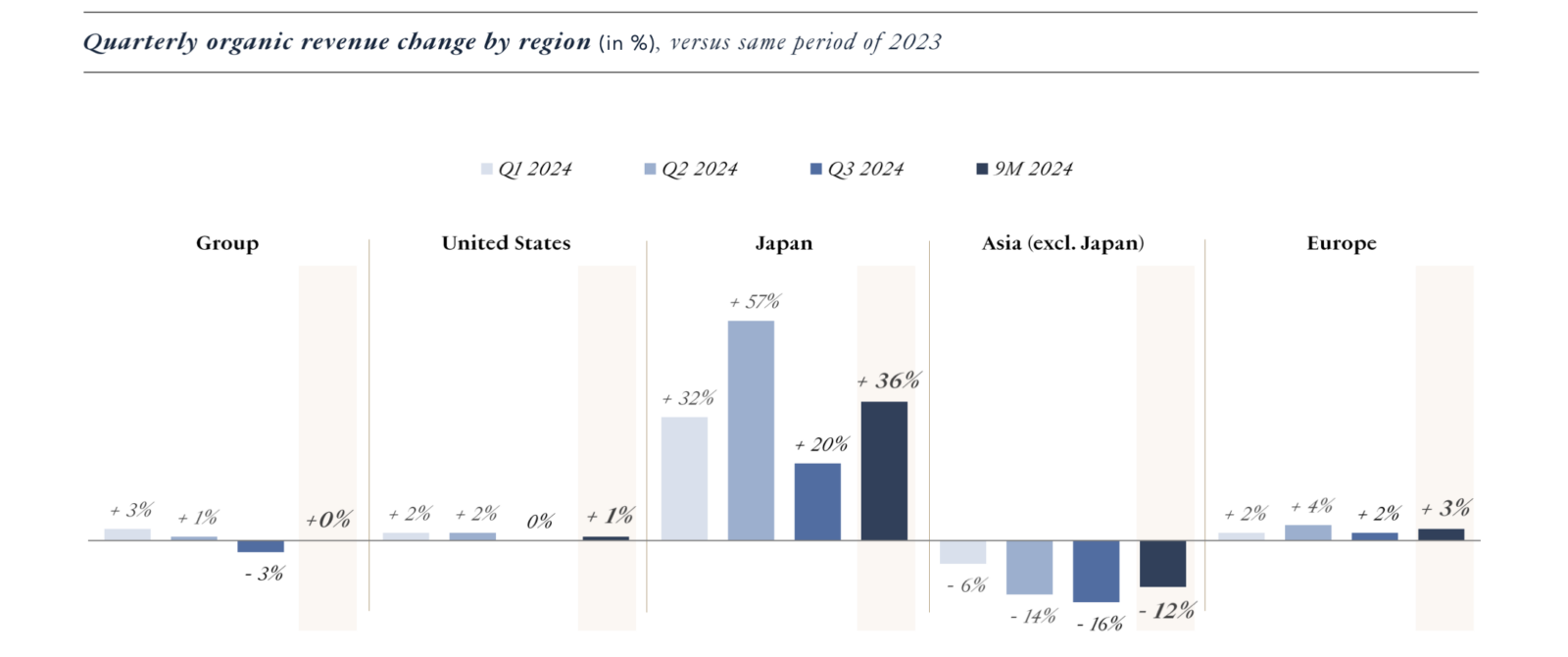

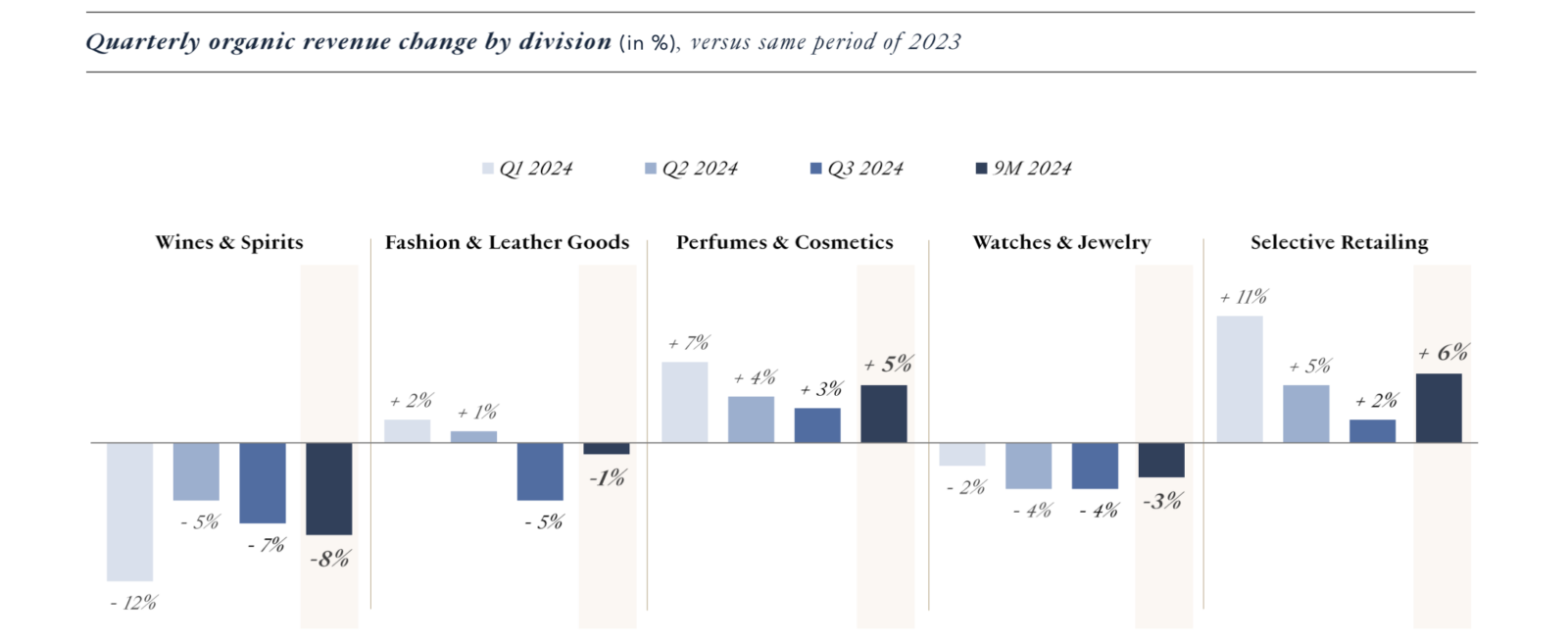

Some of the biggest news this week came in the form of disappointing Q3 results for LVMH, a report that is expected to set the tone for other companies’ impending earning reports for the third quarter. The French luxury titan said that it generated 19.08 billion euros ($20.8 billion) in revenue for the three months ending on September 30, a 3 percent drop from the same quarter last year (on an organic basis). LVMH’s fashion and leather goods division, which houses the Louis Vuitton, Dior, Loewe, and Celine brands, among others, reported a 5 percent decline in revenue year-over-year, the high-performing division’s first decline since 2020.

There are a number of interesting factors at play when it comes to LVMH’s lack of luster in Q3. LVMH management explained that a large part of its disappointing quarterly performance – which “badly missed” analyst expectations (as Bernstein’s luxury goods senior analyst Luca Solca put it) – was the fall in consumer confidence in China. While demand for luxury goods is not an issue with consumers in China, per LVMH, the group’s leadership said in a call with analysts this week that “consumer confidence is at a Covid-era all-time low.”

“Domestic demand has been especially moribund” in China, according to Solca, who noted that LVMH’s management “expects the wealth creation that drove luxury growth to resume in time, with the government’s intent helpful.” At the same time, it is difficult not to consider the narrative that has been permeating the press: Price-conscious consumers are turning to dupes (or “pingti”) amid China’s economic slowdown – from copycat Lululemon leggings to handbags that mirror those from Prada and of course, Louis Vuitton. The impact of the rising adoption of dupes among consumers should not be dismissed here.

