As counterfeit goods mimic authentic products with near-perfect precision and infiltrate resale platforms, brands and marketplaces are confronting a reality that is no longer about obvious knockoffs, but about indistinguishable replicas moving through legitimate channels. For nearly a decade, counterfeiting has held a foundational share of global commerce, consistently topping $450 billion a year, or roughly 2–3 percent of world imports, even as the market has evolved from street-corner knockoffs to platform-native supply chains optimized for speed and deniability.

A Market That Doubled in a Decade

What began as a smaller segment of global trade has grown into a substantial and persistent market. In the mid-2000s, the Organisation for Economic Co-operation and Development (“OECD”) estimated that the value of global trade in counterfeit goods was around $200 to $250 billion annually. By 2013, that figure had nearly doubled to $461 billion, accounting for 2.5 percent of world trade. The market peaked at $509 billion in 2016, or 3.3 percent of global trade, before leveling slightly: OECD/EUIPO estimates placed it at $464 billion in 2019 and $467 billion in 2021. For much of the past decade, counterfeit trade has consistently exceeded $450 billion a year, representing roughly 2 to 3 percent of global imports.

These figures are widely considered conservative, as they account only for cross-border trade in physical counterfeit goods and exclude domestically produced and sold fakes, as well as pirated digital content. As a result, the true size of the illicit market is likely considerably larger.

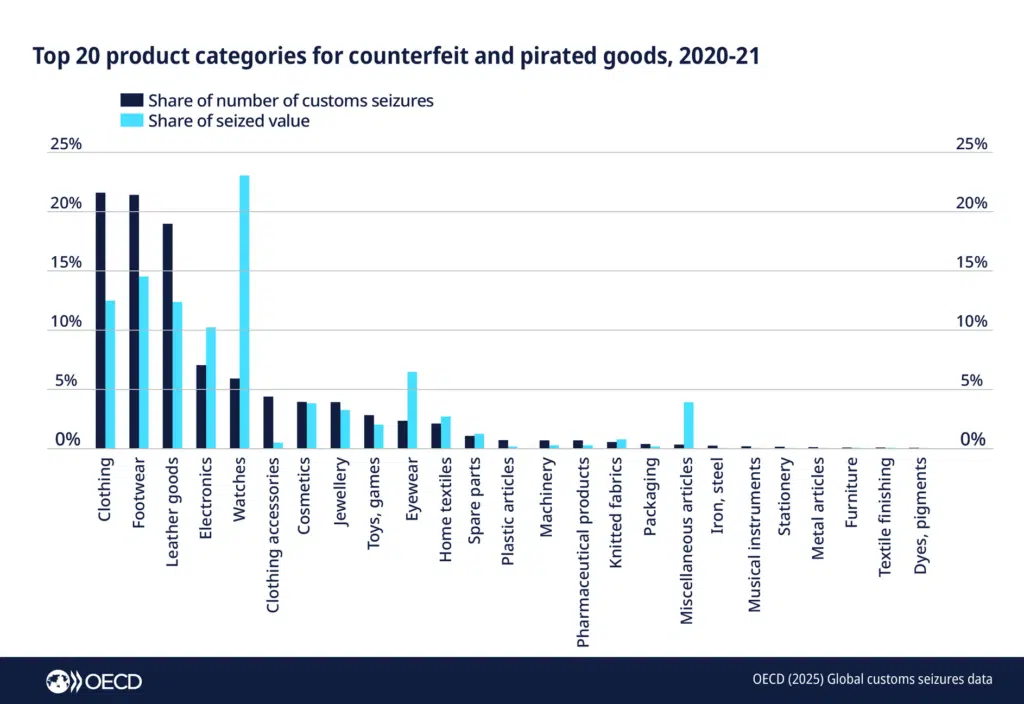

Within that market, fashion and luxury goods remain central. Apparel, footwear, and leather goods, including handbags, account for the majority of counterfeit items seized globally, representing roughly 62 percent of total volume. Footwear leads in the number of cases, followed by clothing and accessories. Watches, while fewer in quantity, account for a disproportionately large share of total value, reflecting their higher price points.

