Counsel for Tapestry and Capri Holdings alerted the U.S. Court of Appeals for the Second Circuit that they were withdrawing their appeal to the preliminary injunction issued by the Southern District of New York, marking the latest legal development in the since-broken-down merger. The proposed $8.5 billion merger to combine Tapestry-owned Coach, Kate Spade, and Stuart Weitzman, and Capri Holdings’ Michael Kors, Versace, and Jimmy Choo will not ultimately come into fruition; the deal fell apart following the SDNY’s injunction order.

Nonetheless, there are still takeaways for companies (in fashion and beyond) that are eyeing M&A. Among them? Milbank’s Fiona Schaeffer, Adam Di Vincenzo, Richard Parker, Grant Bermann, James Weingarten, and Ari Blask point to the following takeaways …

> The Tapestry decision confirms the truism that the antitrust agencies and factfinders place significant weight on ordinary course documents. Companies negotiating deals with significant competitive overlaps should undertake careful review of their own documents and push for robust antitrust due diligence during negotiations.

> Expert opinions that are at odds with the ordinary course documents and other evidence are less likely to be persuasive. Factfinders rely on experts to tie together the evidence into an analytical framework.

> In general, we expect enforcers to rely on this decision to urge courts to discount executive testimony about post-merger plans. The Tapestry court’s discounting of “hollow promises from company executives” to maintain competition post-merger stands in contrast to other cases in which courts credited executive testimony about post-merger behavior. There is a spectrum of evidence supporting “fixes” that merging parties can offer to rebut alleged anticompetitive effects.

More on mergers and competition considerations coming soon. I have a few pieces currently in the works.

A jury sided with Penn State University this week, finding that Vintage Brand willfully violated its trademark rights by selling merchandise featuring retro Penn State logos without the university’s authorization. The jury awarded Penn State $28,000 in damages on the basis that consumers are likely to be confused as to whether Penn State was connected to or otherwise endorsed the products bearing its logos (some pictured below). In response to the case, which Penn State filed in a federal court in Pennsylvania back in 2021, Vintage Brand argued that consumers would not automatically assume that there is a connection between its merchandise and Penn State.

In addition to siding with Penn State on the issue of potential consumer confusion (the crux of a trademark infringement claim), the jury also handed Penn State a win in finding that Vintage Brand’s use of the logos at issue was not merely ornamental or aesthetically functional, and thus, the logos function as trademarks. Vintage Brand – which offers up vintage sports t-shirts, sweatshirts, and sports apparel for college, NFL, MLB, and NBA teams – had argued that that the imagery on the t-shirts and other products at issue primarily serve “an aesthetic purpose wholly independent of any source-identifying function.”

The jury’s November 21 verdict follows from U.S. District Court for the Middle District of Pennsylvania Judge Matthew Brann’s 2022 refusal to dismiss Vintage Brand’s counterclaims in which it argued that its use of the Penn State logos was ornamental and not infringing.

Beyond that, the outcome is worth noting, as that the jury was seemingly unpersuaded by arguments from Vintage Brand that disclaimers on its website “make clear to consumers that Vintage Brand is not affiliated with [Penn State].” We can add this to our larger tracking of disclosures in the trademark context: We considered this issue this week in connection with a recent Rolex summary judgment win, in which the court focused heavily on the defendants’ disclaimers about the modified nature of the watches, and before that, we took a deep dive into disclosures/disclaimers in the resale and up cycling contexts.

Penn State’s win is also notable in light of the number of cases that have been waged against Vintage Brand by the likes of Purdue, Stanford, and UCLA on similar grounds; although, none of those cases made it to trial.

