 22 million Twitter followers that he was “considering taking [publicly-listed] Tesla private at $420. Funding secured.” This was followed by additional statements, such as “My hope is *all* current investors remain with Tesla even if we’re private. Would create special purpose fund enabling anyone to stay with Tesla,” “Shareholders could either to [sic] sell at 420 or hold shares & go private,” and “Investor support is confirmed. Only reason why this is not certain is that it’s contingent on a shareholder vote.”

Sometimes tweets are more than just tweets, and the U.S. Securities and Exchange Commission (“SEC”) – the government agency responsible for enforcing the federal securities laws and regulating the securities industry, as well as the nation’s stock and options exchanges – decided that this is one of those cases.

According to the lawsuit that the SEC filed against Musk on September 27 in a New York federal court, the aforementioned tweets contained “false and misleading statements,” and Musk “knew or was reckless in not knowing that each of these statements was false and/or misleading because he did not have an adequate basis in fact for his assertions.”

In the eyes of the SEC, Musk’s August 7 tweets are more than merely 280 character-or-less messages; they are violations of federal anti-fraud law, which “prohibits any act or omission resulting in fraud or deceit in connection with the purchase or sale of any security.”

By publishing the string of tweets, despite knowing “that he had never discussed a going-private transaction at $420 per share with any potential funding source, had done nothing to investigate whether it would be possible for all current investors to remain with Tesla as a private company via a “special purpose fund,” and had not confirmed support of Tesla’s investors for a potential going- private transaction,” Musk ran afoul of the law, according to the SEC.

The SEC asserted in its complaint that “unlike market participants reading his tweets, Musk knew that his ostensibly ‘secured’ funding was based on a 30 to 45 minute conversation regarding a potential investment of an unspecified amount in the context of an undefined transaction structure.”

Moreover, the SEC asserted in its complaint that “according to Musk, he calculated the $420 price per share based on a 20% premium over that day’s closing share price because he thought 20% was a ‘standard premium’ in going-private transactions.” While “this calculation resulted in a price of $419,” Musk stated that “he rounded the price up to $420 because he had recently learned about the number’s significance in marijuana culture and thought his girlfriend [singer Grimes] ‘would find it funny, which admittedly is not a great reason to pick a price.’”

Given Musk’s role as the Chairman and CEO of Tesla and the company’s view that (per the SEC’s complaint) “Musk’s Twitter statements [are] a ‘strong channel of marketing’” for the company and that “Musk acts as a ‘spokesman’ for Tesla,” Investors swiftly reacted to Musk’s tweet. According to the SEC, “From the time of Musk’s first tweet that day until the close of trading on August 7, Tesla’s stock price increased by more than 6% on significantly increased volume and closed up 10.98% from the previous day.”

The SEC further claims that “Musk’s false and misleading public statements and omissions caused significant confusion and disruption in the market for Tesla’s stock and resulting harm to investors.”

Within two days of the SEC filing suit against Musk, the Tesla CEO and Chairman agreed to settle the securities fraud charge. Tesla has also moved to settle in connection with the SEC’s charge that it failed to maintain required disclosure controls and procedures in connection with Musk’s tweets.

In accordance with the settlements, which are subject to court approval, Musk will be removed as Chairman of the Tesla board (something that stockholders have been pushing for for some time now) and the payment by Musk and Tesla of financial penalties, including a $20 million sum from Musk, who will remain in his role as CEO.

The suit and settlements come as a growing number of companies are using social media in traditionally unconventional ways, including as a way to make market-moving disclosures – which, in the past, were disseminated primarily by way of news releases distributed by services, such as Business Wire, or in formal interviews with media outlets.

As the New York Times noted this summer, this practice has been influx since “Reed Hastings, the chief executive of Netflix, broke ranks in 2012 and wrote on his Facebook page that the company’s video-streaming service had ‘exceeded 1 billion hours for the first time.’”

That instance led to what’s known as the Reed Hastings Rule. Following an investigation of the Netflix disclosure-by-Facebook, the SEC held that companies may, in fact, legally use social media platforms to announce key information in compliance with Regulation Fair Disclosure as long as investors have been alerted about which social media will be used to disseminate such information.

At the time, George S. Canellos, the agency’s acting enforcement chief, announced that “most social media are perfectly suitable methods for communicating with investors.”

* The case is U.S. Securities and Exchange Commission. v. Elon Musk, 1:18-cv-08865 (SDNY).

Share