The scope of counterfeiting is also widening. Cosmetics and perfumes, while smaller in overall share, have grown in prevalence and carry heightened risks, often involving unregulated or unsafe ingredients. As counterfeiters move beyond traditional fashion categories into beauty and wellness, the implications extend beyond brand protection to consumer safety.

Superfakes & the Secondary Market Challenge

Volume alone does not capture the full extent of the shift. Increasingly, the challenge lies not just in how much counterfeit product exists, but in how convincingly it mirrors the real thing.

The emergence of so-called “superfakes,” high-quality counterfeit goods that replicate authentic products with near-perfect precision, has transformed the landscape. Unlike traditional knockoffs, these items reproduce stitching, materials, hardware, and even packaging and authentication markers with a level of accuracy that can make detection difficult, even for trained professionals.

This evolution has converged with the growth of the luxury resale market, where authentication functions as a critical point of trust. Platforms specializing in secondhand designer goods invest heavily in authentication processes, but the increasing sophistication of counterfeit products has introduced persistent uncertainty. The boundary between authentic and counterfeit goods is becoming harder to maintain, not only for consumers, but for the platforms and brands, themselves.

The presence of “superfakes” that leak into legitimate resale channels carries broader implications. For consumers, it undermines confidence in secondary markets and in the authenticity of branded goods more generally. For brands, it complicates enforcement strategies and raises new questions about how and where counterfeit goods are identified, and who bears responsibility when they are not.

E-Commerce & the Fragmentation of Enforcement

Alongside these developments, the rise of e-commerce has reshaped how counterfeit goods are produced, distributed, and detected. Online platforms provide counterfeiters with direct access to global consumers, while modern logistics networks enable rapid, decentralized distribution.

Much of this activity now takes place through small-parcel shipments. In 2020 and 2021, approximately 65 percent of counterfeit seizures involved goods sent by mail or express courier. This shift has fragmented enforcement efforts, pushing detection away from large-scale shipping hubs and into high-volume, low-value parcel flows that are more difficult and costly to monitor.

In this environment, counterfeit goods move quickly and with relative anonymity, exploiting gaps in customs enforcement, platform governance, and cross-border coordination.

The Road Ahead: Trillions at Stake

If current trends hold, the economic implications of the counterfeit market are set to grow significantly. A 2017 study by the International Chamber of Commerce and INTA projected that the global market for counterfeit and pirated goods could reach $2.8 trillion by 2022, with total economic impacts, including lost jobs, tax revenues, and brand value, exceeding $4 trillion over the same period. Even when limited to cross-border trade in physical goods, estimates have approached $1 trillion in recent years.

More recent projections point to continued acceleration. In 2024, Corsearch estimated that global trade in counterfeit goods could reach $1.79 trillion by 2030, a 75 percent increase from 2023 and a rate of growth more than three times that of the global economy. By that measure, counterfeit goods would account for roughly 5 percent of world trade, or $1 out of every $20 spent on goods globally.

Counterfeiting’s economic impact extends well beyond lost sales. In 2022 alone, it displaced an estimated $1.1 trillion in legitimate economic activity, with governments losing approximately $174 billion in tax revenue and up to 5.4 million jobs affected worldwide.

THE BOTTOM LINE: Counterfeiting is no longer confined to the margins of global commerce. It has evolved into a system-level challenge that intersects with e-commerce, resale, and shifting consumer behavior. For fashion and luxury brands, the risks extend beyond lost sales to include brand dilution, reputational damage, and in some cases, such as beauty products, consumer safety concerns. As digital commerce expands and counterfeit goods become increasingly difficult to distinguish from authentic products, the problem is becoming embedded within legitimate retail channels, making it harder to isolate and contain.

Share