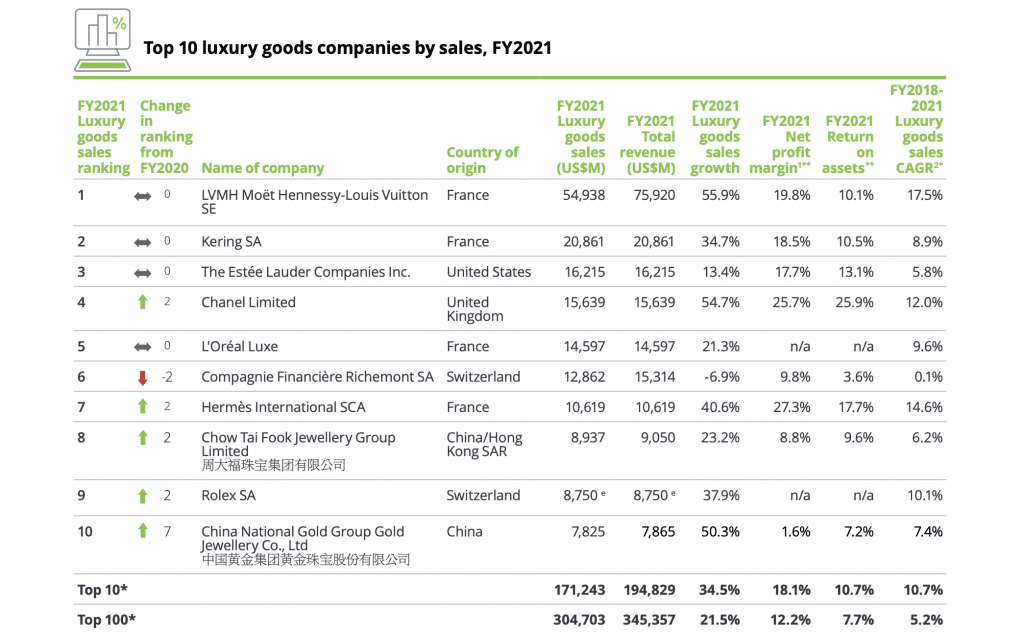

The fashion and luxury goods industry is facing major global challenges in terms of sustainability, digitalization, and consumption patterns – all factors that will lead to “radical transformation” in the coming years, according to Deloitte’s 2022 Global Powers of Luxury Goods report. Despite such challenges, the consultancy found that during FY2021, luxury goods companies rebounded from the COVID-19 pandemic, with the top 100 luxury goods companies generating composite sales of $305 billion, a 21.5 percent year-over-year increase that overtakes pre-pandemic FY2019 levels of $281 billion.

The importance of the leading luxury goods companies is “clear,” according to Deloitte, with the 15 companies with luxury goods sales of more than $5 billion, contributing more than two-thirds of the total Top 100 luxury goods sales, while the 45 companies with sales of $1 billion or less contributed only 6.7 percent to the total. Delving into the Top 100 companies – those that operate in the luxury market (i.e., luxury for personal use, including ready-to-wear, bags and accessories (including eyewear), luxury jewelry and watches, and prestige and luxury beauty), and that have a minimum revenue threshold of $240 million), Deloitte found that 73 of the Top 100 companies reported growth in luxury goods sales in FY2021, compared to only twenty in FY2020.

LVMH, Chanel, Chow Tai Seng, Inter Parfums and new entrant Grupo de Moda Soma all saw luxury goods sales jump by more than 50 percent.

Net profit margins also recovered in FY2021, per Deloitte, with nearly 80 percent of the Top 100 reporting profitability in FY2021, compared with 61 percent in the previous year. Twenty-three companies reported double-digit net profit margins. Still yet, 18 companies in the Top 100 reported both double-digit luxury goods sales growth and double-digit net profit margins in FY2021. These included half of the Top 10 luxury giants, as well as Italy’s Moncler. LVMH, Kering, Chanel, and Moncler all reported double-digit sales growth and net profit margins in each of the past five years (excluding FY2020 due to the pandemic). Deloitte notes that Hermès – which took the number 7 spot on the Top 100 list – is “also a consistently high performer for both sales growth and profitability.”

Addressing the Top 10 (companies with a sales threshold of more than $7.8 billion), in particular, Deloitte states that these ten companies “increased their share of the total luxury goods sales of the Top 100 companies by 4.8 percentage points,” contributing 81.4 percent of the YOY growth in sales of the Top 100 companies, and 84.7 percent of the combined net profit of the Top 100 companies.

“Chanel overtook Richemont and L’Oréal Luxe to take fourth place in the rankings. Hermès International and Chow Tai Fook both moved up two places. Rolex returned to the Top 10 for the first time since Global Powers of Luxury Goods 2014, in ninth place. China National Gold Group Jewellery Co was another new entry into the Top 10, in tenth place. EssilorLuxottica disappeared from the Top 10 – it had to be excluded as the company’s luxury goods sales could not be estimated following a change in its financial reporting. PVH Corp fell out of the Top 10 as its Tommy Hilfiger and Calvin Klein luxury brands saw sales decline due to the impact of the COVID-19 pandemic.”

Key Themes for 2023

In addition to diving into the revenue and profit figures of the Top 100 companies, Deloitte reflects on key themes/opportunities in fashion/luxury, including facets of ESG/sustainability and web3 for the year ahead (and beyond) …

Primarily, Deloitte asserts that “as we have seen in previous editions of this report, sustainability in particular has become a core priority for luxury goods companies.” Given that the fashion and luxury industry has “long been criticized for the environmental impact of its production processes and consumption practices,” an increasing number of companies are “including sustainability principles in their core strategies, making it a new paradigm of conceiving luxury by following ESG criteria (Environmental, Social, and Governance) and applying the concept of being ‘sustainable by design.’”

