What does the future of the luxury segment look like? That is what The Independents recently sought to uncover by way of round-table discussions, expert interviews, and surveys of some 900 luxury goods consumers. The creative agency says that it “unearthed prominent shifts in the luxury landscape,” which it has presented in a lengthy study released this month. I dove into that nearly-60-page report – and highlight some of the key takeaways below – so that you don’t have to.

The current state of play: “Today’s global landscape, marked by economic volatility, social upheaval, environmental urgency, rapid digitization, and political change, has prompted a significant shake-up in luxury consumers’ expectations and behaviors. Across the six key markets surveyed, traditional drivers of luxury consumption are evolving from surface-level status symbols to deeper, more meaningful connections. What consumers desire is also changing – from designer clothes and handbags to appreciating assets such as art, watches and jewelry, and interior design, alongside experiences and travels that enrich their lives.”

What is challenging luxury today and tomorrow?

> Trends: Speed Over Process. “Our digital lives expose us to an endless stream of information: the consumer is overwhelmed, and brands need to work harder to stand out. As a result, ‘trust’ and ‘curation’ are critical words.” The Independents cautions, “While trend-hopping can place you on the map, it can be seen as lacking substance – especially in an age when the consumer is increasingly overwhelmed by content.”

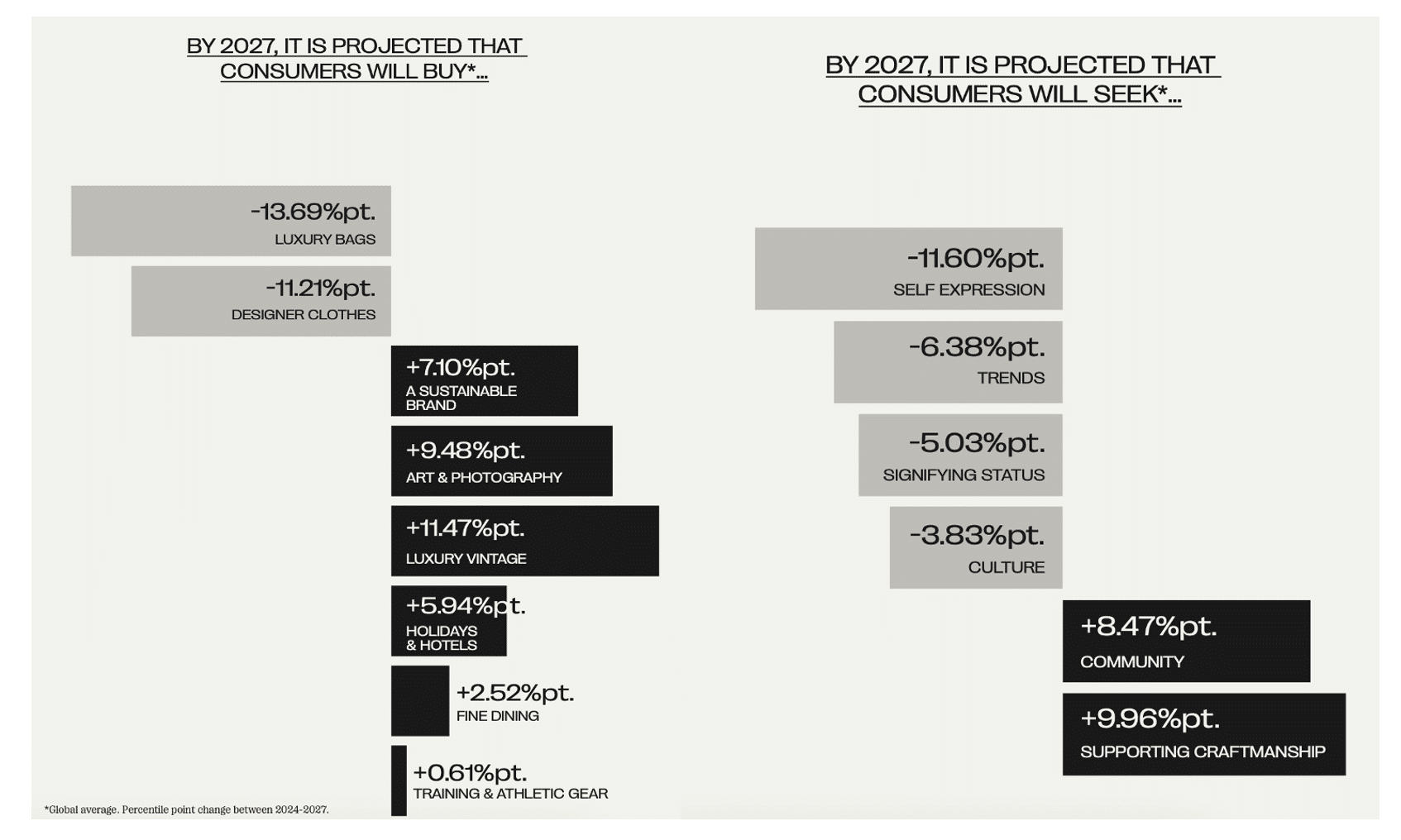

> Culture in Status Now. “As trends become more accessible, luxury consumption is increasingly driven by culture, where luxury serves not just as a signifier of status but as an entry point into a meaningful community. Our data indicates that while ‘Self-expression and identity’ and ‘Signaling status and wealth’ remain important, both are forecast to decline collectively by 16.63% by 2027. Instead, ‘cultural connect[s]’ has risen as a primary motivator towards luxury, growing 8.54% between 2019-2024.”

> Communities Become Carefully Curated. “Consumers want the purveyors of culture to reflect their community’s values and needs. As this strengthens, brands will have to extend beyond consumerism and product, into something deeper, where experience is central. ‘What are you offering them that they cannot buy?’”

What will consumers buy – and opt not to buy?

According to The Independents’ data points, there are “signs of retraction in the traditional luxury goods sector, suggesting that consumers could be beginning to feel overwhelmed or uninspired by categories such as luxury bags and apparel.” As such, leather good and apparel sales are expected to decline. “Overwhelmed by choice and rising prices, traditional luxury categories like handbags are forecast to drop 13.69% by 2027.”