> The word pingti refers to “a range of products, including dupes, counterfeits, and products that come from the same factories as their branded counterparts — as long as the price is more affordable than a much higher-end product,” per Business Insider.

> Is there a real impact here? At least some analysts say yes. Laurel Gu, a Shanghai-based director at market research firm Mintel, for instance, says that the rise in demand for dupes reflects “a significant change in the shopping habits of Chinese consumers.” Mintel recently revealed that searches for dupes have tripled between 2022 and 2024, which it says is indicative of a meaningful shift in consumer behavior.

For a deeper dive into the state of dupes, you can find that right here.

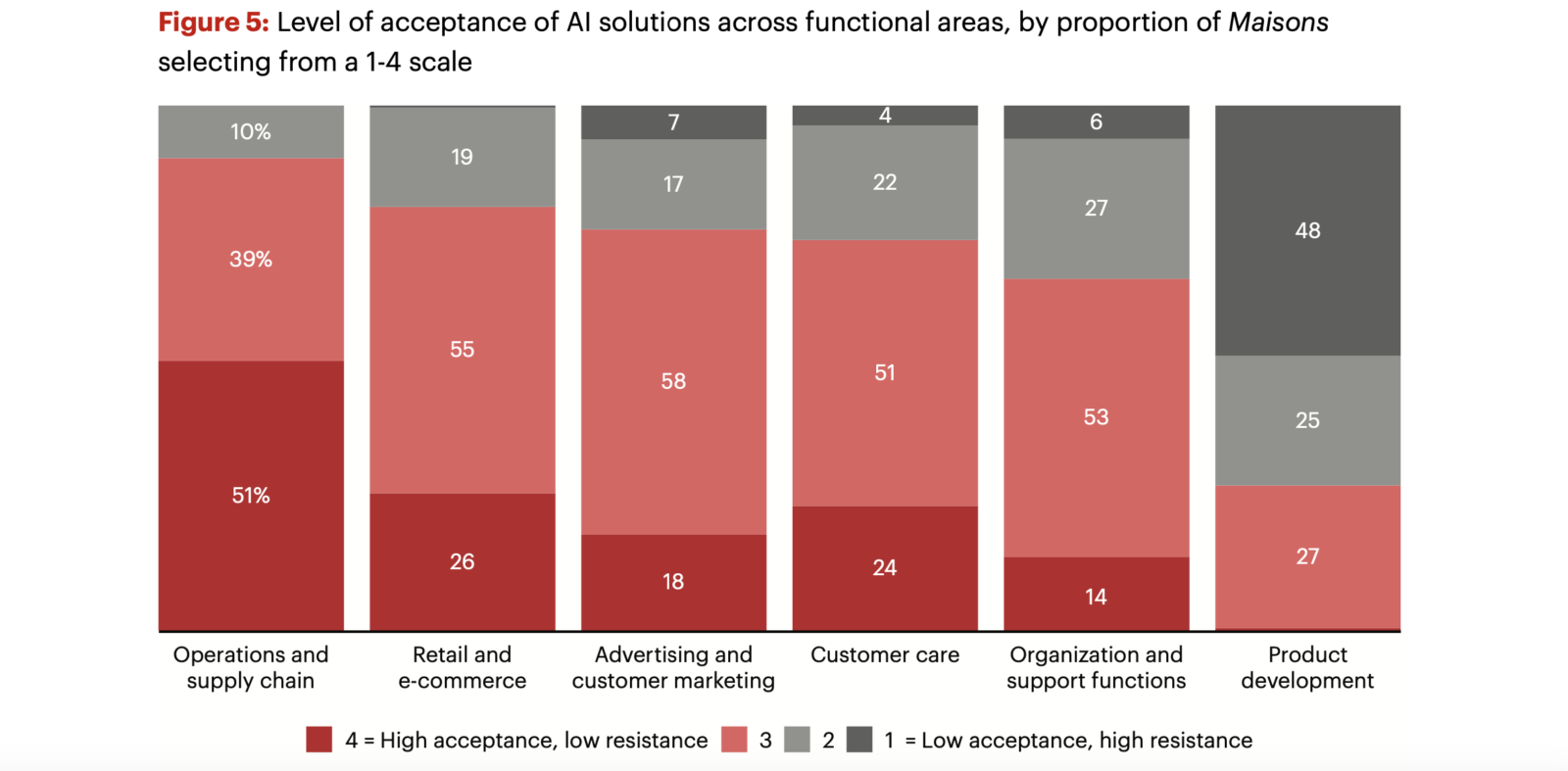

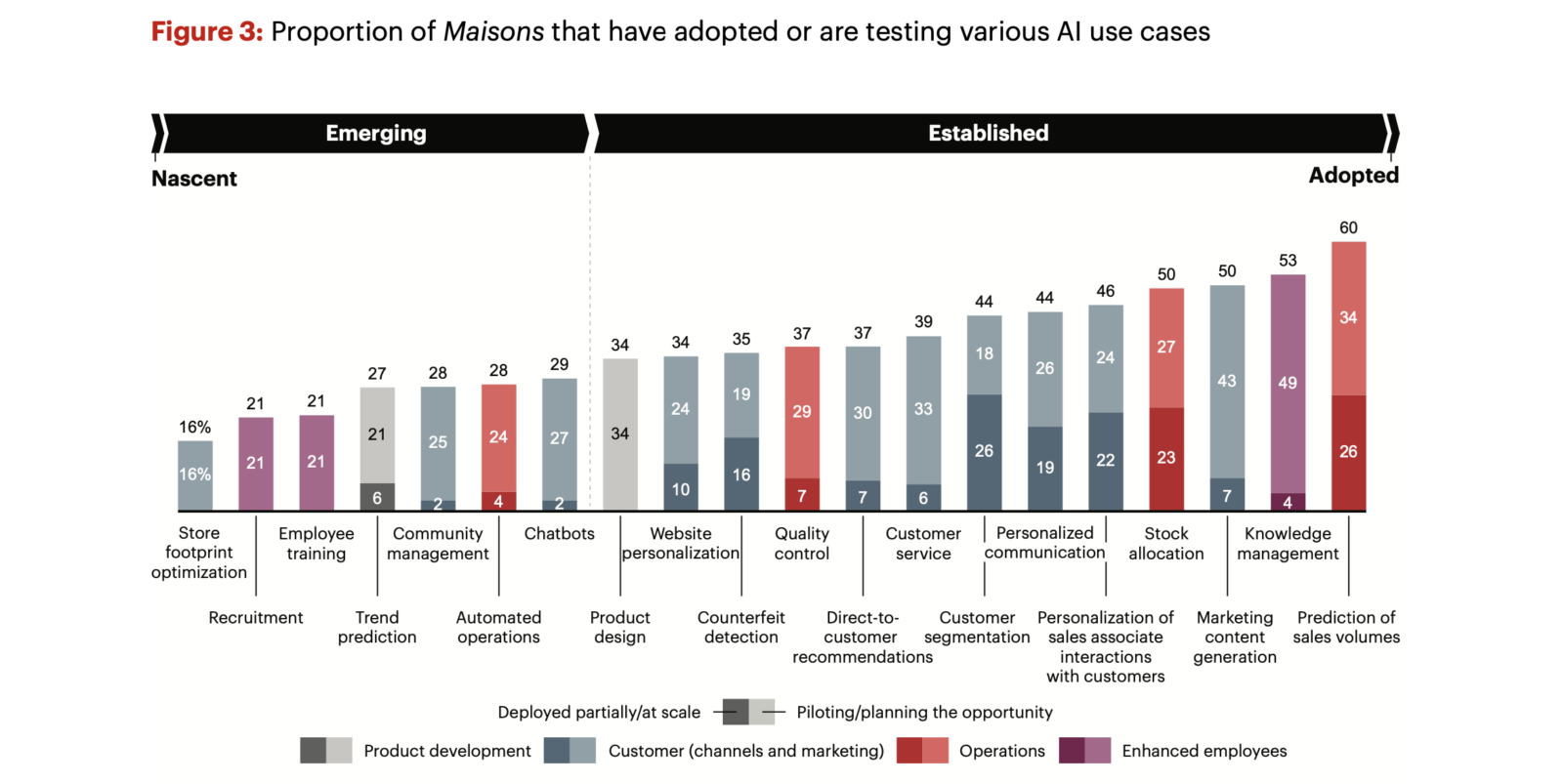

Bain released an AI-centric report this week, finding that since analytical AI was first used in the luxury market more than five years ago, adoption