This is taking an array of forms, including secondary market-focused endeavors, with Deloitte noting that “to adopt circularity, luxury companies would have to disrupt their traditional linear model of “take-make-use-waste” and work on new strategies, with the aim to: (1) Foster new business models that increase products use (second hand, resale, renting); (2) Create safe, renewable raw materials (bio-materials, bio- chemicals, etc.); and (3) Implement alternative solutions which allow used products to be turned into new (repairing, recycling, etc.).”

Looking at resale specifically, Deloitte states that consumers are changing the way in which they buy, use, and sell luxury products and are “increasingly showing interest in the second-hand market.” Due to the growing demand in this market segment,luxury goods companies are “discovering how the pre-owned category can help to extend the lifetime of their products and to increase the relevance of brands among new, and mostly young, woke consumers.” Some companies are already investing and joining forces with resale platforms as an alternative distribution channel, per Deloitte. (And as we noted not too long ago, big-name brands are testing the waters of resale, but even bigger names have been unapologetic about their unwillingness to actively participate in the resale market – Louis Vuitton, Chanel, and Hermès come to mind.)

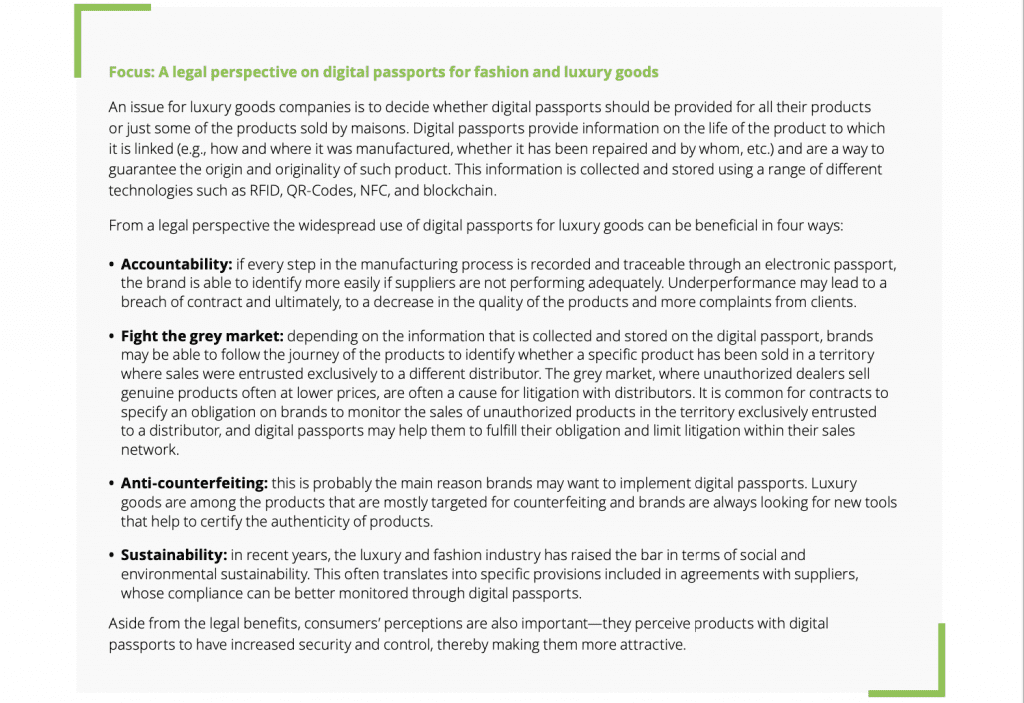

The rise of the resale market and the overarching adoption of e-commerce by brands across the spectrum of fashion and luxury has caused the risk of a proliferation in counterfeited goods to increase, according to Deloitte, which states that “counterfeit goods are one of the most severe problems for the luxury industry.” Against this background, companies are turning their attention to effective solutions to the problem. One of them is the digital passport, a digital tool (often based on blockchain technology) that verifies the origin of luxury goods such as designer items or works of art.

Blockchain, a technology that is commonly associated with cryptocurrencies, has gained a role in the luxury goods market, according to Deloitte, “as it helps to verify and authenticate the origin of an item.” Whether it is a new or secondhand item, a purchase can be verified immediately by scanning its digital passport that can communicate its provenance and demonstrate that the item is authentic. Luxury companies are beginning to use this new technology more intensively as indicated by a partnership between the LVMH, Richemont-owned Cartier, and Prada Group-created Aura Blockchain Consortium and the Sustainable Markets Initiative Fashion Task Force, the latter of which was created by His Royal Highness King Charles III, is chaired by former YNAP founder and chairman Federico Marchetti, and boasts members, such as executives from Brunello Cucinelli, Burberry, Chloé, and Giorgio Armani, among others.

As for the metaverse, which garnered quite a bit of attention in 2022, Deloitte states that at this moment, it is “mainly used to reinforce luxury companies’ brand equity and drive traffic to their websites and stores.” While “there are many other potential uses of the metaverse,” in order to activate any of them, companies “need to adopt the foundational technologies underpinning the metaverse (such as NFTs and blockchain) and at the same time, adapt to the rapid pace of technological change.”

Ultimately, Deloitte states that “none knows what the metaverse could become, but the momentum for progress is unlikely to slow down or go into reverse,” asserting that “by taking advantage of the many opportunities offered by the metaverse, well-prepared fashion and luxury companies could help to shape an exciting future.”

Share