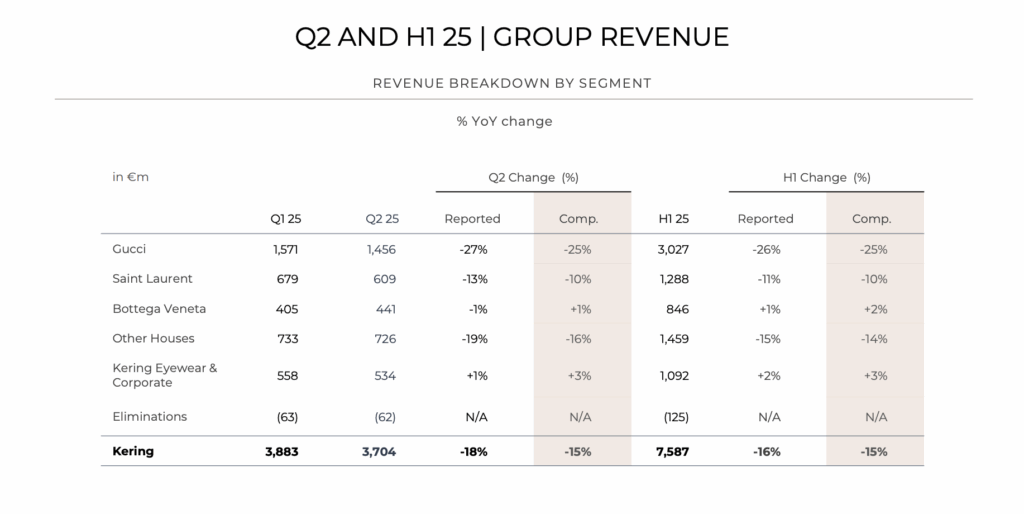

Kering posted a significant slowdown in the first half of 2025, with revenue falling to €7.6 billion ($8.77 billion) – down 16 percent year-over-year – amid what the group describes as a challenging luxury market environment and weak consumer confidence, particularly in Asia. Recurring operating income plunged 39 percent to €969 million, resulting in a slimmer operating margin of 12.8 percent (down from 17.5 percent in H1 2024), while net income attributable to the group fell 46 percent to €474 million.

For its flagship brand Gucci, revenue came in at €3 billion, a 26 percent decline compared to the same period last year, with recurring operating income down by more than half to €486 million (a margin of just 16 percent). Yves Saint Laurent reported €1.3 billion in sales, down 11 percent, while Bottega Veneta emerged as a rare bright spot, delivering a modest 1 percent increase to €846 million. Sales across the “Other Houses” segment – which includes Balenciaga, Alexander McQueen, and the group’s jewelry maisons – dropped 15 percent to €1.5 billion.

Like its peers, Kering saw a broad-based regional slowdown. Asia-Pacific (excluding Japan) plunged 23 percent, reflecting reduced store traffic and tepid demand in China, while Japan posted a 19 percent drop amid a stronger yen and declining tourism. Sales in Western Europe and North America each fell 13 percent, though U.S. performance was buoyed by wealthier domestic customers.

Some of the standout elements for Kering as the first half of the year comes to a close …

> Gucci’s Creative Reset: Gucci’s sharp decline underscores the brand’s transitional moment. Following the departure of creative director Sabato De Sarno in February, Kering announced the appointment of Demna – previously the force behind Balenciaga – as Gucci’s new artistic director, effective July 10, 2025. This move signals a pivot toward a more disruptive, statement-driven aesthetic, but analysts warn that such a reset will take time to resonate with consumers and may not yield immediate sales recovery.

> Strategic and Financial Moves: Despite declining sales, Kering strengthened its financial flexibility. Free cash flow from operations surged 126 percent to €2.4 billion, driven by strategic asset sales, including a €837 million deal with Ardian for prime Paris real estate and the €350 million divestment of The Mall Luxury Outlets to Simon. The group also issued a €750 million bond in May to bolster liquidity and reduce net debt, which fell to €9.5 billion. Beyond financial maneuvers, Kering continued its sustainability push, unveiling its first Water Strategy in April, which targets a “net positive” impact on global water basins by 2050.

> Fashion & Leather Goods Lag: The steep drop in Gucci’s operating margin (from 24.7 to 16 percent) highlights the cost of maintaining brand desirability amid falling traffic and higher operational expenses. Analysts note that Kering’s heavy reliance on Gucci – which accounts for 40 percent of group revenue – leaves it vulnerable to shifts in consumer sentiment. Yves Saint Laurent and Bottega Veneta, while smaller contributors, have been more consistent performers, with Bottega leveraging “quiet luxury” trends and maintaining pricing power.

The Other Houses segment continues to be weighed down by Balenciaga’s wholesale rationalization and Alexander McQueen’s weaker performance, though the group’s jewelry brands, such as Boucheron and Qeelin, remain growth drivers, particularly in the U.S. and Asia.

Is “Big Luxury” Losing Its Shine?

Kering’s H1 2025 results reflect a growing narrative that the post-pandemic luxury boom may be cooling. Like LVMH, which recently reported weaker Fashion & Leather Goods sales for H1, Kering is facing signs of “luxury fatigue.” Consumers – particularly younger affluent buyers – are gravitating toward niche brands and “quiet luxury” aesthetics, favoring craftsmanship and understated design over the logo-heavy products that have dominated the market for years.

In Asia, price hikes and currency pressures have dampened enthusiasm for high-priced handbags and accessories, while aspirational shoppers in the U.S. and Europe are pulling back amid persistent inflation. Analysts have suggested that the broad-based slowdown across major players could mark a structural shift in luxury demand, with ultra-high-end brands like Hermès and jewelry-focused maisons (e.g., Cartier and Van Cleef & Arpels) weathering the storm better than diversified players like Kering.

Kering’s leadership transition is poised to reshape its trajectory. Luca de Meo will step in as Chief Executive Officer on September 15, while François-Henri Pinault remains Chairman. The governance split is intended to sharpen operational focus and support a longer-term strategy aimed at restoring growth across the portfolio. The group’s outlook remains cautious, with management emphasizing the need for “financial discipline,” selective investments, and heightened brand exclusivity in the face of macroeconomic uncertainty.

Analysts see 2025 as a critical inflection point for Kering: whether Demna’s creative overhaul at Gucci and continued expansion of Kering Beauté and Eyewear can offset the luxury market’s slowdown remains to be seen.

Share