Instead, The Independents asserts that luxury consumers are starting to spend more selectively, “placing greater value on objects that demonstrate creative excellence or have a history that displays our knowledge and individuality … Meanwhile, experiential sectors continue to boom.” Experiences over possessions has become “a catch-all phrase in luxury strategy and although this has had some influence on the slowdown in goods-centric verticals such as fashion, it is not the sole factor,” the report states. “Experience has been amplified as a commodity thanks to social media: experiences now have permanence. This shows no sign of slowing.”

“Holidays and hotels now bring status through social media. Experiences become as valuable as tangible objects because consumers are commoditizing them, making them visible to many more people than just those they are travelling with.”

What will drive consumer buying behavior?

“The consumer is hungry for difference: 42.55% of those surveyed said that by 2027, ‘A new designer doing something different’ would be the second most bank-able option for the future consumer.” At the same time, “self-expression remains a key motivator for consumers in luxury and it is the task of the design house to provide a vehicle for expressing identity through unique product offers.”

Who is doing this well? Miu Miu. The brand has consistently posted impressive growth: in Q3 it climbed by 105% year-over-year, contributing to 25 percent of sales for the Prada Group. “Much of its success can be attributed to its presence at various cultural events as a lifestyle brand with a clear point of view. However, its tangible growth has largely been driven by hit products, such as the micro skirt and its sneaker collaboration with New Balance. The Prada group’s report credits the success to ‘dynamic creativity that leads to increased desirability,’ a rare feat in a market of hyper-abundance.”

What about resale?

In a world where “the flux of micro-trends is causing trend fatigue and novelty is highly valued,” consumers are looking to luxury vintage as a vehicle for self-expression, alongside environmental and economic factors. The report “identifies a growing desire for collection over consumption, with the goal of curating a wardrobe of archival pieces and iconic designs, which are vehicles for individualism. As a category, luxury vintage is forecast to grow by 11.47% between 2024–2027, with more than 38% of those surveyed saying it would be their priority category by 2027.”

