Financial markets have been in flux in recent years, but the value of the world’s strongest brands, including some of the biggest luxury players, has “steadily increased, driving customer choice, loyalty, and margins,” Interbrand states in connection with its 2022 Best Global Brands report. Reflecting on its annual brand valuation exercise, the management consulting company asserts that the average brand value of the top 100 brands – namely, the biggest global brands that publicly report their performance and that generate at least 30 percent of revenue from outside of their home region – rose by 16 percent to more than $3 trillion, which “demonstrates the growing contribution a company’s brand has in driving its economic success.”

Based on its evaluation of global technology, consumer-goods, automotive and financial brands, New York-headquartered Interbrand calculates a “brand value” for each one by considering the company’s financial forecast, “role of brand” (i.e., “the portion of the purchase decision attributable to the brand, itself, as opposed to other factors, such as purchase drivers such as price, convenience, or product features”), and brand loyalty elements. Against this background, tech brands dominate the top spots, with Apple landing in the number 1 position with a brand value of $482.2 billion, followed by Microsoft ($278.3B), Amazon ($274.8B), and Google ($251.8B), and Samsung ($87.7B) in the top five.

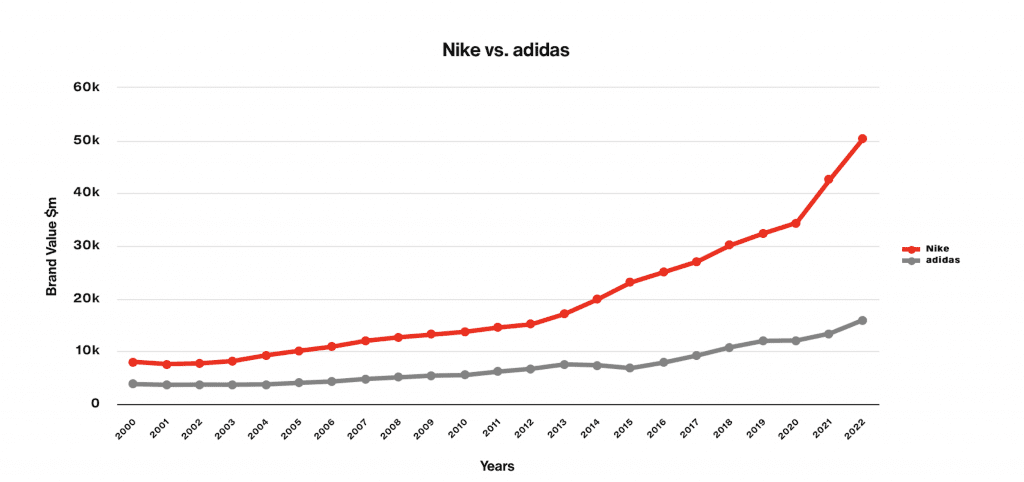

Rounding out the top 10 are Toyota in the number 6 spot ($59.8B), Coca-Cola ($57.5B), Mercedes-Benz (56.1), Disney ($50.3B) and Nike with the Swoosh landing in the top 10 first the first time in 2022. Nike’s $50.3 billion brand value is up 18 percent from Interbrand’s 2021 ranking and up from a brand value of $32.3 billion back in 2019.

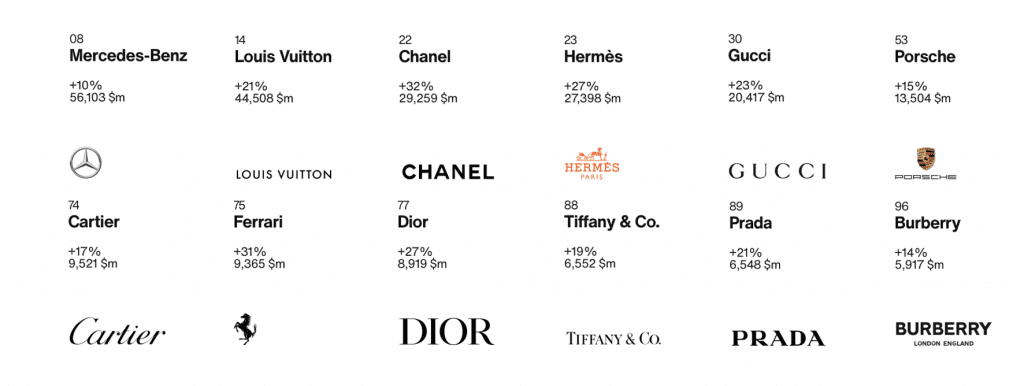

LUXURY: In terms of luxury brands, in particular, Louis Vuitton landed in the number 14 spot, the highest-ranking luxury brand behind Mercedes, with a brand value of $44.5 billion (up 21 percent – but down one position – from Interbrand’s 2021 ranking). Broadly speaking, Louis Vuitton’s value has been on the rise since Interbrand began tracking it in 2000. On the one hand, it saw a significant spike in brand value between 2004 and 2005, which corresponded with it celebrating its 150th anniversary. On the other, it has seen minor dips over the years, including from 2008 to 2009 (likely the result of the recession) and 2019 to 2020, likely prompted by the pandemic.

