BCG and Altagamma recently released their 11th annual “True-Luxury Global Consumer Insights” report, offering a sharp diagnostic of the shifting luxury landscape. In a year marked by economic headwinds and fading aspirational demand, the report draws on data from 7,000 global consumers, top-tier VIC interviews, and Altrata’s Wealth-X database to spotlight where growth remains: the ultra-affluent. The study urges brands to pivot decisively: refocus on product excellence, elevate personalization through AI-enabled clienteling, and rebuild intimacy and recognition for the wealthiest consumers who are driving the industry’s future.

With democratization in retreat, luxury’s next chapter hinges on exclusivity, experience, and a return to the core. Here are the top-line areas of the report to review …

1. Top-Tier Clients Are the New Power Center of Luxury: Though only 0.1% of the population, top-tier clients (spending €50K+/year) now generate 23% of all luxury sales – nearly double their 2013 share. Their spending tracks stock markets (60% correlation), not GDP, and their numbers are growing at 8–10% annually, reaching 900K+ HNWIs globally.

2. Aspirational Consumers Are Pulling Back: 35% of aspirational buyers (€2K–€20K spend/year) have reduced or stopped luxury purchases, shifting toward savings (22%), wellness (13%), secondhand (13%), and tech (12%). With inflation and economic stress mounting, 65% expect to hold or cut spending further.

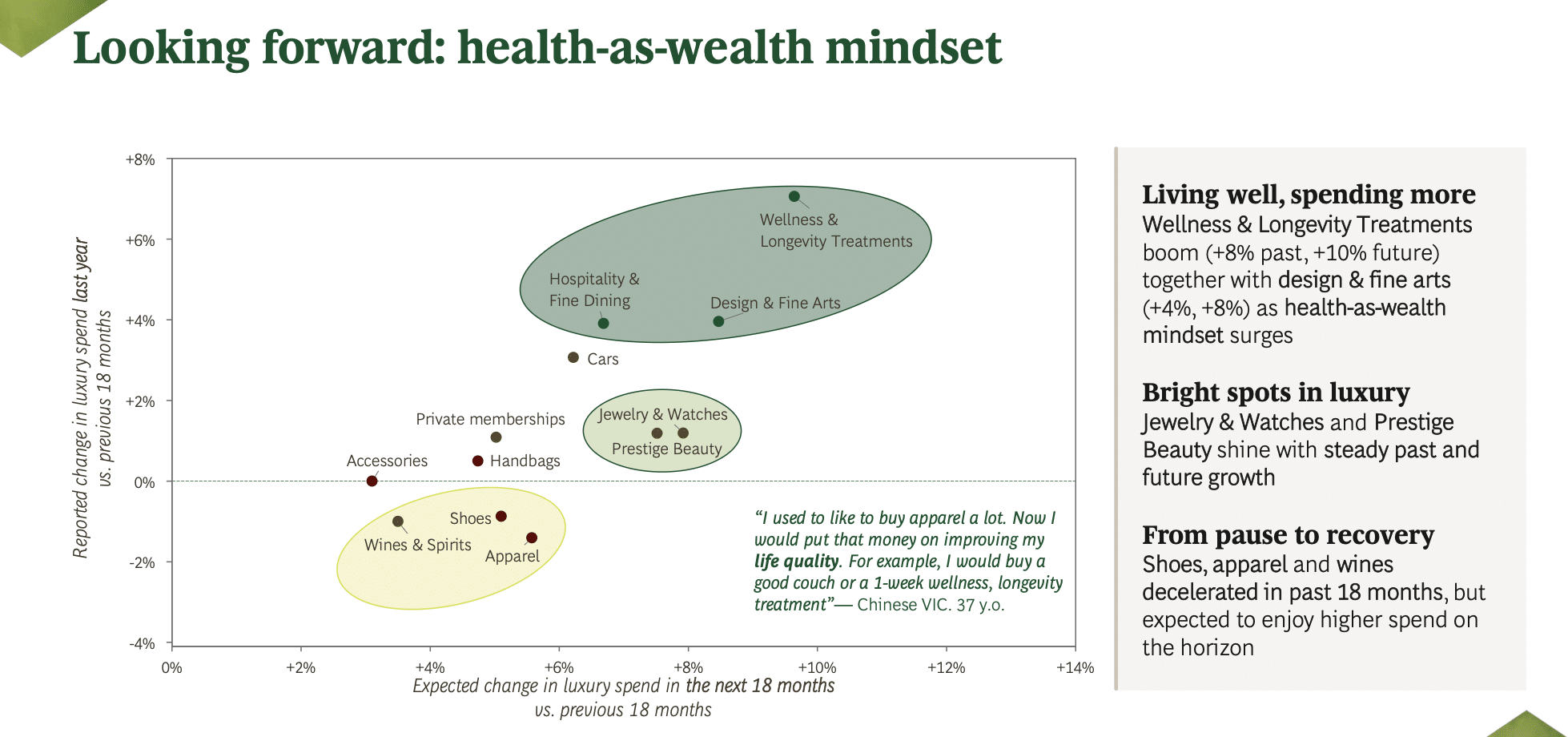

3. The ‘Health-as-Wealth’ Mindset Is Reshaping Spend: Spending is rising in wellness (+8% past, +10% future) and design/fine arts, reflecting a shift from material goods to quality-of-life investments. Traditional categories like apparel and wine are expected to rebound after a slowdown.

