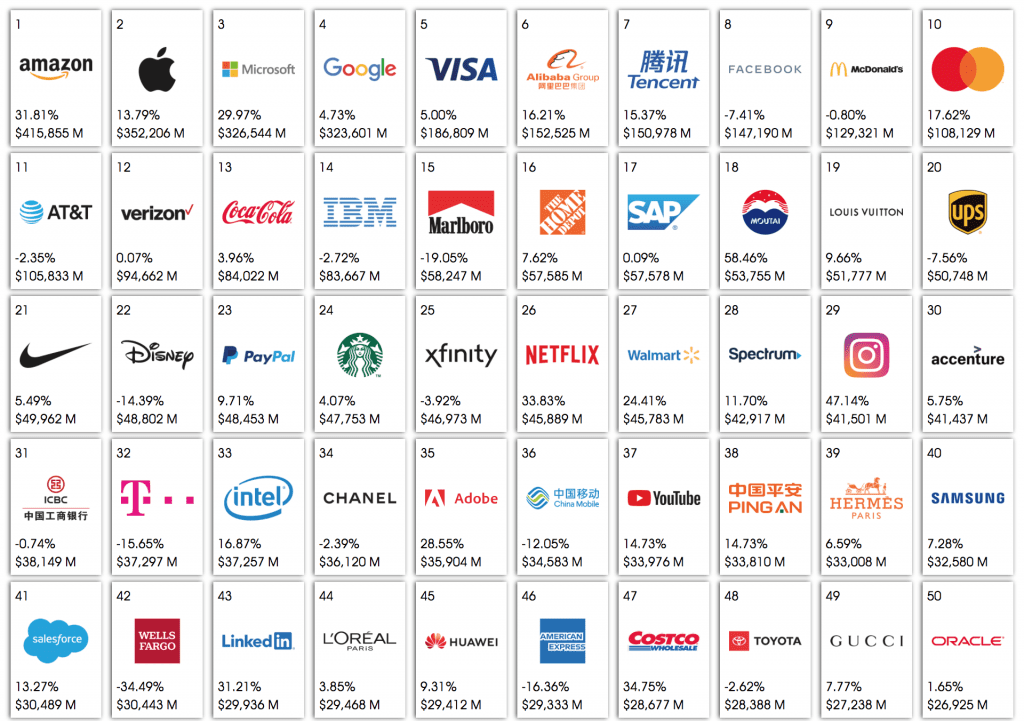

“Strong brands provide stock market resilience during periods of volatility, providing a reliable, positive return on the money invested to build valuable brands,” WPP and Kantar assert in their 2020 BrandZ™ Top 100 Most Valuable Global Brands ranking. The recently-released report – which looks across more than two dozen market categories to rank the most valuable brands, putting Amazon, Apple, Microsoft, Google, and Visa in the top 5 spots – found that the world’s most valuable brands have recorded a steady increase in value of 6 percent (compared with a 7 percent increase a year ago), and reached nearly $5 trillion in total value, despite the economic toll of the COVID-19 pandemic.

Looking specifically to luxury brands’ valuations, which are calculated by pairing the brands’ financials with consumer viewpoints by way of research that covers over 3.7 million consumer interviews and more than 165,000 different brands in over 50 markets (to determine brand equity), the names topping the 2020 luxury-specific list did not change much compared to last year’s list. Louis Vuitton, Chanel, Hermès, and Gucci again took the top four spots for luxury brands, and the number 19, 34, 39, and 49, spots, respectively, on the Top 100 list regardless of sector.

They are followed by Rolex, Cartier, Dior, Yves Saint Laurent, Burberry and Prada, respectively rounding out the rest of the top 10 of the luxury list – but did not make it onto the full 100 list. Taken together, these ten brands have a combined value of $177 billion, according to WPP and Kantar’s metrics, and were one of the six categories (of a total of 14 categories) that increased in value.

The report attributes the rise in value to the fact that “luxury brands, compared to brands in other categories, tend to enjoy strong brand equity, with strong brand equity adding resilience.” Additionally, enduring consumption by “Chinese shoppers, which account for an estimated one-third of luxury purchases worldwide,” helped luxury brands to continue to grow despite challenging market conditions.

As for the role of luxury brands in the market, more generally, WPP and Kantar found that “the influence of young consumers continues to shape the luxury category, even the very definition of luxury,” and that just with the other categories of brands, the ability of a brand “to be creative and innovative,” (i.e., to “stand out and set trends”) was “the most determinative factor in whether brands increased or decreased in value year-on-year.”

“Louis Vuitton’s partnership with the streetwear brand Supreme, and the creation of the Fenty brand by LVMH and the singer Rihanna” are examples of how “luxury integrated deeper into society” and the interest of younger consumers, particularly Chinese shoppers, who drive a substantial portion of luxury sales worldwide, according to the report, while “the expansion of athleisure as affordable luxury also demonstrated this phenomenon.”

Moreover, WPP and Kantar assert that “sustainability has become a creative territory, as “luxury brands have discovered that designing, crafting, and packaging products using sustainable materials can enhance desirability and exclusivity.” Beyond that, “some customers have become less comfortable with products made with exotic leathers or furs,” and/or with brands whose values do not align with their own. It is in this vein that a trend is emerging, one that sees at least some consumers “using logos not to aunt wealth – i.e., ‘this is what I can afford’ – but rather to express individuality – i.e., ‘this is who I am.’”

With this in mind, “The desire for products crafted with sustainable materials and presented with minimal packaging makes sustainability the new luxury,”which is a large part of why brands like Loewe are rolling out sustainability-centric collections, and “32 fashion and luxury brands,” such as Burberry, Chanel, the Prada Group, and the Gucci and Bottega Veneta’s parent company Kering Group, “signing a commitment to reduce their environmental footprint.”

Another key point of reference in terms of luxury in this year’s report: a focus on the necessary evolution of brands’ heritage storytelling. “Within the luxury category, many brands have rich heritages that have underpinned and helped to instill the quality credentials that help build a premium offering.” In other words, storied histories of limited quantities, the highest quality materials, and a small manufacturing networks that consist exclusively of brand-owned and operated factories help brands to elicit (and sell) the aura of luxury even as such practices have – in many cases – been phased out in favor of less expensive materials (i.e., coated canvas) and cost-efficient, outsourced manufacturing, and an emphasis on higher-volumes of sales.

With the importance of such heritage and the marketing of it in mind, the report asserts that it is “no longer enough to sustain their offering moving forward, and repetition of the brand legacy by itself is not going to entice the modern consumer.” As such, “Brands must go beyond this approach and keep their heritage relevant by finding ways to make yesterday’s stories connect with tomorrow’s customers.”

Finally, in light of the enduring COVID-19 pandemic and the various phases of reopening that are happening across the globe, the report states that two already-existing luxury category trends may accelerate: consolidation and e-commerce, as high-fashion and luxury brands continue to be brought under the umbrellas of conglomerates (the recent LVMH acquisition of Tiffany & Co. is one example), and entities within this sphere move to place greater reliance on online shopping after years of attempting to avoid it in order to adhere to a more traditional understanding of what luxury looks/acts like.

As for the Top 100 brands, as a whole, BrandZ chairman David Roth says that “the continued growth in value of [these brands] shows that strong brands are in a much better place than they were in the global economic crisis of 2008-2009.” This is the result of “a significant improvement in brand equity now compared to 10 years ago,” per Roth, “because businesses understand the importance of investing in brand-building and are stronger and more resilient as a result.”

Share