The U.S. Securities and Exchange Commission (“SEC”) voted to adopt its highly anticipated climate-related disclosure rules for public companies on Wednesday, a move that will require companies listed on U.S. exchanges to disclose certain climate-related risks for the first time. The agency said in a statement that the final rules reflect its efforts to respond to investors’ demand for more consistent and reliable information about the effects of climate-related risks on companies’ operations and how theymanages those risks while balancing concerns about mitigating the associated costs of the rules.” Following the announcement, Chairman Gary Gensler stated that the rules “provide specificity on what companies must disclose, which will produce more useful information than what investors see today.”

In addition to laying out “clear reporting requirements” that will lead to “consistent, comparable, and decision-useful information,” Gensler further asserted that the new rules mandate that climate risk disclosures “be included in a company’s SEC filings, such as annual reports and registration statements rather than on company websites, which will help make them more reliable.”

What companies are affected: Companies that are listed on a U.S. stock exchange and those preparing to list on a domestic exchange (via a registration statement).

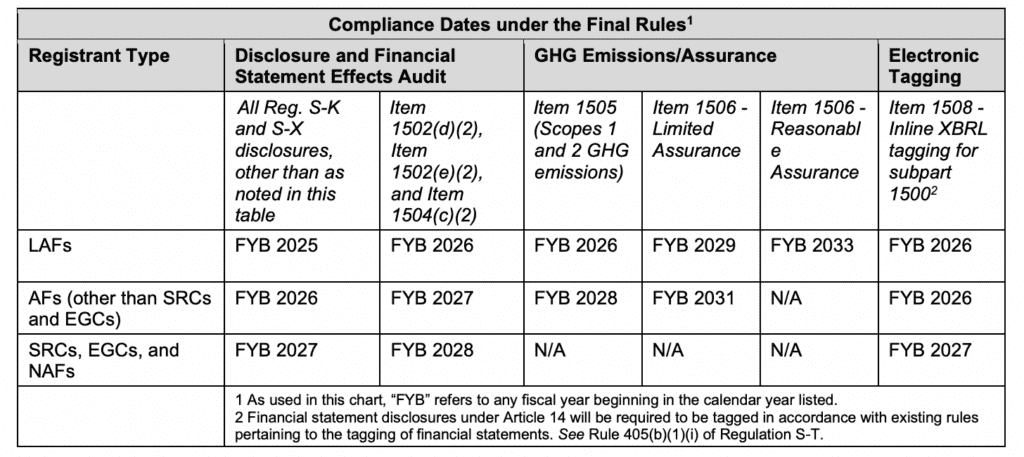

Timing: The final rules include a phased-in compliance period for all registrants, with the compliance date dependent on the registrant’s filer status and the content of the disclosure.

What needs to be disclosed: The SEC’s newly finalized rules will require listed companies to disclose material climate-related risks; activities to mitigate or adapt to such risks; information about the company’s board of directors’ oversight of climate-related risks and management’s role in managing material climate-related risks; and information on any climate-related targets or goals that are material to the company’s business, results of operations, or financial condition. Specifically, the SEC says that companies will need to report …

(1) Climate-related risks that have had or are reasonably likely to have a material impact on the registrant’s business strategy, results of operations, or financial condition;

(2) The actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model, and outlook;

(3) If, as part of its strategy, a registrant has undertaken activities to mitigate or adapt to a material climate-related risk, a quantitative and qualitative description of material expenditures incurred and material impacts on financial estimates and assumptions that directly result from such mitigation or adaptation activities;

(4) Specified disclosures regarding a registrant’s activities, if any, to mitigate or adapt to a material climate-related risk including the use, if any, of transition plans, scenario analysis, or internal carbon prices;

(5) Any oversight by the board of directors of climate-related risks and any role by management in assessing and managing the registrant’s material climate-related risks;

(6) Any processes the registrant has for identifying, assessing, and managing material climate-related risks and, if the registrant is managing those risks, whether and how any such processes are integrated into the registrant’s overall risk management system or processes;

(7) Information about a registrant’s climate-related targets or goals, if any, that have materially affected or are reasonably likely to materially affect the registrant’s business, results of operations, or financial condition. Disclosures would include material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or actions taken to make progress toward meeting such target or goal;

(8) For large accelerated filers (“LAFs”) and accelerated filers (“AFs”) that are not otherwise exempted, information about material Scope 1 emissions and/or Scope 2 emissions;

(9) For those required to disclose Scope 1 and/or Scope 2 emissions, an assurance report at the limited assurance level, which, for an LAF, following an additional transition period, will be at the reasonable assurance level;

(10) The capitalized costs, expenditures expensed, charges, and losses incurred as a result of severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, and sea level rise, subject to applicable one percent and de minimis disclosure thresholds, disclosed in a note to the financial statements;

(11) The capitalized costs, expenditures expensed, and losses related to carbon offsets and renewable energy credits or certificates (RECs) if used as a material component of a registrant’s plans to achieve its disclosed climate-related targets or goals, disclosed in a note to the financial statements; and

(12) If the estimates and assumptions a registrant uses to produce the financial statements were materially impacted by risks and uncertainties associated with severe weather events and other natural conditions or any disclosed climate-related targets or transition plans, a qualitative description of how the development of such estimates and assumptions was impacted, disclosed in a note to the financial statements.

What is absent from the reporting rules: Requirements that larger companies gather and report data on their suppliers and end-users of their products. “Scope 3” greenhouse gas emissions-specific requirements were included in the proposed climate disclosure rules that the SEC released in March 2022, but appear to have been slashed in an apparent effort to minimize the strenuousness of the disclosures and the resulting burden on reporting companies. The move to strike Scope 3 emissions reporting from the final rules has been met with pushback among some, namely, environmental organizations and democratic lawmakers.

The SEC’s final rules walk back on the applicability of Scope 1 and 2 emissions disclosure requirements, as well, as only large filers will need to report on these two scopes and only when they are deemed material.

Other Scope 3 reporting mandates: It is worth noting that companies may be exposed to more rigorous reporting requirements through other rules. The Corporate Sustainability Reporting Directive in the European Union requires certain EU and non-EU-headquartered companies (depending on their size) to make Scope 3 disclosures. At the same time, California’s Climate Corporate Data Accountability Act calls for Scope 3 reporting, as well.

The impact for apparel/retail entities: As for the impact of the SEC’s new rules on fashion/apparel entities, the rolled-back requirements with regards to Scope 3 emissions (i.e., those that result from the activities of entities not owned or controlled by the reporting organization, but that indirectly effect its value chain) will certainly be welcomed. After all, some 96 percent of the total emissions of fashion brands are in Scope 3, according to Reuters’ data.

Not a total loss, sustainability policy expert (and former foreign exchange trader) Kristen Fanarakis states that “increased reporting requirements around expenditures toed to companies’ climate goals, such as the purchase of carbon offsets to mitigate climate risks, will provide much needed insights.” This will be useful to gauging the efforts of companies across industries, including fashion, per Fanarakis, who points to Gucci-owner Kering as an example of one company previously pivoted to claiming carbon neutrality. This type of disclosure requirement “will give us better insight when it comes to how companies are arriving at their net carbon claims.”

Ultimately, while the SEC’s new rules might not require companies to report their emissions along the supply chain, Fanarakis contends that the new requirements – especially provisions that call on companies to identify any processes they have “for identifying, assessing, and managing material climate-related risks and, if [they are] managing those risks, whether and how any such processes are integrated into [their] overall risk management systems or processes” – should provide better insights for consumers, investors, and analysts, alike, “into how they are thinking about these risks.”

Share