In the wake of a failed deal between Tapestry and Capri Holdings, a number of new deals are in the works. Capri, for one, is said to be looking to off-load Versace and Jimmy Choo (in an apparent effort to focus exclusively on its Michael Kors brand), while WHP Global is snapping up Vera Wang and Saks Fifth Avenue’s owner HBC is getting closer to a deal to take over fellow retailer Neiman Marcus.

Interestingly enough, elsewhere in the market, a deal gone awry has prompted new litigation as seen in Albertsons’ newly unsealed complaint against Kroger. Lodged with Delaware’s Chancery Court and unsealed this week, Albertson’s lawsuit follows closely from a block of its $25 billion merger with Kroger.

Just like Tapestry and Capri, Albertsons and Kroger pulled the plug on their deal after the proposed merger was opposed by the Federal Trade Commission and then blocked by more than one court on anti-competition grounds. However, in an alternative scenario of how such a deal could end up in the event that the parties do not maintain peace following the implosion of their deal (which is how things seem to have ended up with Tapestry and Capri), Albertsons and Kroger will now face off against one another in the wake of taking on regulators together in order to save their proposed deal.

> In a nutshell: Albertsons alleges that Kroger “derailed the merger after suffering a classic case of buyer’s remorse … after a negative market reaction to the Merger and falling post-pandemic profits, and it decided it would go through with the deal, if at all, only on terms far more advantageous to Kroger than those for which it had bargained.” Instead of complying with its contractual obligations to exercise “best efforts” and to take “any and all actions” to get the merger approved, Albertsons claims that “Kroger prioritized its own financial self-interest and refused to do what was required to close the deal.”

Kroger, therefore, breached the merger agreement “at least by: (a) Failing to divest an adequate package of up to 650 stores to satisfy regulators’ concerns; (b) Failing to divest an adequate package of non-store assets (like banners, technology, and private label brands) to satisfy regulators’ concerns; (c) Delaying its engagement with regulators and failing to respond adequately to regulators’ questions and concerns; (d) Mismanaging the process of identifying a divestiture buyer; and (e) Failing to cooperate with Albertsons in good faith.”

What to Expect from the Trump Administration: Not only are the most recent deals coming out of the fashion industry unlikely to warrant regular scrutiny due to the size of the companies and the combined value of the deals (save for Tapestry, Capri, that is), the incoming Presidential administration is expected to be much more pro-deals than the FTC under Biden. Because Trump has not expressed frustrations with many retail companies, Chris Sagers, an antitrust professor at Cleveland State University told Modern Retail, which noted that since the election, investors have been enthusiastic about the prospect of less regulation and more opportunity for M&A. Sagers says that he does not expect many retail deals other than those to the degree of Kroger-Albertsons to be challenged. “What I would predict is we will have pretty routine enforcement in retail.”

