After mentioning Environmental, Social, and Governance – or “ESG” – almost 100 times in the nearly 60-page S-1 that it filed with the Securities and Exchange Commission (“SEC”) in August, Allbirds is reigning its sustainability-centric declarations back a bit. In an amendment form filed with the securities and stock market regulator on Monday, the San Francisco-based brand best known for its lineup of eco-friendly wool trainers “removed several key references to the sustainability principles and objectives framework” that it outlined in its earlier filing, according to the FT, cutting the number of references to the Sustainable Public Equity Offering framework from 65 to 33.

Interestingly, Allbirds has limited its language about the Sustainable Public Equity Offering framework and its applicability to other companies, as well as to investors in order to help them “better identify public companies that are committed to sustainability and positive outcomes for all stakeholders,” and has reined in its use of “ESG” – albeit minimally – from 89 times in the October 4 versus 91 times in August. At the same time, it has increased the use of other sustainability-centric buzzwords. For instance, the brand mentioned “sustainability” 112 times in its August 31 S-1; it mentions the term 129 times in the October 4 filing.

Consumer & Regulator Attention

As the FT notes, the alterations to Allbirds’ S-1 come as the company has been facing “questions over the genuine sustainability of its business,” including a class action complaint accusing it of peddling “false, deceptive and misleading” ESG information in order to bank on the fact that “consumers are increasingly influenced” by companies’ business practices and prioritize companies that “act in a way that protects the environment, labor practices and animal welfare.”

In the complaint that she filed this summer in a New York federal court, plaintiff Patricia Dwyer specifically alleges that Allbirds’ life cycle assessment tool – which identifies the carbon footprint of each product – does not assess the environmental impact beyond the manufacturing of the shoes, themselves, such as the impact of “wool production, including on water, eutrophication, or land occupation,” and thus, “exclude[es] almost half of wool’s environmental impact.” The plaintiff also claims that the brand’s carbon footprint figures “are based on ‘the most conservative assumption for each calculation, skewing the calculations in its own favor,’ so it can make more significant environmental claims.”

Consumers and prospective class action members are not the only parties paying attention to companies’ ESG claims. The SEC confirmed in September that it is prepared to review and investigate public companies’ ESG disclosures. “While the SEC generally keeps matters under investigation confidential,” Winston & Strawn LLP attorneys Jonathan Brightbill and Jennifer Porter note that on September 22, the SEC revealed that its staff is sending letters to dozens of public companies in order to “seek more information about how climate change might affect their financial earnings or business operations.”

In addition to calling for information about “how climate change may physically impact companies and their operations, the SEC is asking companies to disclose how putative changes in climate change policies may impact financial performance,” per Brightbill and Porter, further solidifying the agency’s enhanced focus on climate-related financial risk amid its ongoing efforts to draft proposed regulations that would mandate enhanced – and uniform – climate and other ESG disclosures.

The Impact of ESG Disclosures

Despite skepticism about the veracity of its “eco-friendly” messaging and a growing focus on companies’ sustainability claims more generally, Allbirds has, nonetheless, emphasized its efforts on the sustainability front not only in its consumer-facing ad campaigns but in various regulatory filings leading up to its impending initial public offerings, as indicated by its S-1s. This comes in furtherance of a larger trend of companies playing up their consciousness credentials, including in IPO forms.

Just this week, Rent the Runway filed its own S-1 with the SEC, in which it touts “the importance of sustainability” generally, as consumers are “increasingly aware of the impact their choices are making on the environment and seeking more sustainable alternatives,” and the role that it plays in RTR’s model. The company states that its “platform allows brands to participate in the circular economy and provides a way for them to address the secondhand market in an aspirational way.” Meanwhile, in its August 24 S-1, eyewear brand Warby Parker – a public benefit corp. – stated, among other things, that “ESG is embedded in our core value and vision.”

(It is worth noting that while Warby Parker made mention of the importance of ESG to its model, the company’s S-1 was not jam-packed with ESG jargon, and for another point of reference, neither was the S-1 that luxury resale marketplace 1stDibs filed in May.)

