Farfetch is making headlines again this week. On the heels of reports that founder and CEO José Neves is looking to take the NYSE-listed company private, Farfetch – which has long bid to become the future of luxury fashion retail – revealed that it would not present its third quarter results this week, cancelled the corresponding conference call, and discounted all previously issued guidance. The news comes on the heels of the European Commission giving the green-light to long-anticipated deal between Farfetch and Richemont, one that is slated to see Richemont sell off a 47.5 percent “non-controlling” stake in Yoox-Net-a-Porter (“YNAP”) to Farfetch in exchange for a 10 to 11 percent stake in Farfetch and a 2.7 billion euro ($2.7 billion) write-down. (You can find a deep-dive into the deal right here.) The not-yet-closed transaction would position Richemont alongside other large Farfetch shareholders, including Alibaba, the Chinese e-commerce group, and Artemis, the investment company of Kering’s Pinault family. It would also set Farfetch up to acquire the rest of YNAP through a put and call option scheme.

As for what happens next, there seem to be a few immediate possibilities …

New deal or no deal – The chances of the parties seeking out a revised version of the deal they previously reached seems likely – if for no other reason than the changing value of Richemont’s intended stake in Farfetch. As of October, when the deal was approved by the EU Commission, UBS analyst Kunal Madhukar said that Richemont’s potential stake in Farfetch was valued at $615 million. That number has since dropped to $120 million. “Richemont would have to accept a significantly lower value for Yoox-Net-a-Porter or agree on new deal terms with Farfetch. Taking Farfetch private could facilitate a compromise on new terms,” Stifel’s Rogerio Fujimori told the FT.

At the same time, RBC Capital Markets analyst Piral Dadhania said in a note that Farfetch may also look to back out of the deal or renegotiate its terms.

If the deal falls apart, Richemont would likely seek out other options in its quest to deconsolidate YNAP. In the meantime, it would maintain control of its technology platform, which seems to be a key consideration in the mix. Richemont asserted in its Nov. 29 statement that “neither Richemont Maisons nor YNAP have currently adopted Farfetch Platform Solutions and they continue to operate on their own platforms.”

Privatization – In the event of a no-deal scenario or even if a new deal does come into fruition, Neves could go through with his reported privatization plan with the help of existing investors like Alibaba, for instance, and/or Richemont. The move would enable the company to restructure and refocus its business, which is necessary, per Bernstein’s Luca Solca, outside of the public view. (Farfetch selling off beauty brand Violet Grey and shuttering in beauty division seems to be one step in the direction of refocusing. Recent reports that LVMH, which owns a majority stake in the late Virgil Abloh’s brand, is looking to buyout the Off-White license from Farfetch (ahead of its renegotiation or termination window in 2026) are also worth noting here.)

As of now, Richemont seems unlikely to take this route, saying in a release on Wednesday in response to “recent media reports [about the privatization plan] and announcement made by FARFETCH,” Richemont “remind[ed] its shareholders that it has no financial obligations towards FARFETCH and notes that it does not envisage lending or investing into FARFETCH.” Bernstein Consumer Sector Specialist Maria Meiță said in a note that “this is excellent news for Richemont’s investors, despite the remaining overhang from YNAP, given Farfetch’s weakness was a key risk for the stock. Richemont is closer to reaching luxury safe haven category and joining LVMH and Hermès as our top picks for next year.”

This does not mean that Alibaba – which was at the center of in a mega-deal that first brought Farfetch and Richemont together back in November 2020 (but is absent from the latest round hence the swap-in of Emirati businessman Mohamed Alabbar) – might not be interested. Morningstar’s Jelena Sokolova said that she believes that “Farfetch’s extensive connections with luxury boutiques and brands across Europe could be valuable to a big Chinese online player” – although likely only if its “purchased at a distressed valuation (less than $500 million in market cap).”

Adding to such existing speculation, MarketScreener noted on Nov. 30 that business jets leased by Richemont and Alibaba had landed in London in recent days.

Bankruptcy for Farfetch – One other potential outcome could see Farfetch file for bankruptcy. The company’s name has been floated more than once in the past year by analysts and agencies, with credit reporting agency CreditRiskMonitor, for example, stating in a report this fall that Farfetch – which has incurred debt of upwards of $900 million – was among 10 other retailers that could be facing bankruptcy in 2023. As recently as Friday, a note from Welbeck Ash Research put Farfetch’s risk of bankruptcy at an “elevated” level following “a disastrous 12-24 months, as the post-pandemic bump in demand has dried up and the business comes to terms with minimal financial progress.” Despite revenue growing at a CAGR of 42%, Welbeck Ash states that “Farfetch has experienced limited margin improvement,” noting that the company is “burning cash at an alarming rate and is running out viable financing options.”