of AI solutions has remained targeted and quite limited. On average, fewer than two of the 20 use cases examined in our study have been adopted by members of the Comité Colbert, the trade association for the French luxury industry, and none have been adopted by more than 30% of these luxury brands. The use cases supported by analytical AI are among the most widely deployed by the brands.

However, that may not be the case for long, as numerous pilots are underway and brands are currently testing or planning more AI uses according to Bain, which expects AI adoption to accelerate over the next 12–24 months. As for what those uses look like, 60 percent of the brands surveyed said that they have adopted or are testing AI-based sales forecasting solutions and 50 percent said they are looking to use AI for stock allocation.

> Looking ahead: In the future, Bain expects that AI algorithms will also be able to “incorporate public data that affects companies’ operations, such as changes in customs regulations, import taxes, and complex climate or transport conditions. This predictive capability will enable brands to engage in proactive discussions with their suppliers to prevent supply disruptions and manage supply chain risks effectively.”

> AI & counterfeits: Despite the resistance to customer-facing AI applications, Bain found that “some solutions based on analytical AI that don’t involve key moments in the sales process are being embraced by brands. For example, The Ordre Group, in partnership with several brands, has developed a solution called Authentique that enables customers to know in a matter of seconds whether they are looking at an original product or a counterfeit. The luxury goods sector has embraced this solution with enthusiasm due to the significance of the subject, the specific friction point it addresses, and the substantial revenue loss associated with counterfeits. Authentique also helps brands reduce fraudulent returns.”

