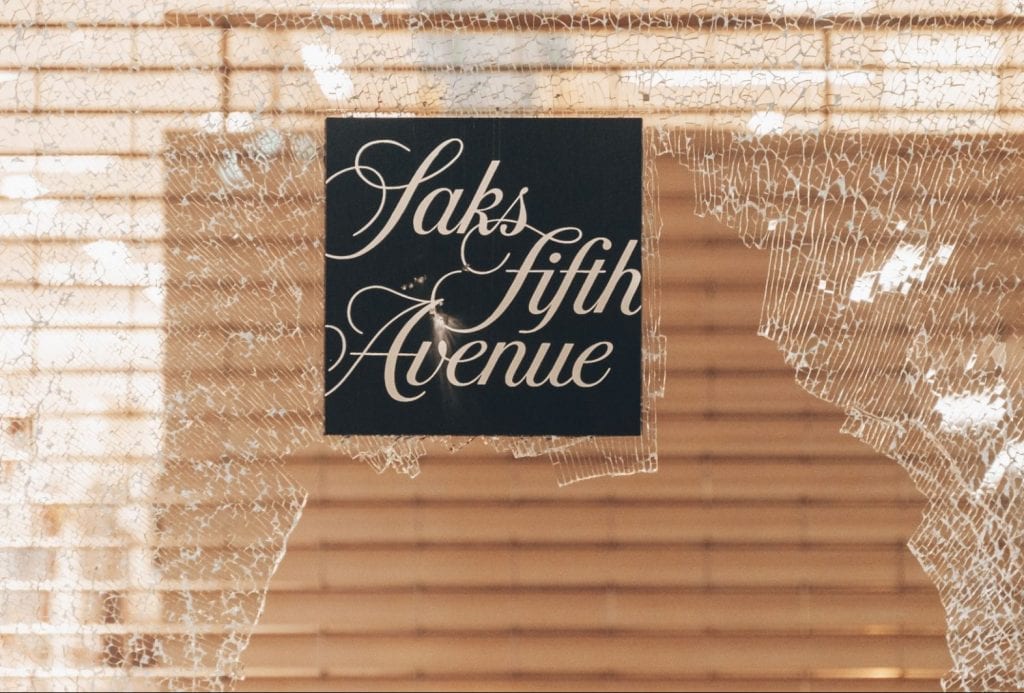

Retailers across the country are closing and boarding up stores as mass protests – some of which include looting – rage in the wake of the killing of Minneapolis man George Floyd by a police officer late last month. This weekend, stores on upscale shopping avenue Rodeo Drive in Beverly Hills were looted, with protestors breaking into stores and scrawling “F*ck the police” across the front of the Hermès outpost, and “Eat the rich” on the boarded-up Gucci store. Meanwhile, in New York’s Soho neighborhood, stores ranging from H&M and Zara to Rolex and Dior were raided by protestors, who left many of the shops virtually empty by Monday morning.

According to Reuters, many businesses, including giants like Apple and Target, are responding to such widespread protests by limiting their store hours or upending their brick-and-mortar operations entirety for the foreseeable future, citing safety concerns and their attempts to begin “recovery efforts.”

Aside from the larger impact of such social unrest on the market, which is likely to “hurt certain businesses like retailers and restaurants, and for it to further dent consumer and business sentiment,” Robert Phipps, director at financial advising firm Per Stirling, told Reuters, individual companies have been affected by protest-related damage and looting. In many cities, property damage, including shattered windows and broken security equipment, has been common for many companies’ outposts, while certain brands, such as Rolex and Hermès, for instance, have reportedly been robbed of costly merchandise in connection with the ongoing looting.

As for what businesses can expect in terms of recouping the losses associated with protest-related damages, many companies, particularly small ones, are at a loss. Sean Wotherspoon, the co-founder of Round Two, saw his a buzzy vintage boutique on Melrose Avenue looted this weekend, while his outpost in Richmond, Virginia caught on fire. Speaking to the Los Angeles Times, Wotherspoon said, “We are insured, but I don’t know what we are covered for, and I don’t know whether we are covered for losses in a civil disturbance. We may not know for a week or so.”

Every business’ insurance policy (and the benefits that come with it) varies, with “large chains like Target, Starbucks and Apple using their deep pockets to buy sophisticated policies that cover the entire chain for losses stretching into the millions of dollars,” while smaller companies are subject to a vastly different reality, particularly since “not all landlords require businesses to insure their inventory and equipment against loss, some local owners will end up having to cover all of the losses and repair costs on their own,” the Times aptly noted.

Despite the existence of such sweeping disparities between policies, there are generally two core elements to consider: immediate, physical damage to stores as a result of looting, and damages that come from the interruption of regular business operations.

In terms of the former, Womble Bond Dickinson’s Jonathan Reid Reich states that generally, most businesses have a commercial property or business-owners property policy, which likely contains “provisions that cover riot, civil insurrection property damage, and looting,” and “this would include physical damage to a building, as well as merchandise that may have been stolen” or otherwise damaged.

For companies that are in the possession of others’ property – whether that be repair shops, or potentially, consignment stores, such as Rebag and The RealReal, both of maintain outposts in New York City, where protests continue to gain steam, they “would likely need to have specific bailee insurance to cover the cost of replacement of a customer’s property which was damaged” or stolen.

Beyond immediate damage or theft, business may also suffer if restrictions stand in the way of normal operations, thereby, compounding the fact that many businesses are already struggling as a result of plummeting sales in light of the COVID-19 pandemic. If access to a business by either its customers or employees is restricted, for example, “a company may have a claim for business interruption or lost business income,” according to Reich, who notes that the “usual business interruption policy will only be triggered if there is sufficient physical damage to the business’s property such that the business must suspend its operations.” Given the significant damage and threat of future damage that comes with the looting that is occurring across the country, this threshold would almost certainly be met in places like New York’s Soho or Rodeo Drive, among other locations.

It is worth noting that while protections and triggering events will vary according to each company’s insurance policy, Insurance Information Institute encourages companies to …

– Contact your insurance professional and start the claims filing process;

– Take photos of any damage. A photographic record is useful when making an insurance claim;

– Make temporary repairs to prevent further loss from damage or looting; these costs are reimbursable under most policies, so save the receipts;

– Compile a detailed list of all damaged or destroyed property. Do not throw out damaged property until you meet with an insurance adjuster. If you have an inventory list, it will make the claims-filing process easier;

– If your business is forced to close temporarily or relocate because of direct physical damage to its premises, file either a business income (also known as business interruption) or extra expense claim, if you carry these coverages;

– To receive a business income settlement, document your net income and operating expenses, including payroll, both before and after the business was disrupted; and

– Keep detailed records of all business expenses and transactions as your business recovers.

Share