Luxury brands may have sidestepped the harshest trade war penalties, but the 15% tariff imposed under the new EU-U.S. deal still poses a significant threat. For industry titans like Chanel, Louis Vuitton, and Dior – who have leaned on steep price increases in recent years to drive profits – the timing couldn’t be worse. Consumer demand is already weakening, especially in the U.S., which has become increasingly important as China’s luxury market continues to sputter.

After a 33% average price hike between 2019 and 2023, many shoppers are showing signs of fatigue. Some are retreating to the resale market; others are questioning whether the quality and creativity justify the soaring price tags. As a result, brands now face a high-stakes balancing act: raise prices modestly to offset tariffs, or risk margin compression and potential damage to their image.

> 15% tariffs on EU exports to the U.S. take effect August 1, affecting everything from fashion and handbags to wine and cosmetics.

> Declining consumer base: Bain & Co. estimates 50 million luxury buyers exited the market in 2024, with a further contraction expected in 2025.

> Post-pandemic price fatigue: Many brands raised prices aggressively (Chanel’s classic flap bag tripled in price since 2015), but perceived value hasn’t always kept up.

> China slowdown: Formerly the sector’s main growth driver, Chinese consumption is down nearly 20% year-over-year.

> U.S. market vulnerability: American consumers are more price-sensitive post-COVID, especially among younger and occasional shoppers.

Luxury houses are trying to avoid repeating past mistakes. UBS estimates that brands may pass only a 2% price increase to U.S. consumers to avoid a projected 3% earnings hit. Yet, maintaining prestige without pushing prices beyond consumer tolerance will require more than financial engineering. Brands may have to reexamine sourcing, redesign product strategies, and – perhaps most critically – restore the trust eroded by years of aggressive markups.

In a market where perception is everything, and value is under scrutiny, European luxury brands can no longer count on name alone. The era of unchecked pricing power appears to be over.

In a candid moment during Hermès’ Q2 2025 earnings call, CEO Axel Dumas issued a pointed critique of the booming secondary market for Birkin bags, one of the most coveted status symbols in the world of luxury. Dumas did not mince words when addressing what he sees as a troubling disconnect between the brand’s intended clientele and the increasingly transactional nature of the Birkin’s resale ecosystem. “Sometimes we have false customers come to our stores to buy them, to resell them, and they prevent us from serving our real customers, and that is a real cause for concern for us,” Dumas said.

He added: “So, I’m not at all happy to see this development of new bags that are sold in the secondhand market … I’m not happy, and it doesn’t make me feel in a good mood.”

Despite Dumas’ frustration, Hermès’ Q2 performance underscores the paradox: the very scarcity and allure that fuel the resale market are also what continue to drive Hermès’ growth. The company posted a 9% increase in quarterly sales, buoyed by demand for its “Holy Trinity” of handbags – the Birkin, Kelly, and Constance – even as broader luxury spending has slowed.