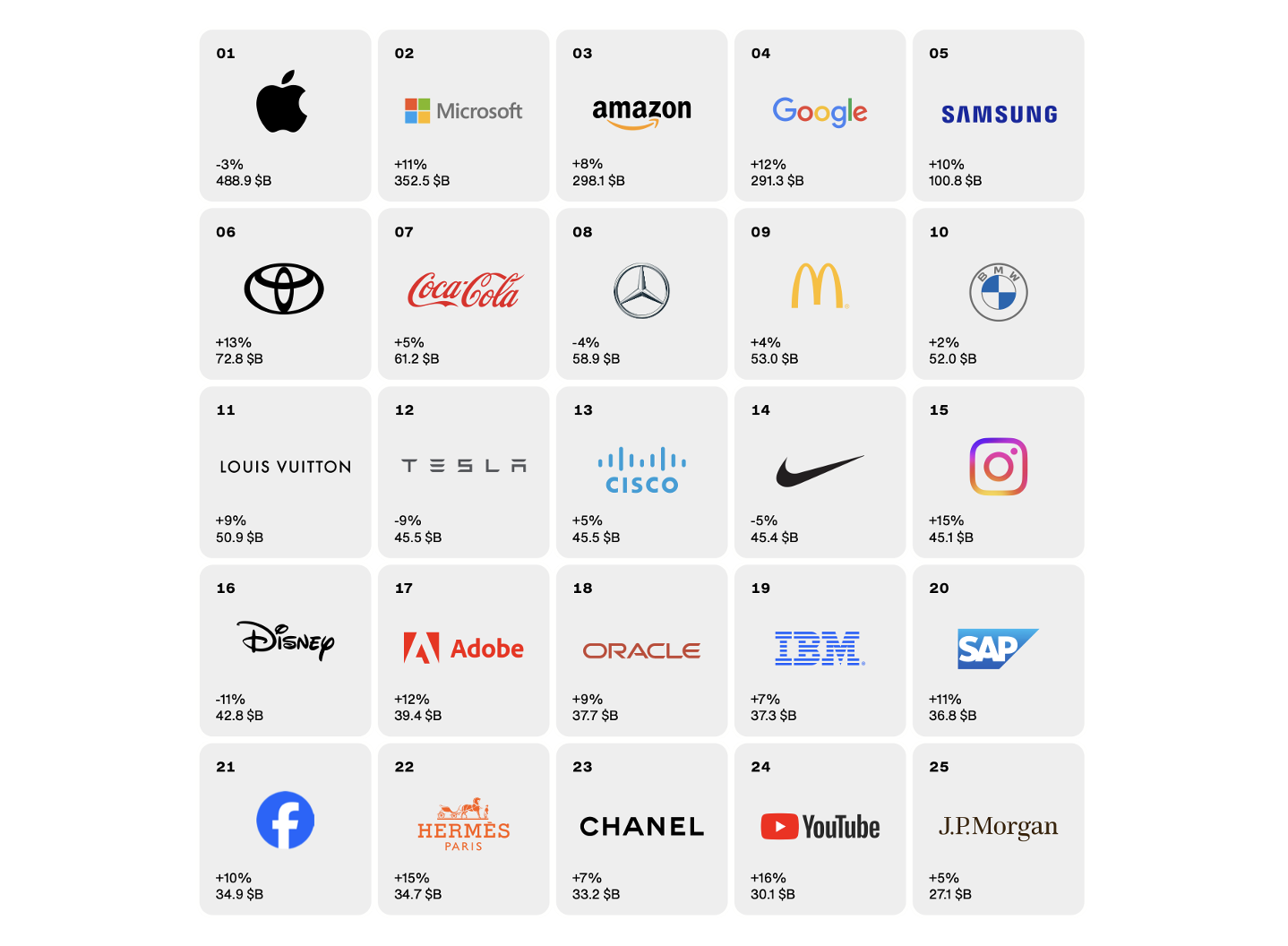

Interbrand released a report of its own this week, its 2024 Best Global Brands ranking, which saw Louis Vuitton, Nike, Hermès, and Chanel land in the top 25. Meanwhile, Hermès, Prada, and Sephora were name-checked as among the “fastest risers.”

Some of the most interesting information from the report comes by way of the consultancy’s comments on brand loyalty – or the lack thereof: “Across all markets, choices are increasing exponentially. Even if customers know, trust, or even love a brand, exploring new options has never been cheaper and quicker. This creates an erosion of loyalty and increases the need for all brands to continuously address rapidly shifting needs and expectations.”

This mirrors (to some extent) what the FT’s Brooke Masters wrote not too long ago, stating that big-name brands, “rather than being immune” to the whims of consumers in times of economic hardship, “are squarely in the line of fire as shoppers start to cut back.” While Masters was largely referring to mass-market products like Coke/Pepsi or consumers’ preferred cleaning product brands when she said that “emotional ties to specific products started fraying in the pandemic, when persistent shortages of basic items … forced many consumers to reach beyond their preferred selections,” luxury brands are likely not immune.

(Again, cue the rising popularity of dupes, which suggests that consumers are driven, at least in part, by the product and not the brand, itself; hence buying an unbranded pair of leggings that looks like Lululemon’s popular Align pants or even buying a pair that looks to replicate the design but comes with another company’s name on them.)

> Brands & ESG: Interbrand also posed thoughts on the role of branding and ESG, saying, “As we face existential crises such as climate change, resource depletion and global conflict, brand leaders are at an inflection point; do they want to be seen as part of the problem, or part of the solution? At a time of distrust towards institutions, government and even NGOs, societal leadership is now seen as a core function of business.”

> A note on the legal front: “When a business competes on product, price or proximity, advantages are increasingly temporary,” per Interbrand. As such, “the brand becomes the only truly ownable point of difference – the one asset that cannot be legally replicated. As such, it’s the source of choice, revenue and margin. Its performance can and should be enhanced and optimized – but one should never save on the car’s maintenance purely to buy more fuel.”