Nike, Inc. reported revenue of $12.7 billion for the quarter ending August 31, 2022 (up 4 percent on a year-over-year basis), with President and CEO John Donahoe citing “the depth and breadth of NIKE’s global portfolio” as enabling the sportswear titan to deliver a “strong start” to 2023 fiscal year and helping it to “continue to manage through volatility.” Also on the up for Q1: NIKE Direct sales, which reached $5.1 billion, up 8 percent on a reported basis, and NIKE Brand Digital sales, which rose by 16 percent, led by 46 percent growth in EMEA. Sales momentum “even in this environment puts Nike head and shoulders above its peers,” Neev Capital managing director Rahul Sharma stated on Thursday.

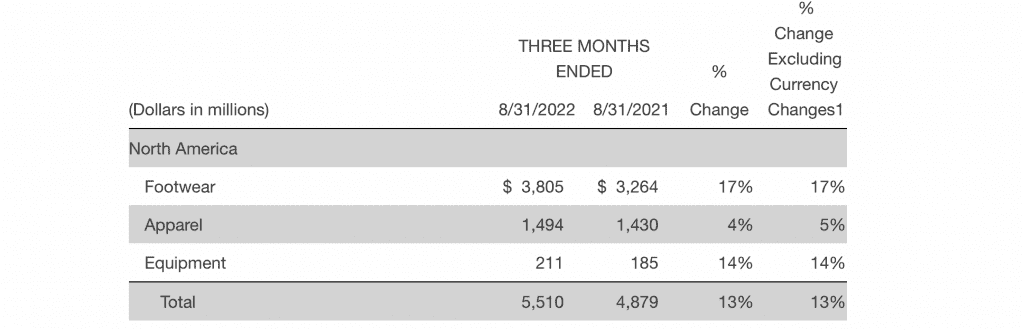

Geographically speaking, Nike revenue in North America rose 15 percent year-over-year to $5.5 billion, driven by a 17 percent increase in shoe sales. Sales in “Europe, Middle East & Africa” grew by 23 percent to $3.3 billion, again, helped along by an 18 percent rise in footwear sales. The tough market for Nike for the quarter was, of course, Greater China, where revenue fell by 16 percent compared to Q1 2021 to $1.65 billion, with apparel sales dropping 18 percent and footwear by 11 percent.

While revenues were up in Q1, the Swoosh is not without issues for the quarter. Profit was dragged down by “elevated freight and logistics costs,” and high inventory levels. Nike revealed that inventory was up by 44 percent on a year-over-year to $9.7 billion as of the end of Q1, “driven by elevated in-transit inventories from ongoing supply chain volatility, partially offset by strong consumer demand during the quarter.” Taken together, the result was a drop in gross margins, which fell by 220 basis points to 44.3 percent; analysts were expecting 45.4 percent, according to Refinitiv’s IBES data. At the same time, net income fell to $1.47 billion – down from $1.87 billion for the same period last year.

Looking ahead to Q2, Nike expects revenue will grow in “the low double digits,” while gross margin is expected to continue to drop – this time by about 350 to 400 basis points compared to Q2 2021. The company says it will focus on liquidating inventories in the second quarter, asserting that roughly 65 percent of its inventory backlog in North America is currently in transit.

The earnings call on Tuesday was dominated by analyst questions about inventory – no mention of RTFKT, Nike’s enduing Nikeland partnership with Roblox, non-fungible tokens, or virtual goods from Nike or analysts despite Nike’s continued emphasis on the virtual goods front. (Donahoe may have alluded to this, stating that Nike’s “growth is strengthened quarter by quarter,” thanks, in part, to “the fundamental shift in consumer behavior toward digital,” a comment that may extend beyond pure e-commerce activity to the metaverse, where Nike is actually driving some revenue.)

In terms of inventory, CFO Matt Friend stated that the issue is “predominantly apparel, [and] it is in North America predominantly.” Nike expects “total inventory to improve as we go from the first quarter,” and while North America is “obviously the geography where we’ve seen this most significant increase,” Friend said that the company “does expect to see it reduce.” As for what the Swoosh is doing to address excess inventory, Friend claimed that “because we have a portion of that inventory being seasonally out of relevance, we’ve decided to take that inventory and more aggressively liquidate it” – by way of in-house markdowns, as well as offloading it to third-party discount retailers – “so that we can put the newest and best inventory in front of the consumer in the right locations.”

As for the Chinese market, Donahoe is “enthusiastic,” saying that “Chinese consumers are emerging from these lockdowns with a real hunger for innovation, quality, and energized storytelling,” – and in particular, “hyper-localized innovation and storytelling.”

Reflecting on the company’s results, Sharma asserted, “Despite hysteria over a European recession, consumer-facing companies – from Nike to Zara – are doing very well there,” noting that “tough times may be coming but U.S. margin implosion is a huge contrast as companies seem to have managed U.S. inventory spectacularly badly.” For Nike, this has meant a rise in the number of days in inventory (136 days now versus 95 pre-Covid), along with a 14 percent spike in inventory “just over past quarter, despite big U.S. markdowns,” he says, with more inventory issues expected to follow.

Nike’s margin “will spike nicely once inventory is run down,” per Sharma, but that “will take time – we may not even be at peak inventory yet.”

Share