A shareholder of The RealReal (“TRR”) is attempting to bulk up his stock-drop case against the luxury resale entity, arguing that the company, an array of its executives, and its big-name initial public offering (“IPO”) underwriters misled investors about the nature of its authentication process, thereby, “artificially inflating” the price of its shares and then damaging those same shareholders “when the artificial inflation dissipated.” On the heels of a California federal court agreeing to toss out part of the federal securities action against TRR and co. in an opinion and order on March 31 (while allowing other claims to remain in place), lead plaintiff Michael Sanders was granted leave to amend his complaint to plead “more particular facts” in order to make his case.

In a second amended complaint filed on April 30, Sanders and named plaintiffs Nubia Lorelle and Garth Wakeford (the “plaintiffs”) reiterated many of the foundational allegations that they made in their earlier complaints, namely, that TRR made false and misleading statements in its registration documents prior to its 2019 IPO, and that these “false and misleading statements continued in the months following the IPO, thereby artificially inflating the stock’s market price.” For instance, despite TRR’s claims in its 2019 IPO filings that its “highly trained experts build trust in our buyer base by thoroughly inspecting the quality and condition of, and authenticating, every item we receive,” the plaintiffs claim that the company’s “authentication process fell far short of its description, [with] only a small proportion of the thousands of items processed by [TRR] each day actually go to its small group of expert authenticators – specifically only certain brands and items deemed to face a particularly high risk of counterfeiting.”

“The vast majority of items supposedly ‘authenticated’ by [TRR] were actually reviewed only by … low-wage hourly employees, often with little or no experience in fashion or luxury products,” according to the plaintiffs, who also claim that the authentication issue was exacerbated by the fact that these individuals “were held to onerous quotas of a certain number of items they were required to process per day,” meaning that in at least some cases, they “could only devote approximately 2-4 minutes to any given item,” a time frame that allegedly required the individual “copywriters” to authenticate an item, as well as inspect it for quality/damages, measure it, and write the corresponding copy for the company’s e-commerce site.

The alleged reality of TRR’s authentication operations is at odds with the warranties that the company made in its IPO documentation, according to Sanders and the two other plaintiffs, and this proved to be problematic “in the months following the [June 27, 2019] IPO, [when] the truth about TRR’s authentication process began to leak out” by way of various media articles. Specifically, the plaintiffs point to “an extensive investigative report conducted and published by CNBC,” which revealed that despite TRR’s claims to the contrary, “untrained, inexperienced, and overworked copywriters were performing the bulk of the ‘authentication’ efforts at [TRR].” The first of two November 2019 articles from CNBC, as well as articles from other sites, such as Forbes, “challeng[ed] the claims by [TRR] and its CEO, [Julie] Wainwright, that there are ‘no fakes on our site,’ and that ‘every single item [is] authenticated’” by highlighting that “most pieces were being handled by copywriters” with “little training … on how to spot fakes,” and that “only very, very high-value items, it seemed, were being authenticated by the actual lead authenticators.”

Sanders and the other named plaintiffs assert that interviews conducted by their investigator with over one dozen former employees of TRR “corroborate the facts reported” by CNBC and a couple of other publications, including that “outside of certain brands, garments, and specialty leather goods and furs, everything else … essentially, did not have to go through authentication,” “85-90 percent of the product never gets seen by the official authentication team,” “there is no way that things could be authenticated on the site; there were never enough people to do it,” and TRR “would often hire copywriters with no experience in fashion, and that many of these people would struggle with authentication and would inadvertently pass counterfeit items on to [TRR’s] website.”

Beyond these assertions, one “former employee” told the plaintiffs’ investigator that “in addition to attempting to authenticate each item, copywriters were tasked with taking measurements and entering other information into a comprehensive database to prepare them for sale,” and thus, TRR’s copywriters often “tried to keep [inspections] under a minute for [each item].” An additional former employee alleged that they were never “actually trained on authenticating things,” while another “reported receiving only a basic two-hour training on their first day and then was given their daily quota and informed for the first time that they would be responsible for authentication, as well as copywriting.”

