When Aston Martin Lagonda went public on the London Stock Exchange in October 2018, it was supposed to signal a new chapter – one where the brand would join the rarefied ranks of public luxury icons. The British automaker’s pitch was clear: emulate Ferrari’s high-margin luxury business model. Like the Italian sports car icon, Aston Martin – synonymous with British elegance and James Bond appeal – aimed to leverage its brand cachet to expand into apparel, real estate, and a planned line of SUVs.

Executives pitched the move as a long-term growth story, underpinned by product diversification, luxury brand expansion, and disciplined volume targets. The immediate result? With shares priced at £19 each, the listing valued the company at approximately £4.3 billion. But once the dust settled, what followed was one of the most precipitous post-IPO declines in recent UK corporate history.

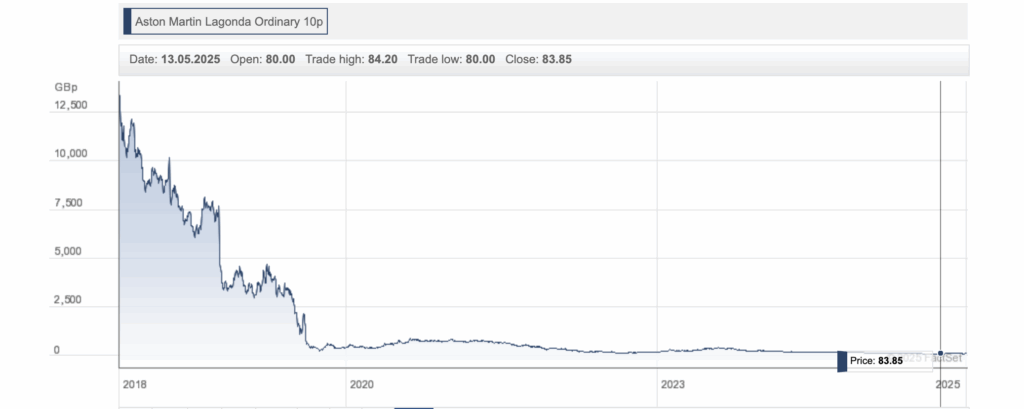

A Stunning Post-IPO Decline

Within a year, Aston Martin’s share price had fallen more than 70 percent, eventually sinking below £5 per share. Investors grew skeptical of the company’s volume projections, which appeared overly ambitious relative to its manufacturing capacity and dealer network strength. Despite earlier hopes, new models like the refreshed Vantage and continued sales of the DB11 – introduced pre-IPO in 2016 – did not generate the margin-rich performance Aston Martin had forecast. Persistent losses, mounting debt, and underwhelming sales figures further undermined its promise of Ferrari-style profitability.

Despite its positioning as a luxury entity, the market viewed Aston Martin’s strategy as aspirational and structurally flawed. Widely described in the press as a “colossal failure,” the 2018 IPO came to symbolize investor frustration with the company’s post-listing performance.

Adding to market unease was the DBX, Aston Martin’s first foray into the SUV segment. While the DBX would later prove commercially important, its development was capital-intensive and came at a time when the company’s liquidity was under pressure. Rather than signaling an expansionary win, the DBX’s launch highlighted the fragility of Aston Martin’s balance sheet.

Operational missteps and supply chain inefficiencies also weighed on investor sentiment. The company struggled with inventory buildup and slow dealer sell-through rates, particularly in China and the U.S. – two markets key to its luxury positioning. Moreover, questions about governance emerged early on, with critics pointing to the board’s limited public-market experience and concerns around executive compensation despite widening losses.

By early 2020 – just 15 months after the IPO – Aston Martin’s market capitalization had dropped by more than 75 percent, prompting the company to seek potential investors. According to reports, Aston Martin approached several parties in late 2019, including Chinese auto giant Geely and Canadian billionaire Lawrence Stroll, who had an existing interest in the auto sector through his ownership of the Racing Point Formula 1 team, acquired earlier that same year. Preliminary discussions with private equity firms reportedly yielded limited interest, as there was little appetite for a pure financial buy-in without governance control or operational levers.

Geely explored a deal that would have seen it take a significant equity stake – mirroring its previous rescue of Lotus – but negotiations faltered due to disagreements over valuation and strategic influence. Meanwhile, Stroll, with exposure to the luxury performance market through past investments in brands like Michael Kors, moved quickly and aggressively. His interest was strategic: he saw Aston Martin not just as a car company but as a brand with underleveraged luxury equity.

Aston Martin’s urgent need for liquidity gave Stroll leverage. The company had over £800 million in net debt, and liquidity was drying up ahead of the DBX launch – an SUV it needed to succeed both commercially and reputationally. Without new capital, Aston Martin risked a credit downgrade and possibly even a covenant breach.

A New Start Under Stroll

By early January 2020, Aston Martin warned that its profit for 2019 would amount to just half of what it generated in the same period a year earlier. After weeks of negotiation, Aston Martin and Stroll’s Yew Tree Consortium announced a rescue package: an initial £182 million equity investment, followed by a broader £500 million capital restructuring.

The deal, formally announced on January 31, gave Stroll and his investors a 16.7 percent stake (later expanded), two board seats, and a roadmap for greater strategic control. Crucially, the deal also included a recommitment to the company’s F1 ambitions, rebranding Stroll’s Racing Point team as the Aston Martin F1 Team for the 2021 season. Aston Martin revealed it would raise an additional £318 million through the issue of new shares, some of which would be purchased by Stroll’s consortium.