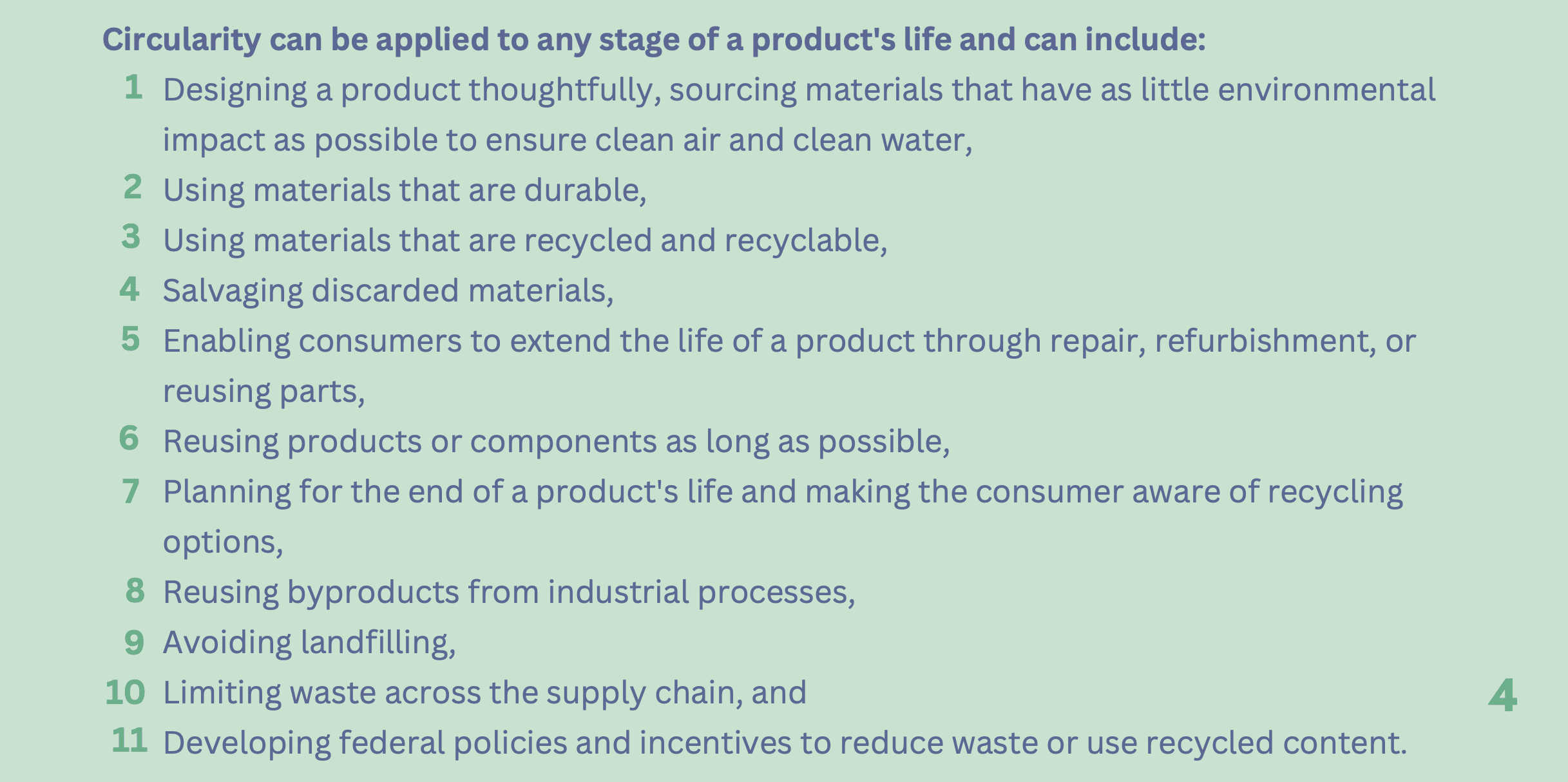

The U.S. Circular Economy Coalition recently released its first Federal Circularity Audit and Report to identify how the U.S. government is encouraging increased adoption of circularity practices by corporations and companies operating in the U.S. The report provides a snapshot of how the federal government is participating as an entity and encouraging others to participate in a circular economy, and what the federal government’s level of maturity looks like when it comes to participating in the circular economy.

> The Bottom Line here: “The U.S. federal government values the importance of promoting circularity. Of the five agencies we reviewed, all had incorporated circularity to some degree into their program activities. With grants in particular, the Inflation Reduction Act of 2022 and the Save Our Seas 2.0 Act authorized and released billions of dollars to agencies that ultimately support circularity goals. Our review, however, reveals opportunities for enhancing the federal government’s approach to circularity to further increase efficiency, promote circularity, and help the U.S. emerge as a world leader in promoting a circular economy.”

The Coalition also set out three key recommendations for the federal government …

> Improve Circularity Efforts to Achieve Meet Big Goals. “Harnessing the power and reach of supply chains in reusing materials can keep our economy strong while reducing harmful emissions and streamlining the volume of materials headed to landfills;”

> Better Coordinate Circularity Activities and Centralize Information. “The adoption of a government-wide definition for circularity would create clarity both within the federal government, to state and local governments and the private sector, and appointing circularity leads at each agency to collaborate would help establish consistency and accountability;” and

> Promote Worldwide Circularity through International Engagement. “The U.S. federal government should also recognize the value of a circular economy and demonstrate that recognition by building circularity into its own climate action plans.”