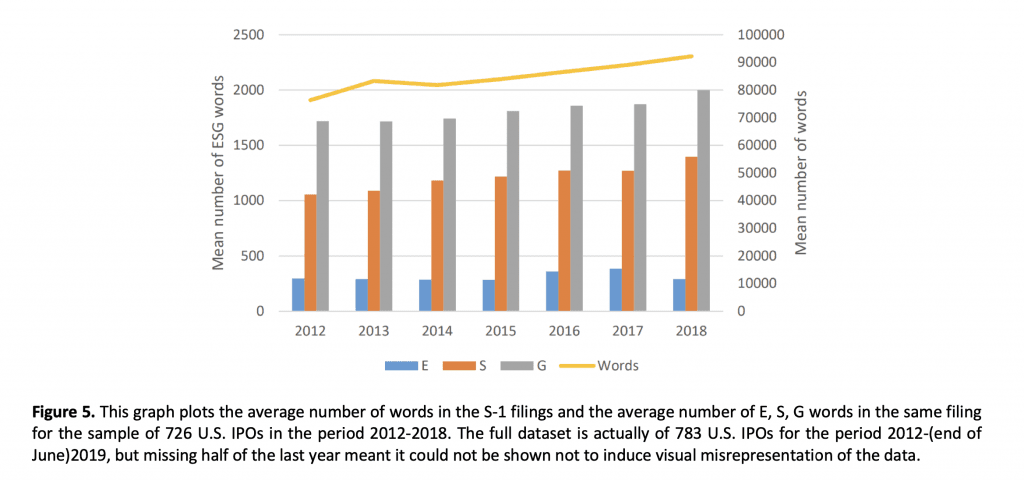

The overarching emphasis on ESG in companies’ pre-IPO regulatory filings is likely multi-purposed: it is aimed at luring top-notch talent to fuel expansion (millennial jobseekers are increasingly factoring in ethos and ESG efforts when gauging the attractiveness of a company), catering to sustainably-minded consumers, and potentially, boosting share prices. As for therelationship between ESG communications and IPO pricing and valuation, Alessandro Fenili and Carlo Raimondo took on this issue in a recent paper, in connection with which they examined the amount of ESG disclosures – or more specifically, the use of words related to the ESG topics – in the S-1 prospectuses for 783 Nasdaq or NYSE IPOs between 2012 and 2019.

In addition to determining that S-1 forms on average have “become more prolonged and detailed,” and that the same is also happening for ESG disclosures, which may be the result of “companies seeing it as more critical to disclose more, and possibly be more detailed, on such topics,” the two University of Lugano academics found that a “significant relationship” exists between companies’ ESG communications, and their IPO pricing and evaluation.

Specifically, Fenili and Raimondo found that there is a negative relationship between the amount of ESG disclosures – both as topics generally and in terms of the individual E, S, and G components – in S-1 forms and a stock’s underpricing, or the increase in stock price from the initial offering price to the first-day closing price. The reason for this, according to Fenili and Raimondo? “ESG disclosures usually bring positive benefits to the companies’ financial performance,” and thus, disclosing more of this information at the outset “diminishes the information asymmetry” between a company and investors. (Information asymmetry exists when one party to a transaction has more or superior information compared to another.)

The potential for benefits here is particularly relevant given that “more and more investors use ESG criteria to evaluate investment opportunities and IPOs, and also because they might want to avoid investing in companies associated with insufficient and inefficient environmental, social, and governance practices.”

While the relationship between ESG communications and IPO pricing and valuation that Fenili and Raimondo detected may not directly explain the rise in ESG disclosures in companies’ S-1 filings, their findings, nonetheless, “contribute to the other researchers’ results that the disclosure of ESG information … leads to higher corporate financial performance, here in terms of lower underpricing and more precise firm evaluation,” which may play some role in the drafting of regulatory paperwork. The researchers’ findings should, of course, be balanced against the need for companies to be careful when it comes to ESG claims thanks to rising SEC attention and a growing number of lawsuits, something that Allbirds is well aware of.

Share