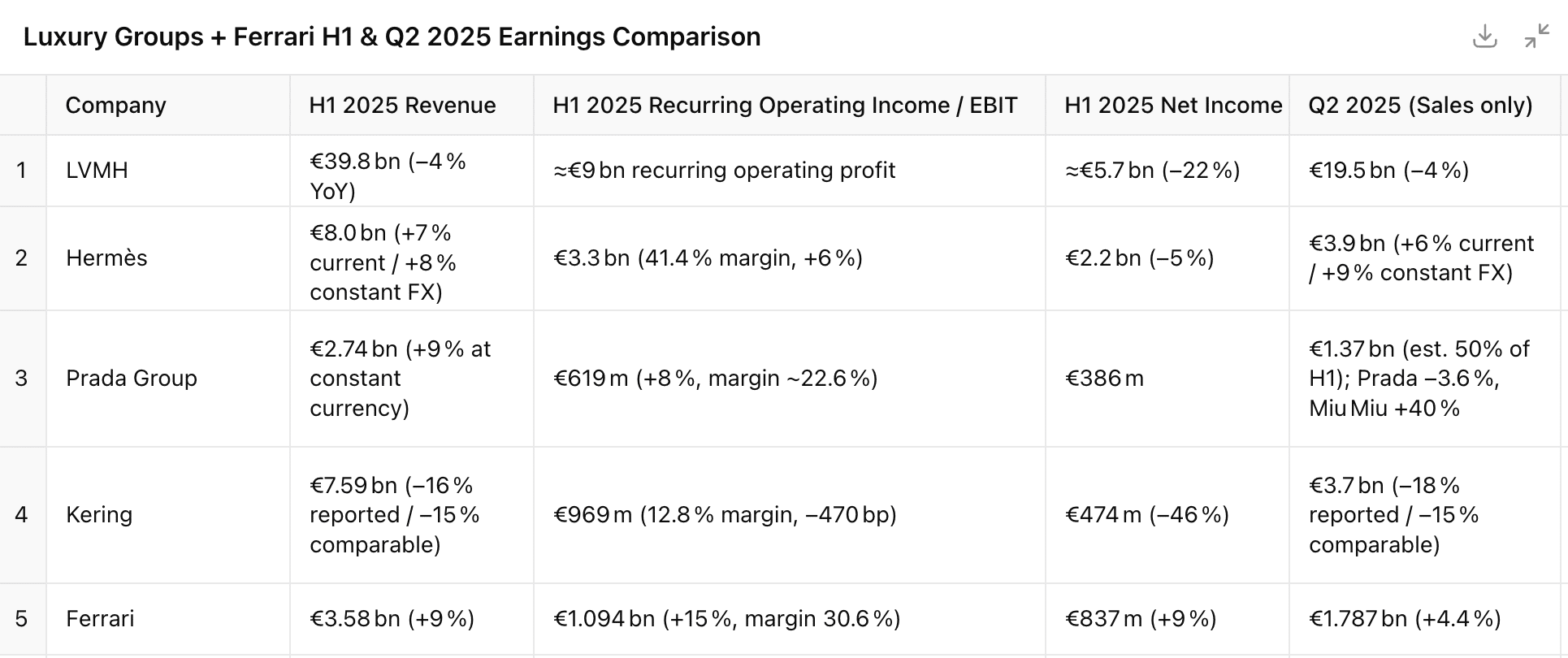

Luxury groups are busy reporting their results for the first half of 2025, and the figures coming from some of the industry’s biggest names paint a sharply divided picture across the sector. While Hermès continues to outperform with strong sales growth and exceptional margins, other giants like LVMH and Kering are grappling with slowing revenues, falling profits, and weakening momentum at key brands. Prada Group sits somewhere in between – bolstered by Miu Miu’s impressive surge, even as the Prada label slips.

From revenue declines and margin compression to brand-specific volatility, the latest round of earnings highlights the widening performance gap in an industry adjusting to price fatigue, trade pressures, and shifting consumer sentiment.

> LVMH: Revenues fell ~4% in H1 and Q2 2025, with recurring operating profit around €9B and net profit down ~22% to ~€5.7 B.

> Hermès: Delivered a strong performance. H1 sales up ~7–8%, recurring operating income up 6%, margin at 41.4%, and Q2 sales growing ~9% at constant FX (€3.9B).

> Prada Group: H1 net revenues rose 9% (to €2.74 B) led by Miu Miu; adjusted EBIT increased 8% (€619M, ~22.6% margin); net income €386M. Prada brand was down ~3.6% in Q2, while Miu Miu surged ~40%. And speaking of Miu Miu, it nabbed the top spot on Lyst’s Q2 index …

> Kering: Suffered a sharp decline. H1 revenue was down 15–16%; recurring operating income €969M (margin 12.8%); net income €474M (–46%). Q2 sales dropped ~15–18%, with Gucci down ~25% in Q2, alone.

> Ferrari: Delivered resilient growth amid macro pressures. Q2 revenues rose 4.4% to €1.787B, with EBITDA at €709M and an EBIT margin of 30.9%. Net profit reached €352M, up 7.2%, and the company confirmed full-year guidance after removing a tariff-related margin risk.

Top performer: Hermès shows the strongest growth and profitability among peers, with high margins and consistent Q2 momentum. Ferrari also stands out for its margin discipline and tariff resilience.

Brand contrasts: Within Prada, brand mix matters, with Miu Miu strongly outperforming the Prada label. At Kering, Gucci’s slump is dragging down group results.

Margins: Hermès retains a very high margin (~41%), Ferrari ~30.9% EBIT margin, Prada stable (~22.6%), LVMH recurring margin ~23%, and Kering at a lower ~12.8%.

Kering SA is offering Luca de Meo a €20 million sign-on package as he prepares to step in as CEO this September, per Bloomberg, compensating him for the long-term incentives he forfeited when leaving Renault. The bonus, split between cash and shares, accompanies a proposed fixed salary of €2.2 million for 2025, plus up to €1.21 million in annual performance-based pay tied to strategic milestones.

In 2026, his variable compensation could soar to 300% of his base salary – potentially €6.6 million – if performance targets are exceeded. Known for steering Renault back to profitability, de Meo is now tasked with revitalizing Kering’s luxury portfolio.

> While common in tech, banking, and U.S. corporate settings, where they are used to attract star talent or lure executives from competitors, signing bonuses are less commonplace in the luxury. However, that may be changing. Over the past five years, luxury brands, particularly in Europe, have increasingly turned to “golden hellos” to recruit top C-level talent, especially when candidates must forfeit unvested compensation to make the move. These bonuses, while still selective, are becoming more visible in strategic hires, notably for CEOs and CFOs brought in to lead turnarounds, drive growth, or execute digital transformation.

In addition to de Meo’s impending pay day, Burberry ponied up approximately £6 million to Jonathan Akeroyd “to compensate for share and cash incentives from [former] employer [Versace] that he [would] forfeit on joining Burberry.” (Akeroyd held the CEO role at Burberry from April 2022 to July 2024.)

Though still subject to greater governance scrutiny in Europe than in the U.S., these awards are often structured to align with performance or paid over several years to ensure retention and investor support. As executive mobility and competition intensify, especially across industries, luxury firms appear increasingly willing to invest in substantial upfront incentives to secure transformative leadership.