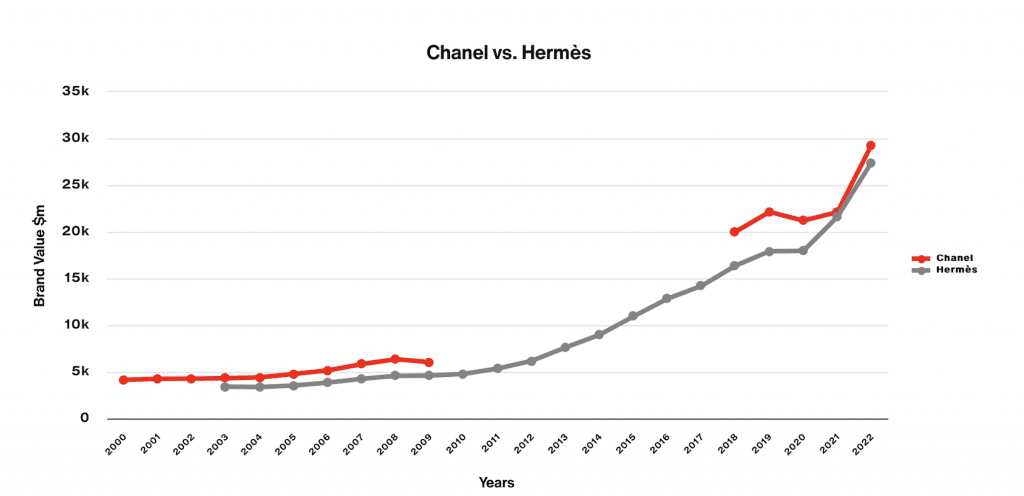

Chanel and Hermès were ranked similarly in the 22 and 23 positions, respectively – the same as last year. Chanel’s brand value rose 32 percent year-over-year to $29.3 billion, and Hermès’s value rose by 27 percent to $27.4 billion. (The Birkin bag maker has seen steady growth over the past two decades in terms of Interbrand’s values, steadying for a year between 2019 and 2020, but has since bounced back from the pandemic with robust growth in brand value.)

Not too far behind, Gucci landed in the number 30 spot, up 3 places from last year, with a $20.4 billion brand valuation, up 23 percent. The boosts for Kering-owned Gucci are interesting in light of still-slowing growth for Gucci, and corresponding worries among analysts. Bernstein analyst Luca Solca pointed to “brand fatigue” in China and a need for new creative energy in a note last month, while Jefferies’ Flavio Cereda and Kathryn Parker said that Gucci is “an odd limbo” complete with “obvious shortcomings.”

In other interesting rankings, LVMH-owned luxury brand Dior remained in the same spot – 77 – for 2022, with a brand value that rose by 27 percent to $8.9 billion. The nearly 30 percent rise is noteworthy, and chances are, LVMH’s second-largest brand – which Interbrand began tracking in 2017 when the brand was fully brought under the conglomerate’s umbrella – will continue to trend higher in light of enduring progress from a positioning and revenue perspective; Dior boasted slightly higher growth in Q3 than Louis Vuitton, for instance. (From a positioning POV, Solca stated last year that “the ‘new’ Dior – complete with its ‘pioneering’ position when it comes to collaborations, market share gain in the skincare segment, successful adoption of local brand ambassadors, including in China, and high visibility across social media channels – has ‘resonated with consumers and has been in recent years the hottest brand in the high-end.’” This has also come “hand in hand with continuing increases in pricing to further establish the brand’s high-end credentials” alongside the likes of Chanel and co.)

