Once shorthand for timelessness and quality, the term “investment” piece has taken on a far more literal meaning in the personal luxury goods market. Increasingly, and particularly in connection with certain handbag models, it is being used to describe consumer goods that are not merely expected to endure from a style perspective, but to appreciate financially. In this context, the term is being used to describe accessories that are part of a class of investment assets, or in other words, handbags that are purchased for the purpose of earning returns when they are later resold.

This evolution reflects a broader financialization of luxury, in which products are discussed in the language of returns, premiums, and portfolio diversification. It is a narrative fueled by resale platforms, auction houses, market reports, and social media content that collectively promote the idea that certain bags, most notably Hermès’ Birkin and Kelly models, can rival traditional investment vehicles.

But while that proposition has proven powerful from a marketing standpoint, it is far more fragile from a market and legal perspective.

The Potential Paradox at Play

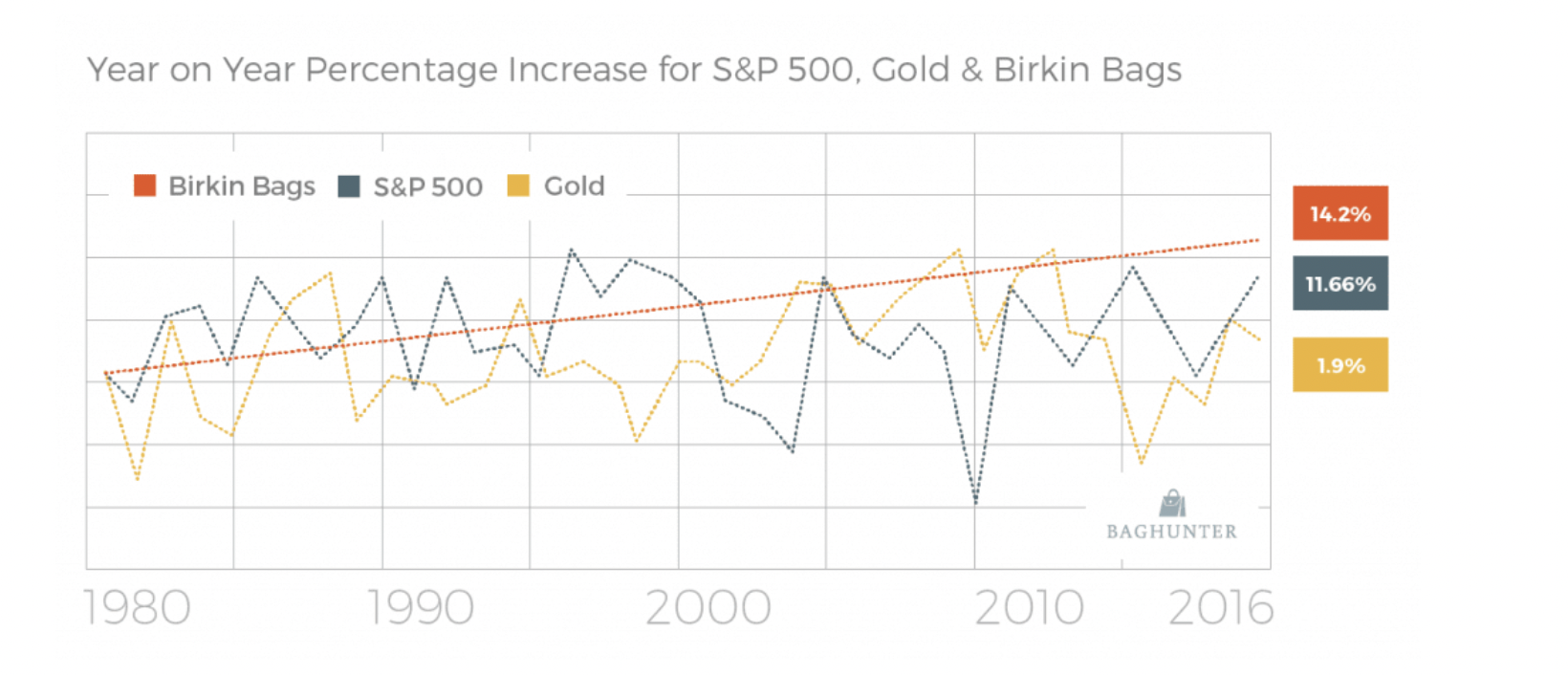

The notion that handbags can serve as outperforming assets entered the mainstream in 2016, when luxury resale platform Baghunter released a report comparing the performance of Birkin bags from 1980 through 2015 with that of the S&P 500 and gold. Baghunter concluded that Birkin values rose steadily, at an average annual rate of 14.2 percent, while stocks and commodities experienced volatility.