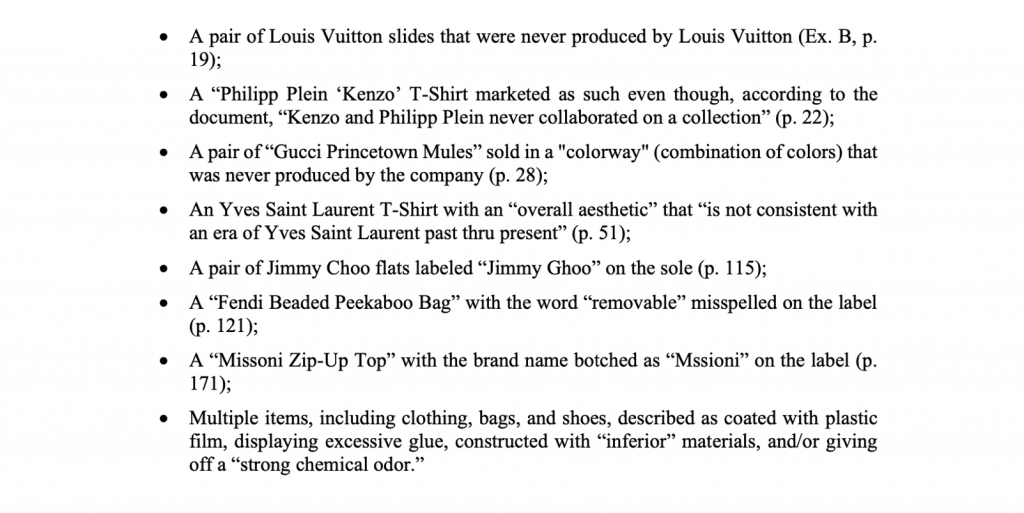

Still yet, another former TRR employee asserted after “shifting to a customer service role [from a copywriting role], that ‘people would return stuff all the time’ as counterfeit … it just happened way more than it should have for a company that says everything [is] authenticated.” And finally, one former employee “explained that many items should have been easily identifiable as counterfeit” and yet, slipped through the cracks. These included …

Against this background and in furtherance of their Securities Act claims, the plaintiffs assert that the Registration Statement that was issued in connection with TRR’s IPO “was inaccurate and misleading, contained untrue statements of material facts, [and] omitted other facts necessary to make the statements made not misleading” in connection with the company’s authentication process. “The individual defendants were in positions to control and did control, the issuance of the false and misleading statements and omissions contained in the Registration Statement,” according to the plaintiffs, who allege that “none of the individual defendants or [TRR] made reasonable investigation or possessed reasonable grounds for the belief that the statements contained in the Registration Statement were accurate and complete in all material respects.”

All the while, the plaintiffs allege that IPO underwriters, including including BoFA Securities, UBS Securities, and Cowan and Company, among others, “failed to perform adequate due diligence in connection with their role as underwriters for the IPO and were negligent in failing to ensure that the Registration Statement was prepared properly and accurately, free of misrepresentations or omissions.” In addition, Sanders claims that “the underwriters met with potential investors and presented highly favorable but incorrect and/or misleading information about [TRR], its business, products, plans, and financial prospects, and/or omitted to disclose material information required to be disclosed under the federal securities laws and applicable regulations promulgated thereunder.”

As a result, the plaintiffs and the class – i.e., “all persons and entities who purchased [TRR] common stock from June 27, 2019 through November 20, 2019” – have “sustained damages,” according to Sanders, namely because “the value of [TRR] common stock has declined substantially due to the Securities Act violations alleged herein.”

In furtherance of their separate Exchange Act claims, the plaintiffs assert that the defendants “made a number of additional false and misleading statements and omissions of material fact during the Class Period about [TRR’s] purported authentication process.” For instance, they allege that “on the day of [TRR] IPO, Defendant Julie Wainwright appeared on CNBC” and said that “every single item on the site has already been inspected, authenticated before it gets on the site,” which the plaintiffs argue is “false and misleading because Wainwright failed to disclose that (1) the small group of authenticators employed by [TRR] did not authenticate every item, or even most items; and (2) the copywriters who actually did inspect and purportedly ‘authenticate’ the vast majority of the items did not put the items through a ‘rigorous multi-point inspection process.’”

Beyond that, on September 26, 2019, TRR Chief Financial Officer Matt Gustke “engaged in an extended conference call discussion with a Wells Fargo securities analyst and answered questions about the [TRR] authentication process.” During that call, Gustke asserted that TRR authenticates all goods “through a no risk multi-point process – absolutely, every item,” which the plaintiffs contend is “false and misleading because Gustke failed to disclose that [TRR’s] authentication process was not ‘no risk,’ and in fact, [it] maintained an internal, regularly updated list of hundreds of purportedly authenticated items returned by customers as counterfeit.”