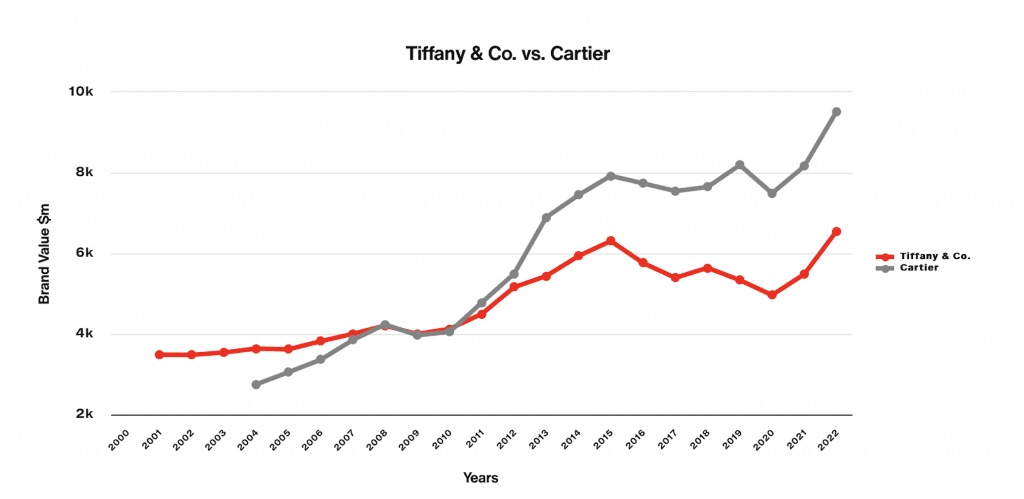

As for an LVMH-owned brand whose position is also likely to move upwards even further in the near- and medium-term, that is Tiffany & Co., which jumped 4 places from 2021 and rose in value by 19 percent to $6.6 billion. (As of the 2022 ranking, Tiffany & Co. surpassed its previous high of $6.3 billion in 2015, and overcome a low of $4.9 billion in 2020.) The famed jewelry brand is undergoing a significant revamp – complete with the newly-released Lock collection, which appears to be Tiffany’s attempt to compete with Cartier’s Love bracelet – since it merged with LVMH in January 2021 by way of a $15.8 billion deal.

Burberry’s ability to maintain a spot within the top 100 is also worthy of attention. The brand took the number 96 position (up one place from 2021) with a brand value of $5.9 billion – an increase of 14 percent YoY. While Burberry is hardly at its peak in terms of consumer demand and/or market share, and it is certainly lagging in terms of coveted leather goods (especially compared to its peers), this is expected to change once former Bottega Veneta creative director, who was appointed to the Burberry helm in September, begins delivering his designs.

In the meantime, what appears to be driving Burberry’s strength from a brand valuation perspective is its ventures in the virtual world, including a successful non-fungible token project. Interbrand specifically highlights the brand’s VP of Channel Innovation Rachel Waller, who pointed to Burberry’s experimentation in terms of “the idea of seamlessly connecting our customers’ digital and physical worlds,” as well as its effort to “redesign the online experience to enhance the customer journey by replicating behaviors seen in store and increasing personalization.”

Finally, Prada – which began “renovating its retail network, investing more in e-commerce and digital marketing and refreshing its product range [in 2014], after losing ground to both new and old competition” – is also worth mentioning, as the Italian luxury brand, which rose 5 places to no. 89 and 21 percent to a brand value of $6.6 billion, putting it above its previous high of $6.2 billion in 2015.

MASS-MARKET: Luxury entities were not the only ones that climbed in terms of brand value between the 2021 and 2022 rankings, as mass-market entities like Nike continued to rise in value. (Nike’s brand value has been rising steady – and without interruption – since Interbrand began tracking it in 2000.) At the same time, Nike’s closest rival adidas took the number 42 spot, with its $15.9 billion brand value, which rose 19 percent from 2021; that valuation was presumably calculated before the fall-out with Kanye West.

The two fast fashion brands on Interbrand’s top 100 delivered mixed results. Zara fell two places from last year to the number 47 spot, but its brand value still rose to almost $15 billion. Its value is up by 11 percent from last year’s $13.5 million but down significantly from a high of $18.6 billion in 2017. The Spanish titan is not suffering nearly as much as H&M, whose brand value has been falling consistently since it reached $22.7 billion in 2016. Th Swedish company nabbed the number 56 spot for 22, down 13 places and down 8 percent in brand value to $12.9 billion.

H&M’s stellar fall – which comes as Interbrand says that it incorporated “quantitative” Environmental, Societal and Governance (“ESG”) data incorporated into the Best Global Brands methodology for the first time this year – appears to fall in line with the enduring narrative that consumers, particularly millennials and Gen-Z, are increasingly cognizant about how companies’ approaches to ESG and shifting their consumption patterns accordingly. However, Zara’s rebound in brand value seems to represent the reality of the situation, namely, that consumers’ reported penchant for sustainably-made products does not always – or often – translate to sales or lack thereof.

As for the ranking as a whole, Interbrand’s global CEO Gonzalo Brujó said that amid the current “period of economic uncertainty, the most successful brands will continue to make ever stronger connections with consumers,” arguing that “t is no longer enough to have a static business and brand offering. Successful brands know how to harness new technology to create improved experiences for consumers and become a truly integrated part of their lives.”

Share