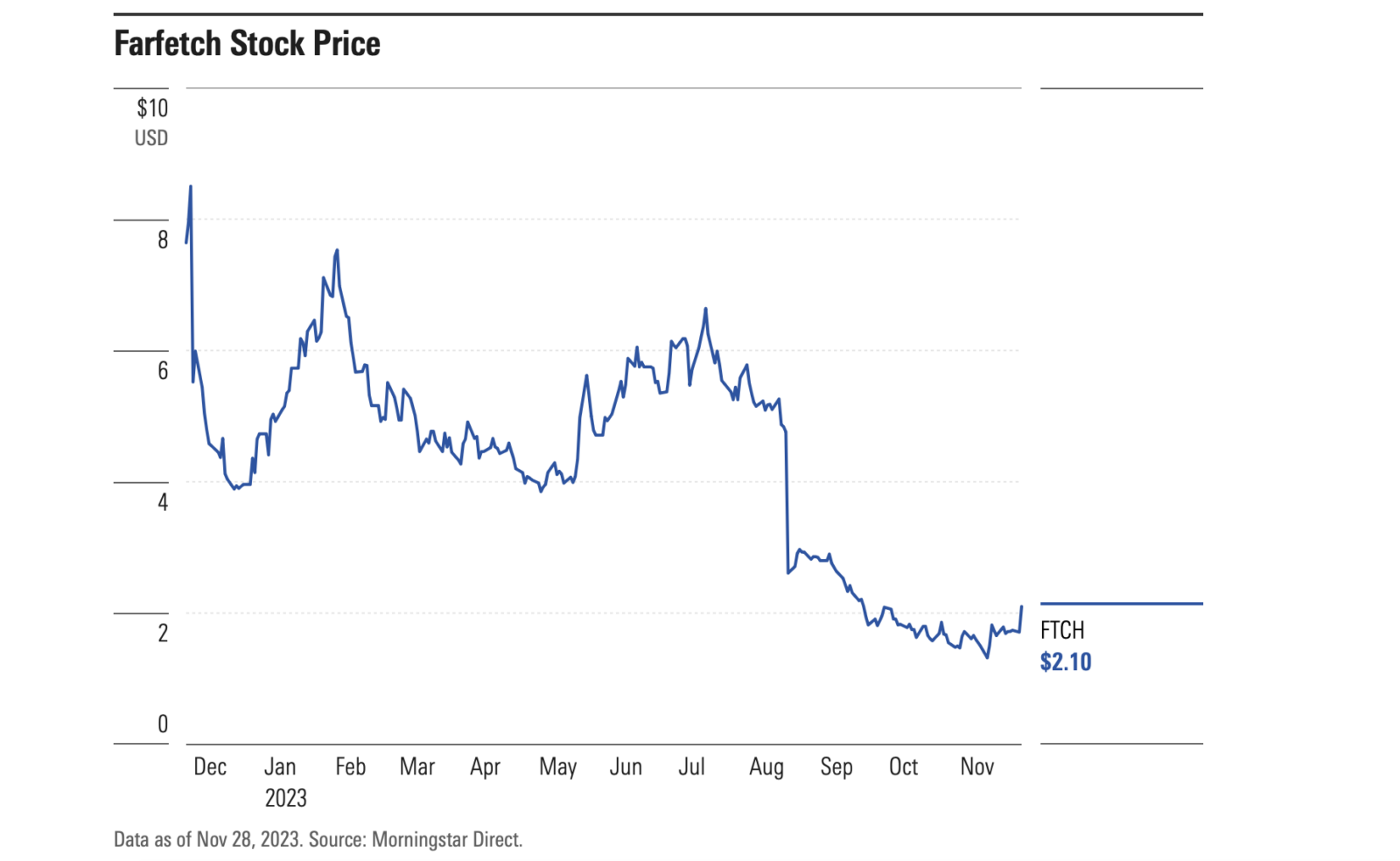

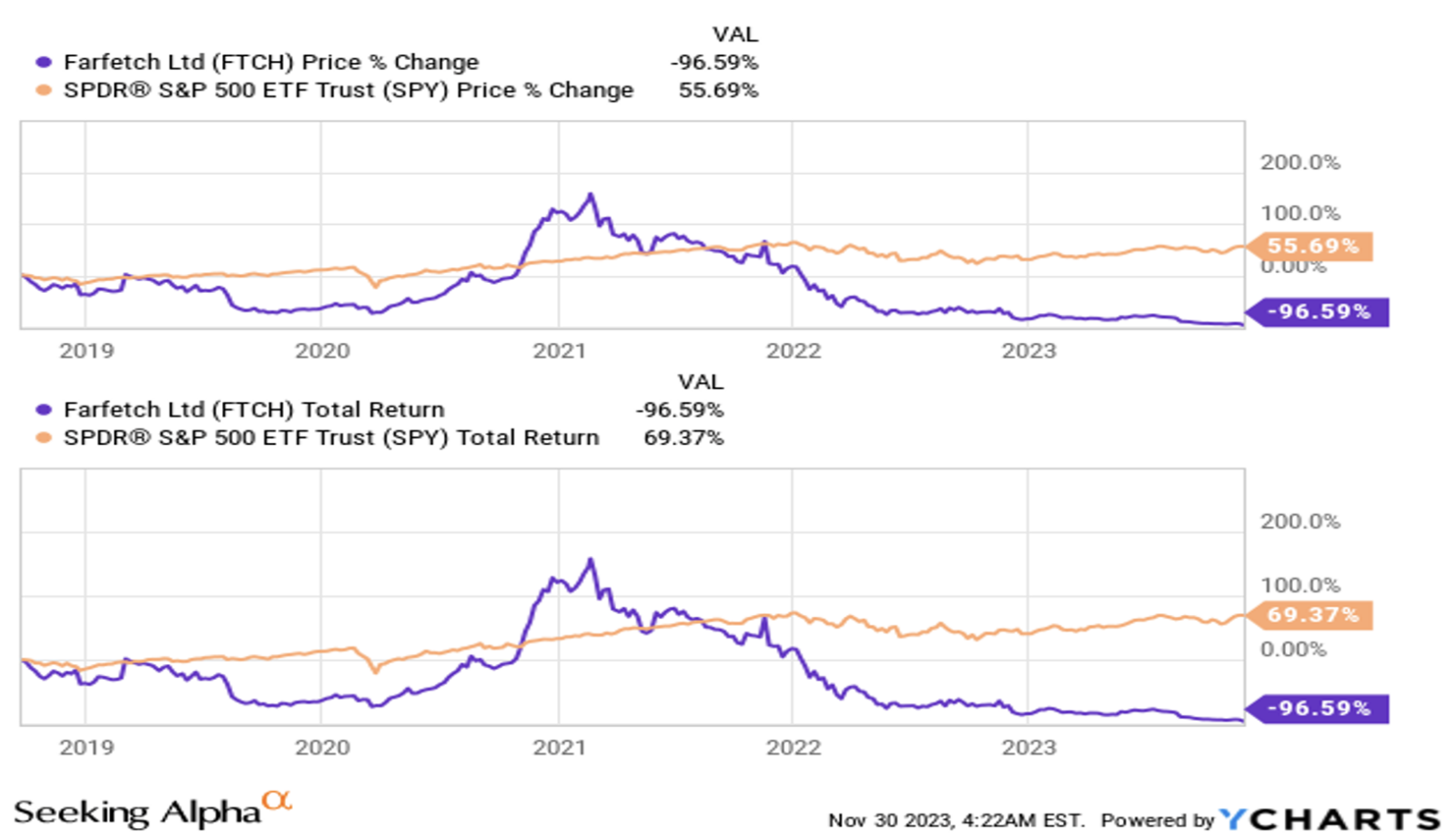

Rising debt comes as the company’s market value has fallen to just upwards of $400 million from its peak at $23 billion in early 2021. Meanwhile, its shares have lost more than 95 percent of their value since it listed on the NYSE in 2018. Even since it reached a deal with Richemont, the value of its shares has dropped from $10 to about $1.15.

Meanwhile, on the legal front … Farfetch is facing a securities class action suit, accusing it and a few executives (Neves, CFO Elliot Jordan, and Group President Stephanie Phair) of violating Section 10(b) of the Securities Exchange Act, which prohibits the use of any “device, scheme, or artifice to defraud” and imposes liability (via Rule 10b-5) for any misstatement or omission of a material fact regarding a security, and Section 20(a) of the Securities Exchange Act, which provides that “controlling persons” – like Farfetch’s execs. – can be vicariously liable for 10b-5 violations. (Sound familiar? Adidas is facing something of a similar suit at the moment.)

In particular, lead plaintiff Michael Ragan claims in his Oct. 20 complaint that throughout the class period (between March 9, 2023 and August 17, 2023), the defendants “made false and/or misleading statements and/or failed to disclose” … (i) Farfetch was experiencing a significant slowdown in growth in the U.S. and China; (ii) Farfetch also faced onboarding challenges impacting the launch of its Reebok partnership; (iii) Farfetch downplayed challenges it faced with respect to, and/or overstated its ability to manage, its supply chain and inventory; (iv) all the foregoing was having a significant negative impact on Farfetch’s revenue and GMV growth; (v) accordingly, Farfetch was unlikely to meet market expectations for its Q2 2023 financial results or its own FY 2023 revenue guidance; and (vi) as a result, the Company’s public statements were materially false and misleading at all relevant times.