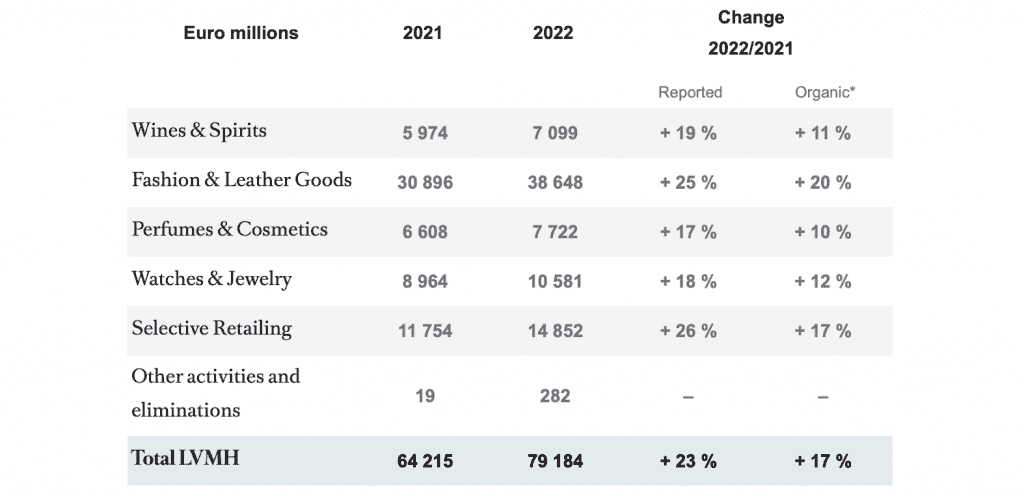

LVMH generated 79.2 billion euros ($85.9 billion) in revenue during 2022 and profits from recurring operations reached 21.1 billion euros ($22.9 billion), both up 23 percent from the year before. While all of the French luxury good conglomerate’s business groups achieved “significant organic revenue growth” over the year “despite the geopolitical and economic situation,” it highlighted Fashion & Leather Goods, which reached record levels, as well as the European, United States and Japanese marks, which “rose sharply, benefiting from strong demand from local customers and the recovery of international travel.” Asia was “stable” over the year due, according to LVMH, thanks to developments in the health situation in China.

For Q4, alone, LVMH’s revenue reached 22.7 billion euros ($24.65 billion), marking a 9 percent increase on an organic basis. “That marked a deceleration from the 20 percent growth recorded in the first nine months of the year,” per Reuters, with LVMH CFO Jean-Jacques Guiony attributing the fall wo the fact that China was “sharply down” during the last three months of 2022. “Everybody was sick, it’s as simple as that,” he said, noting that things are already looking up in 2023.

Delving into the full-year results for the Fashion & Leather Goods group, LVMH reported organic revenue growth of 20 percent to 38.6 billion euros ($41.9 billion) – and a profit of 15.7 billion euros (up 22 percent from 12.8 billion euros in 2021). 20 billion euros of the Fashion & Leather Goods group’s total revenue came from Louis Vuitton; this is the first time that the group’s marquee label reached the 20-billion-euro mark. Jefferies analysts said in a note on Thursday that they believe that taken together, Louis Vuitton and Christian Dior account for upwards of 75 percent of Fashion & Leather Goods revenue. Meanwhile, sales for Celine are now above 2 billion euros.

A key takeaway for Fashion & Leather Goods, according to LVMH chairman and CEO Bernard Arnault is global market share, with the individual division – which accounts for nearly 50 percent of LVMH’s total revenue – boasting a 17 percent share of the market, per Jefferies. That is up from an estimated 10 percent in 2018. “Louis Vuitton, Christian Dior, Celine, Fendi, Loro Piana, Loewe, and Marc Jacobs are all gaining market share globally and reaching record levels of revenue and earnings,” Bernstein analyst Luca Solca said in a note on Thursday. (As usual, Givenchy is missing from that list.)

In terms of balancing growth with market saturation, Arnault that the group’s products currently “sell nicely while remaining hard to find.”

Another business segment that is worthy of attention: Watches & Jewelry, which generated 10.6 billion euros ($11.5 billion) in revenue during FY 2022, up 18 percent on a reported basis, and a profit of 2 billion (up 20 percent from 2021). LVMH pointed to Tiffany & Co., which “had a record year, driven by its increasing desirability.” The New York-headquartered jewelry brand now has an EDIT of more than 1 billion euros – which has doubled since LVMH’s $15.8 billion acquisition of the the brand in early 2021. Meanwhile, Bvlgari “confirmed its strong momentum,” per LVMH, particularly in Europe, Japan and the United States, with “the iconic Serpenti line and the High Jewelry and High Watchmaking collections [being] the main growth drivers.”

In the latest indication that it is prioritizing hard luxury, LVMH management touted the group’s position aa “leaders in high jewelry worldwide.”

Looking ahead, LVMH says that it is “confident but vigilant [for FY23] due to current uncertainties,” stating that if the momentum coming out of China so far this year remains, 2023 will be an “excellent” year. In terms of China, LVMH management is “optimistic,” as while January has proven to be “volatile,” there are already indications of “a marked trend reversal” compared to December. Management also says that it expects some Chinese travel to Europe to resume in the second half of the year, but more meaningfully in 2024, which means that a return to FY19 levels will take time.

Share