4. The Democratization of Luxury Has Peaked – and Is Reversing: Brands heavily reliant on aspirational buyers (50%+ exposure) are underperforming. Decades of scaling via beauty, eyewear, and influencers have hit a ceiling. As affordability drops, the market shifts back toward exclusivity and fewer casual walk-ins.

5. Gen Z Remains a Rare Bright Spot: Gen Z is the most optimistic cohort, with 80% planning to spend on luxury in the next year. They feel more represented by brands than older generations and gravitate toward identity-driven, values-based storytelling.

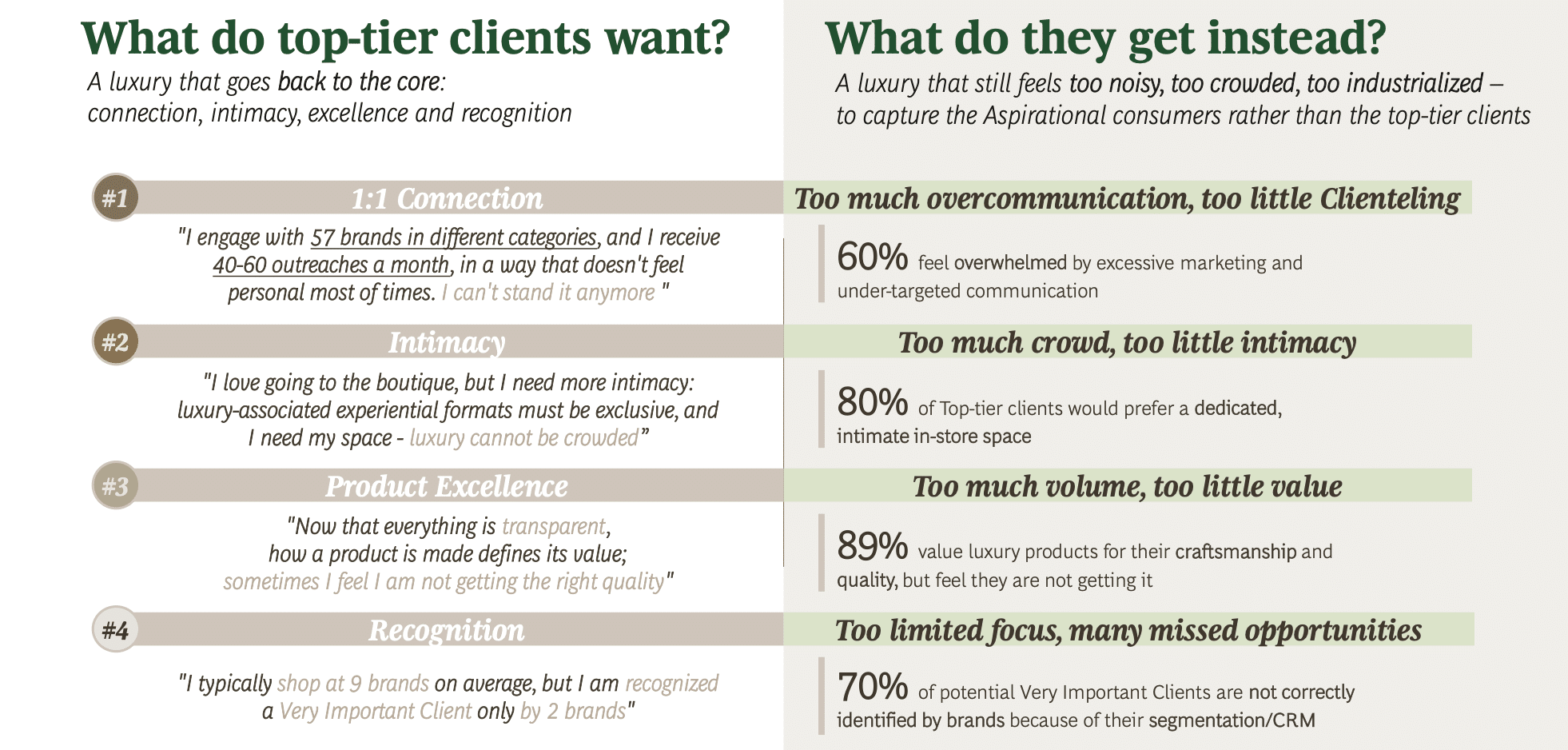

6. Top-Tier Clients Are Dissatisfied – Despite Their Value: Despite their contribution to growth, top-tier clients report 4 persistent frustrations: Overcommunication with impersonal marketing; crowded retail experiences lacking intimacy; poor product quality, despite rising prices; and inconsistent recognition as VIP clients across channels and regions