The transaction provided Aston Martin with breathing room and placed a well-connected operator at the helm of its restructuring. The capital raise involved both equity and debt components, reflecting the scale of the company’s liquidity needs at the time. Stroll became Executive Chairman and quickly initiated an aggressive turnaround strategy: slashing production targets, streamlining product lines, and leveraging his Formula 1 connections to relaunch Aston Martin’s motorsports brand visibility. However, with Stroll came a new governance dynamic that drew criticism from investors and analysts alike. As his influence grew, so did concerns about the consolidation of power and lack of independent oversight at the board level.

As of May 2025, the Yew Tree Consortium holds approximately 33.13 percent of Aston Martin Lagonda’s issued share capital, following a £52.5 million investment through which the group acquired 75 million new ordinary shares at 70 pence per share. To facilitate this increase without triggering a mandatory takeover offer – typically required under UK law when a shareholder exceeds 30 percent ownership – the consortium secured a waiver approved by independent shareholders.

Mercedes-Benz & More Complications

Mercedes-Benz entered the picture in December 2013, gradually acquiring a 5 percent equity stake and a non-voting seat on the board, alongside a technical partnership through which Mercedes-AMG would supply engines and electrical systems for the next generation of Aston Martin models.

In October 2020, Aston Martin revealed that Mercedes was looking to expand its existing partnership and increase its equity stake to up to 20 percent by 2023. The increase would occur in several stages as part of a wider issue of 250 million Aston Martin shares at 50 pence each. In addition to an injection of funds, Mercedes would supply powertrains and advanced electric vehicle technologies, and in exchange, the German firm would gain the right to nominate one non-executive director to Aston Martin’s board.

While the Mercedes deal provided Aston Martin with much-needed technical infrastructure and more cash, it complicated shareholder dynamics further. With Stroll’s group, Mercedes, and a revolving group of institutional investors all holding sizable stakes, governance became a delicate balancing act. Each entity came with its own vision for the brand – some emphasizing luxury positioning, others prioritizing electrification and volume.

And in May 2023, Chinese automotive group Geely increased its stake in Aston Martin to approximately 17 percent, becoming the third-largest shareholder behind the Yew Tree Consortium and Saudi Arabia’s Public Investment Fund. Geely’s presence introduced yet another strategic voice with clear global expansion ambitions and strong infrastructure in emerging markets. While no overt conflicts have surfaced among major shareholders, the multiplicity of strategic stakeholders leaves room for tension and requires coordinated alignment across board-level decisions, product planning, and long-term capital deployment.

Governance Questions & the Aston Martin Brand

Internally, Aston Martin has faced persistent questions on the issues of governance, leadership stability, and strategic accountability. The company has seen rapid CEO turnover in recent years – Andy Palmer was succeeded by Tobias Moers, a former Mercedes-AMG executive, who was then replaced by ex-Ferrari CEO Amedeo Felisa in 2022. Each transition ushered in a new tone and direction, often leaving investors grappling with inconsistent messaging and an unclear long-term view.

At the heart of these concerns is Aston Martin’s sprawling and often contradictory strategy. The company has sought to scale production, preserve luxury exclusivity, expand into lifestyle verticals, leverage motorsport for brand equity, and position itself for an electrified future – all at once. Analysts at HSBC, Jefferies, and Credit Suisse, and major business publications have flagged recurring doubts about the coherence of this vision, citing conflicting leadership priorities and unresolved tensions between scale and scarcity.

In pursuit of its luxury ambitions, Aston Martin has evolved from a storied British property into a brand with a global lifestyle presence – its name now appears on everything from Formula 1 cars and high-end real estate developments in Miami to Hackett menswear and TAG Heuer watches. While such brand extensions follow a familiar luxury playbook – typically involving royalties, minimum guarantees, and territorial exclusivity – the specific terms of Aston Martin’s licensing agreements are not publicly disclosed. These deals nonetheless demand disciplined internal oversight to ensure alignment with core identity.

Unlike its vertically integrated peers, such as Ferrari, Aston Martin’s licensing model is comparatively decentralized. While it has not yet faced high-profile reputational fallout, the broader risk of overextension looms. As its brand stretches across categories and partners, maintaining the cohesion of its luxury image becomes increasingly difficult.

In short, Aston Martin’s multi-pronged approach – ambitious in scope but uneven in execution – continues to raise fundamental questions about the strength, clarity, and future resilience of its brand governance.

The Road Ahead

Today, Aston Martin is at an inflection point. Electrification looms large, and so does competition – not only from traditional rivals like Ferrari and Porsche but from newer entrants like Rimac and Lotus, who are redefining what luxury and performance mean in the EV era. Meanwhile, the brand must contend with a complex cap table, fragmented leadership history, and a business model that has yet to prove durable in the face of volatility.

In many ways, Aston Martin’s struggle is a familiar one in luxury: balancing legacy with innovation, exclusivity with scale, and vision with shareholder interest. But what sets this story apart is how governance, capital, and brand architecture have collided – at times harmoniously, but more often with friction. For a brand that trades on precision, control, and aspiration, the challenge now is to bring those qualities back into its business, not just its design.

Share