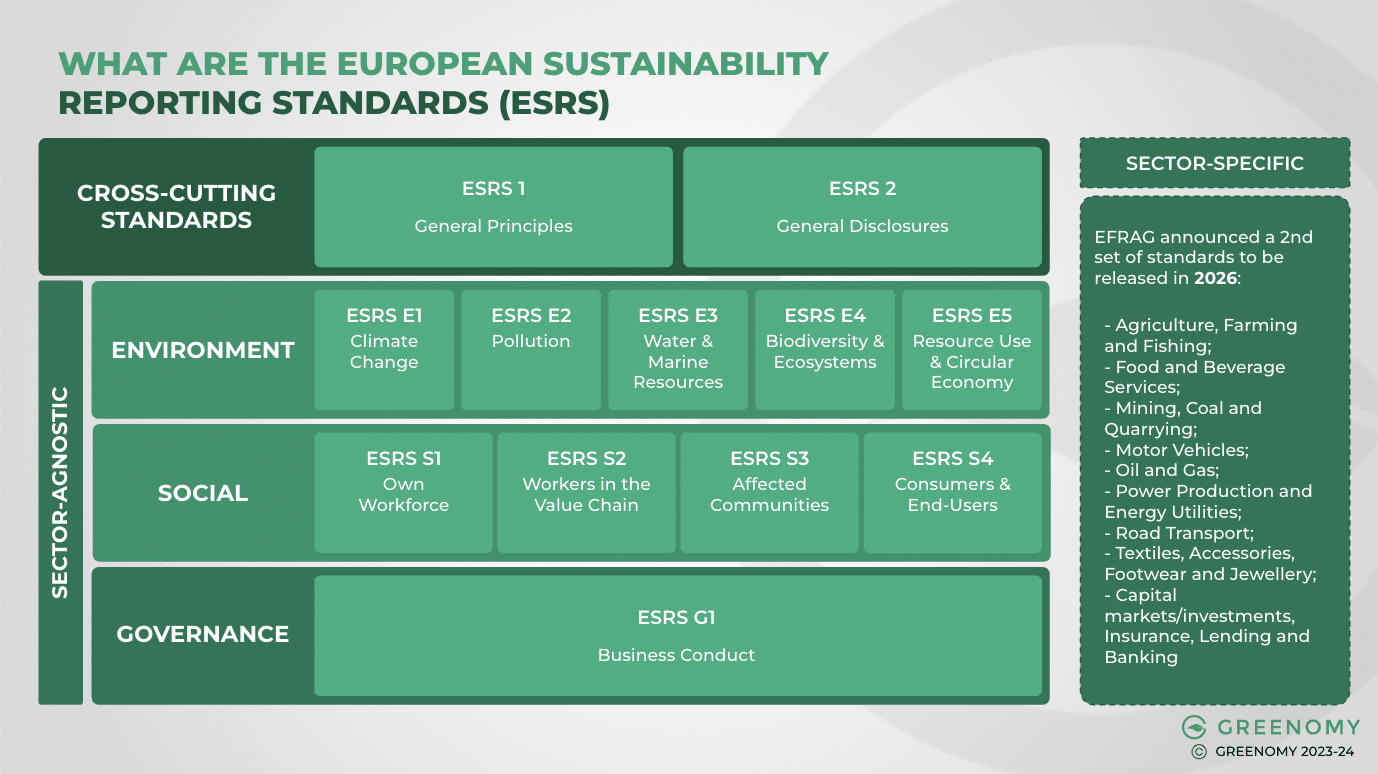

The European Union is moving forward with drafting sustainability reporting standards for non-EU based businesses. The standards, mandated by the Corporate Sustainability Reporting Directive (“CSRD”), will require companies to report how their business impacts – and is impacted by – Environmental, Social, and Governance issues. CSRD reporting will be required for non-EU based companies if they generate a minimum of €150 million net turnover in the EU, and have either: an EU subsidiary in scope of CSRD; or an EU branch with a minimum of €40 million turnover.

The first draft will be released in early 2025 and will go into effect in 2028. In the meantime, the European Financial Reporting Advisory Group’s (“EFRAG”) Sustainability Reporting Board, which is responsible for overseeing the CSRD reporting standards, recently published draft non-EU Reporting Standards.

Non-EU companies are expected to have to follow the same standards as EU companies with one proposed exclusion: non-EU based businesses will be able to avoid reporting: (1) “sustainability‑related “impacts connected with operations and revenues other than those connected with EU customers” (whether indirect or direct); and (2) financial materiality at group level.

In a nutshell: “This narrows the focus on actual GHG emissions by the company, as well as the policies and actions relating to climate change. EU based companies will need to calculate the financial risks associated with climate change, like the cost of natural disasters, and the financial opportunities, like investing in green initiatives. Those calculations are typically reported in the company’s home jurisdiction, if that jurisdiction requires sustainability reporting,” Forbes’ Jon McGowan put it.

As for EU companies subject to the CSRD, reporting standards as of now are as follows …