The plaintiffs allege that “at all relevant times, including at the time of the IPO and during the class period, the Officer defendants and [TRR] knew, or were reckless in not knowing, that their public statements were false and misleading,” and as described in varying detail in a number of media articles, TRR’s “authentication process – having untrained and overloaded copywriters take on the responsibility of authenticating hundreds of items each day that were not seen by the Company’s actual authenticators – had been in place for years and was well known to everyone working at [TRR].” Also, the plaintiffs assert that former TRR employees “confirmed that the company’s executives … were unquestionably aware of [its] flawed authentication process, including the onerous quota system and lack of sufficient training for copywriters.”

Ultimately, Sanders and the other name plaintiffs claim that during the class period, the defendants’ “material misrepresentations and omissions” which can be attributed to TRR, “caused the damages sustained by the plaintiffs and the other members of the class,” thereby, causing “the artificial inflation” of TRR’s common. The defendants’ “material misrepresentations and omissions created an unrealistically positive assessment of [TRR] and its business, operations, and prospects, causing the price of the company’s common stock to be artificially inflated at all relevant times, including when the plaintiffs and other members of the Class purchased the stock.”

“When the truth hidden by these misrepresentations and omissions was disclosed,” the plaintiffs claim that “that disclosure negatively affected the value of the company’s common stock, dissipating the artificial inflation and damaging the plaintiffs and other members of the Class.” Specifically, they argue that on that on the heels of the publication of the first CNBC article on November 5, 2018, TRR’s “share price fell $2.37, or over 10 percent, to close at $19.37 at the end of trading on [that day] on unusually heavy trading volume, [and] the Company’s share price fell a total of $3.80, or over 18 percent, by the end of the next day to close at $17.93 on November 6, 2019, on unusually heavy trading volume.”

All the while, Sanders and the other plaintiffs claim that TRR and the Officer defendants, “individually and in concert … employed devices, schemes and artifices to defraud; made untrue statements of material facts or omitted to state material facts necessary in order to make the statements made, in light of the circumstances under which they were made, not misleading; and/or engaged in acts, practices and a course of business that operated as a fraud or deceit upon the plaintiffs and others similarly situated in connection with their purchases of the company’s common stock during the class period.”

“TRR and the Officer defendants” – the latter of whom have “the power to direct the actions of, and exercised the same to cause, the company to engage in the unlawful acts and conduct complained of herein” – “acted with scienter in that they knew that the public documents and statements issued or disseminated in the name of the company were materially false and misleading,” the plaintiffs argue, and yet, they “knowingly and substantially participated, or acquiesced in the issuance or dissemination of such statements or documents,” which amount to “primary violations of the securities laws.”

With the foregoing in mind, the plaintiffs claim that they – and all other individuals who purchased TRR common stock during the class period – have been damaged “as a result of the defendants’ wrongdoing.” While the plaintiffs say that they do not know “exact number of class members” at this time, they “believe that there are hundreds, if not thousands of members in the proposed class.” As a result, Sanders and the other two named plaintiffs have asked the court to determine that the case may be maintained as a class action, and asserted that they entitled to monetary relief for “all damages sustained as a result of the defendants’ wrongdoing, in an amount to be proven at trial.”

Not the only shareholder action currently in the cards, TRR shareholder Iwona Grzelak filed suit against the company in September 2020, arguing that a number (but not all) of the company’s individual Board members – from founder Julie Wainwright to PVH Corporation president Stefan Larsson – and executives like Chief Financial Officer Matt Gustke and Chief Accounting Officer Steve Lo (collectively, the “defendants”) intentionally or recklessly breached their fiduciary duties as directors and/or officers, and violated the U.S. Securities Exchange Act in the process. Because Grzelak’s lawsuit “challenges substantially similar alleged conduct and involves substantially similar questions of law and fact as alleged in the federal securities action” that Sanders filed in November 2019, it has been put on hold for the time being.

A rep for TRR was not immediately available for comment. However, the company has previously argued that Sanders failed to meet the heightened pleading requirements applicable in securities fraud cases. TRR has also taken issue with the allegedly “misleading” statements, arguing that Sanders’ allegations “do not demonstrate that any challenged statements were false or misleading and, in any event, represent corporate puffery,” while also challenging the reliability of the former employees, among other things, on the basis that they were not employed by the company during the class period, and that their testimony amounts to “gripes of a few insufficiently trained employees that do not render the company’s statements regarding authentication false or misleading.”

The case is Michael Sanders, et al. v. The Realreal, Inc., et al. 5:19-cv-07737 (N.D. Cal).

Share