In other words, Birkins, which retail for upwards of $10,000 (subject to additional hoops/spending), do not have bad years, making them “the safest and least volatile investment market of the three,” per Baghunter.

Two years later, Jefferies analysts reinforced that narrative by pointing to the strength of the secondary market for top-tier Hermès bags, citing the resale of a Himalaya Birkin purchased in 2010 for €29,600 and sold in 2016 for €157,500, a gain of more than 400 percent, outpacing Euronext Paris-listed Hermès shares over the same period.

Auction houses soon followed. Christie’s launched online-only handbag auctions in 2012 and by 2017 had established a dedicated Handbags & Accessories department that quickly became one of its fastest-growing luxury categories. In the process, the infrastructure necessary to treat handbags as tradeable assets – price benchmarking, authentication services, and increasingly global resale platforms – has been steadily put in place.

What has been far less stable, however, is the pricing itself. Recent market data suggests that resale values, particularly at the very top of the handbag market, have already undergone a meaningful repricing. According to Bernstein Research’s Secondhand Pricing Tracker, which monitors average auction resale premiums for Hermès Birkin and Kelly bags relative to their original retail prices, the market has retreated sharply from its pandemic-era highs.

At its peak in 2022, the average resale premium stood at approximately 2.2 times retail, meaning that a Birkin originally purchased for $10,000 could fetch roughly $22,000 at auction. By November 2025, that premium had fallen to about 1.4 times retail, translating into resale prices closer to $14,000 for the same bag.

The Bernstein Birkin and Kelly Price Tracker, developed by luxury analyst Luca Solca, functions as an index measuring the ratio of auction prices to retail pricing, offering a standardized benchmark for top-tier secondary market performance. The index shows that even in the most insulated segment of the resale market, premiums are not immune to volatility.

At the individual model level, the correction is even more pronounced. The Birkin Togo 30, for instance – which carried an average resale premium of 1.9 in 2018 and 1.7 in 2022 – was reselling at roughly 1.0 times retail by late 2025, per Bernstein, effectively eliminating any resale premium altogether.

Solca says that decline is the result of a broader “sobering up from the post-Covid euphoria,” driven by inflationary pressures, slower employment growth among aspirational consumers, and increased supply as more owners move to liquidate pandemic-era purchases. In other words, the very market that was once cited as evidence of handbags’ investment-grade stability is now behaving much more like a cyclical consumer category and responding to the same macroeconomic pressures affecting markets more broadly.

Different Market Mechanics

Even when resale premiums are positive, equating handbags with financial instruments fails to account for the fundamentally different market mechanics at play. The most obvious distinction lies in liquidity. Public equities trade in markets with enormous daily volumes, enabling near-instant entry and exit. By contrast, the global population of Birkin bags has been estimated at roughly one million, with only a fraction circulating on resale platforms or at auction in any given year.

As Sapna Maheshwari previously wrote for BuzzFeed News, stock prices reflect continuous price discovery across large and active markets. If shares in Apple are trading at $100, that price is generally accessible to buyers and sellers, alike. No such pricing certainty exists for rare handbags, where values vary widely depending on size, leather, hardware, color, provenance, and condition, and where sellers may wait months to complete a transaction.

Moreover, reported “returns” rarely reflect net outcomes. Platform commissions, authentication fees, shipping, insurance, storage, and opportunity cost all materially affect realized resale profits. These frictions, which are far more pronounced than in regulated financial securities markets, further chip away at the narrative that handbags consistently function as reliable stores of value.

There is also the problem of selection bias. Headlines overwhelmingly focus on iconic Hermès models and exceptional auction results, rather than on the broader universe of luxury handbags, many of which depreciate significantly once fashion cycles, wear, and shifting consumer tastes are taken into account.

Resale pricing for Hermès bags is heavily dependent on the brand’s tightly controlled retail distribution and chronic undersupply. Scarcity, however, cuts both ways. While it can sustain premiums during periods of strong demand, it also renders the market vulnerable to shifts in consumer sentiment. That vulnerability is compounded by expanding resale infrastructure and rising secondary-market supply. As resale platforms professionalize authentication and logistics, and as more consumers view resale as a liquidity option rather than a last resort, supply pressures can increase rapidly.

At the same time, the continued proliferation of high-quality counterfeits introduces additional risk and uncertainty into pricing dynamics.

Brand risk is not unique to luxury goods; publicly traded companies are also exposed to shifts in consumer demand. But the critical difference lies in market mechanics. Investors can typically exit equity positions quickly and at transparent prices. Owners of high-end handbags, by contrast, face thin markets, limited pricing visibility, and transaction delays, precisely the opposite of what investment theory would prescribe for a low-risk asset.

