Artificial intelligence is beginning to occupy a new place in retail’s corporate landscape. Once discussed primarily in product launches and innovation initiatives, AI is becoming part of the disclosures that consumer goods companies use to explain how they create value, compete, and manage risk. Reformation’s newly filed initial public offering registration statement offers one of the clearest recent examples of that evolution.

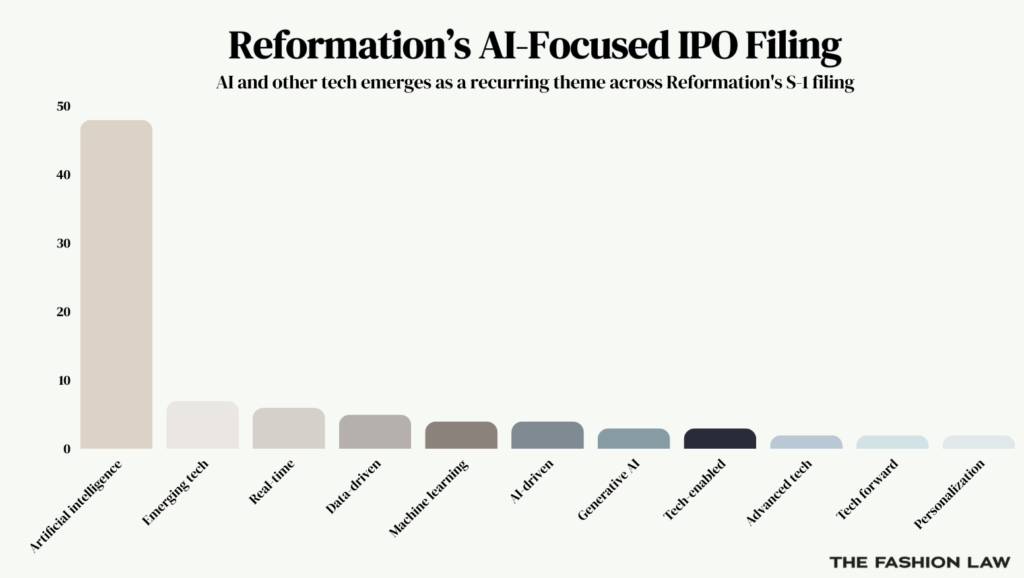

In the S-1 registration statement that it filed with the Securities and Exchange Commission on June 25, Reformation describes using AI and machine learning to support merchandising, demand forecasting, inventory allocation, and product development. Rather than presenting AI as a standalone initiative or consumer-facing feature, the Los Angeles-based fashion company – which mentions “AI” 48 times in its S-1 – frames it as part of the operational infrastructure that underpins its predominantly direct-to-consumer business.

Those references are concentrated not in a standalone technology discussion, but throughout the filing’s descriptions of merchandising, business strategy, and enterprise risk.

Operational AI Becomes an Investor Story

Reformation’s emphasis on AI – along with machine learning and “emerging” and “advanced” technologies – reflects a broader shift in how companies articulate competitive advantage to investors. Rather than focusing solely on brand strength, consumer demand, and digital capabilities, companies are devoting more attention to the operational systems they believe support long-term value creation.

The inclusion of AI in securities filings – particularly in discussions of business strategy, operations, and enterprise risk – reflects a broader change in how companies frame their investment case. Alongside revenue growth and brand strength, management teams are placing greater emphasis on the systems they believe drive productivity, inventory efficiency, and long-term performance.

The filing is equally notable for the way it frames AI as a source of risk. Alongside its discussion of AI-enabled operations, the company cautions that its use of AI technologies may expose it to a range of operational and legal risks, including inaccurate or misleading outputs, intellectual property disputes, cybersecurity and data privacy issues, evolving regulatory requirements, and reputational harm.

The filing notes that AI-generated content “may contain errors, inaccuracies, or hallucinations” and warns that the company could face liability if AI systems generate “inappropriate, offensive, or otherwise harmful” outputs. It also identifies the rapidly evolving regulatory landscape – including the European Union’s AI Act – as a potential source of increased compliance obligations, observing that emerging AI laws “may impose significant operational and compliance burdens” on companies deploying the technology.

When AI Becomes Enterprise Risk

While much of the media coverage surrounding Reformation’s impending IPO has focused on the company’s growth trajectory and profitability, one of its filing’s more consequential features may be its treatment of AI. Taken together, Reformation’s discussion of AI’s commercial benefits and accompanying risk disclosures reflects a broader shift in corporate reporting: AI is no longer presented solely as a source of competitive advantage, but also as an enterprise risk requiring governance and oversight.

The legal significance extends beyond Reformation. Although U.S. securities laws do not require companies to include a standalone discussion of AI, they do require disclosure of material information about a company’s business, operations, and risks. As AI becomes integral to merchandising, forecasting, pricing, customer engagement, and other core commercial functions, boards and management teams face increasingly consequential judgments about when AI capabilities – or AI-related risks – become sufficiently material to warrant disclosure.

The relevant question is not whether a company has adopted AI, but whether its use of AI has become material to the business. Companies will need to assess whether their use of AI meaningfully affects their operations, strategy, financial condition, results of operations, or risk profile in ways that a reasonable investor would consider important.

Reformation’s S-1 also illustrates how the legal implications of AI are expanding. To date, fashion’s AI-related disputes have largely centered on intellectual property, publicity rights, deepfakes, and generative AI in consumer-facing contexts. Its IPO filing points to a broader legal frontier: AI as an operational and governance issue, raising questions of materiality, enterprise risk oversight, and securities disclosure.

THE BOTTOM LINE: As AI becomes part of the operating architecture of fashion businesses, companies will be expected not only to explain how AI creates value, but also how it is governed, monitored, and disclosed.

Share