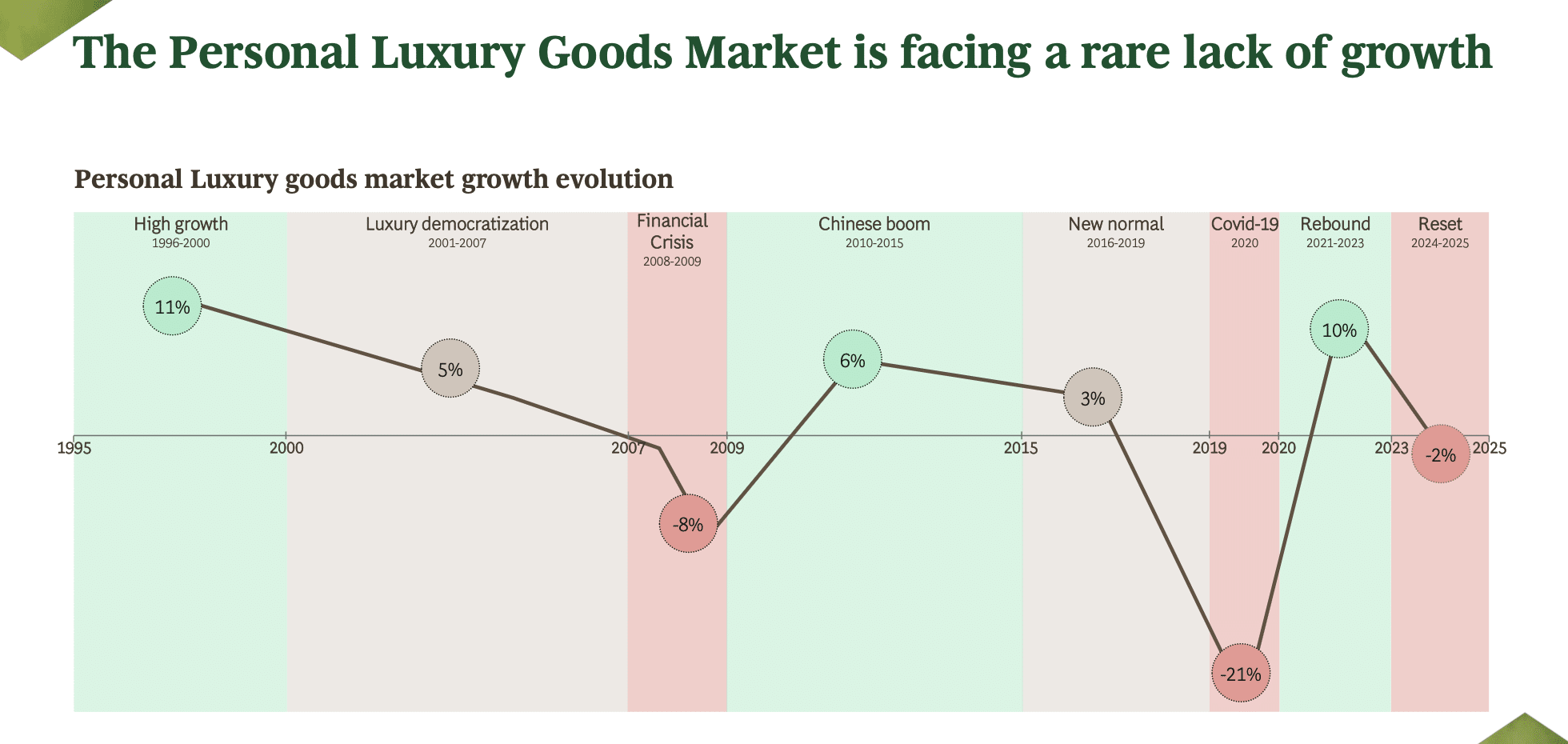

7. The Luxury Market Is Entering a “Reset” Phase: After a post-Covid rebound, luxury is stagnating in 2024–2025. Chinese spending – once the main driver – is down 5% due to macro factors. Demand isn’t disappearing, but access is narrowing as affordability gaps widen.

This is a short excerpt from a weekly briefing that is published exclusively for TFL Pro+ subscribers. For access to all of TFL’s content, including our weekly briefings, inquire today about how to sign up for a Professional subscription.

Share