None of this has slowed the overall growth of the resale sector. Bloomberg has reported that amid broader market volatility, luxury goods, particularly handbags, continue to attract interest as alternative stores of value. Knight Frank’s Wealth Report has likewise identified handbags as an expanding segment within the broader collectibles market.

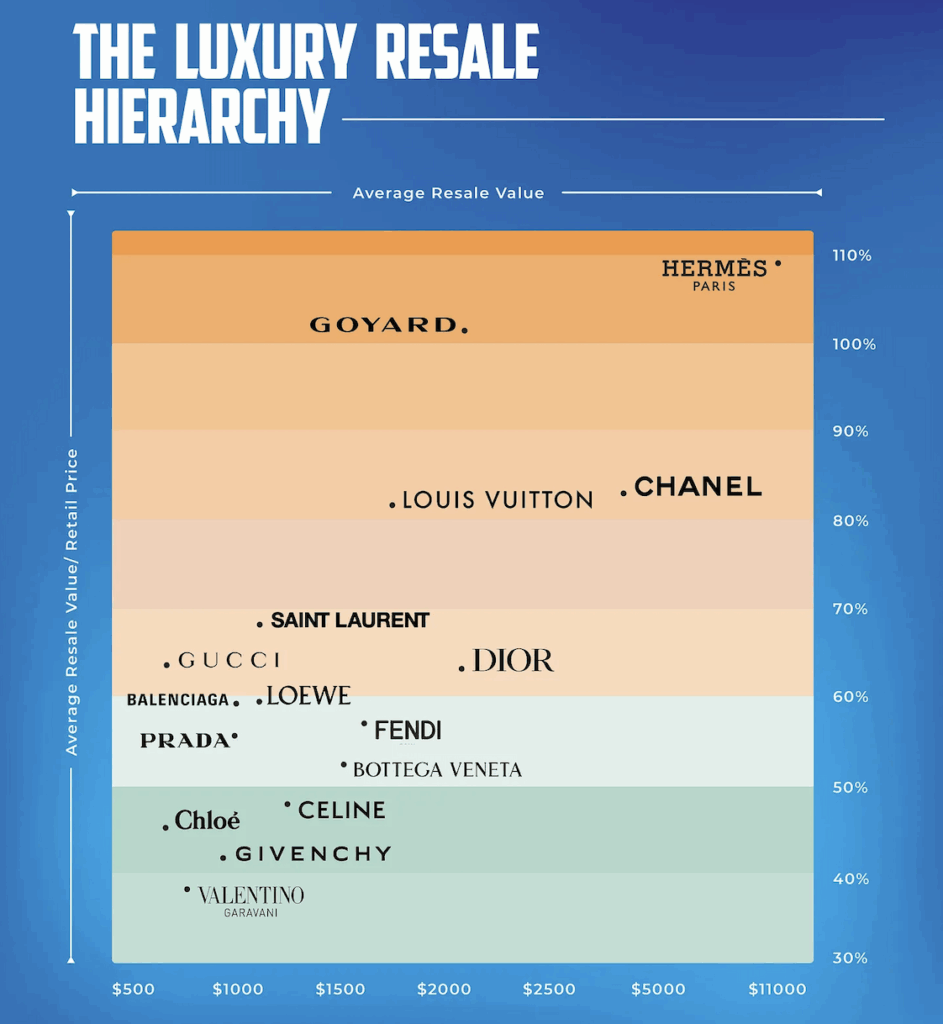

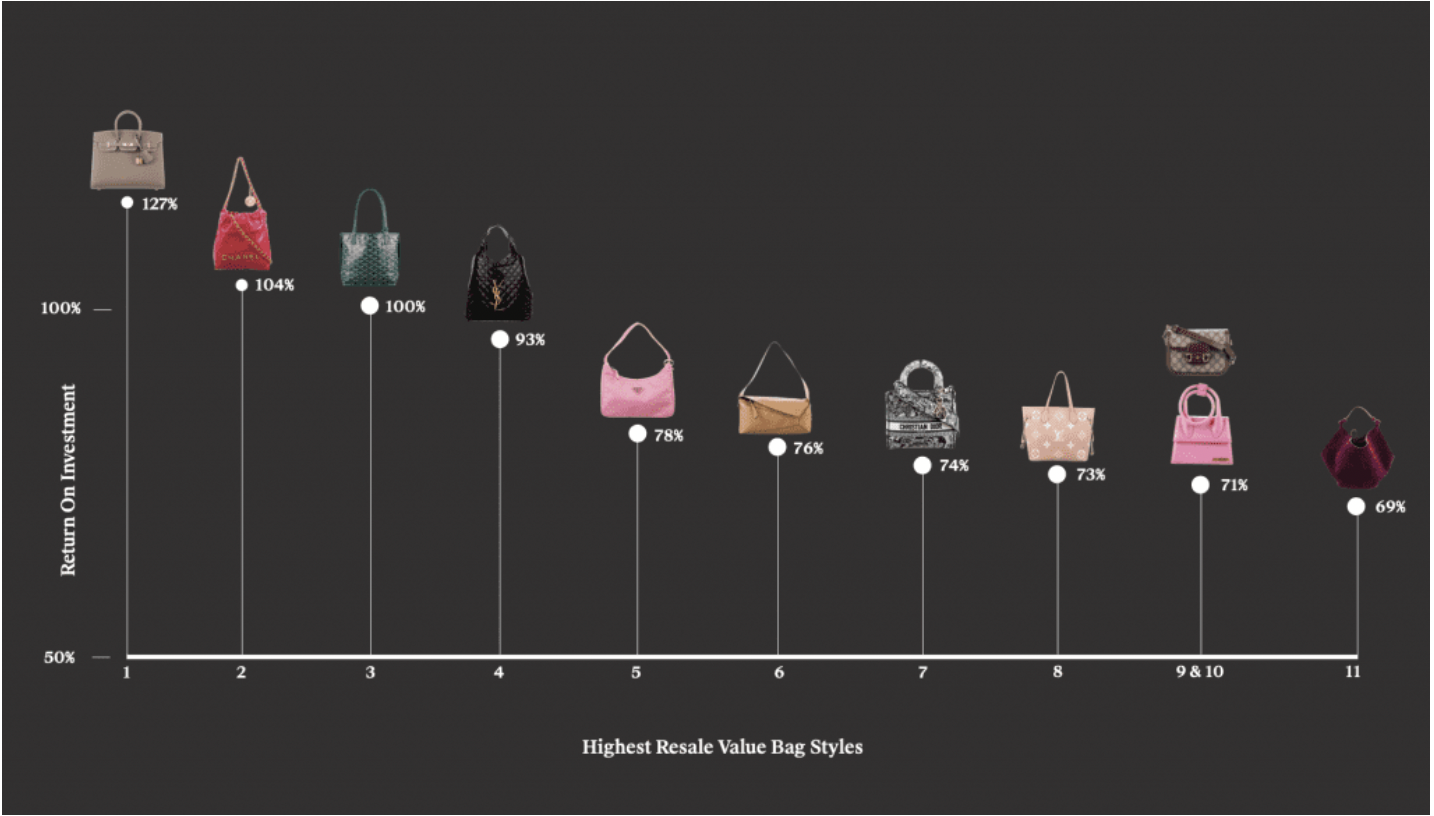

Resale platforms, for their part, continue to highlight strong value retention across multiple brands, with Hermès bags routinely nabbing the title of the top-performing brand by resale value. In its 2023 annual report, for example, The RealReal lists Birkin bags as having the overall highest resale value (see above), whereas its 2025 report reveals that Kelly bags sold on its site “currently fetch an average of 50% above MSRP when sold secondhand.”

Still, even these platforms’ own data reflects stabilization rather than acceleration, suggesting that the exceptional appreciation rates of the early pandemic period are unlikely to represent a permanent baseline for the category.

The “Investment Bag” Narrative

The persistence of the “investment bag” narrative is not difficult to explain. For brands, resale validation supports continued price escalation by reassuring consumers that purchases are at least partially recoverable. For resale platforms, the framing attracts sellers, inventory, and transaction volume. And for consumers, it offers psychological justification for escalating luxury prices.

At the same time, resale transparency reinforces brand consolidation. As Solca previously noted, “The emergence of the second-hand market further reinforces category consolidation and mega-brand concentration, as it provides instantaneous and transparent evidence of which brands hold value and which don’t, [which] is bound to push middle-class consumers to converge even more to ‘surefire’ brands.”

In that sense, resale markets do not merely reflect brand hierarchy; they help to cement it.

What remains unresolved is the regulatory and consumer protection gap that accompanies luxury’s financial turn. Unlike regulated investment products, handbags promoted, directly or indirectly, as stores of value are not subject to standardized disclosures, performance reporting requirements, or risk warnings. Yet, the marketing rhetoric surrounding them increasingly mirrors financial language.

As luxury continues to blur the line between consumption and speculation, the tension between fashion’s emotional appeal and its emerging asset logic is likely to sharpen. And while handbags may continue to hold – and in some cases regain – resale value, the market now offers clear evidence that even its most iconic products are not insulated from economic cycles, shifting demand, or market saturation.

Updated

This article was initially published on Oct. 18, 2023 and has been updated to reflect data from Bernstein’s Hermès price tracker.

Share